What is really wrong with our energy system, particularly as it relates to electricity and natural gas? Are there any mitigations available? I have been asked to give a talk at an Electricity/Natural Gas conference that includes both producers and industrial users of electricity and natural gas.

In this presentation, I suggest that the standard diagnosis of the problems facing the energy system is incomplete. While climate change may be a problem, there is another urgent problem that attendees at the conference should be aware of as well–affordability, and the severe near-term impact affordability can be expected to have on the system.

My written summary of this talk is fairly brief. I have not tried to repeat the information shown on the slides. This is a link to a copy of my presentation: Our Electricity Problem: Getting the Diagnosis Right

Slide 2

A finite world is one that is subject to limits. Its economy cannot grow forever for many reasons.

Slide 3

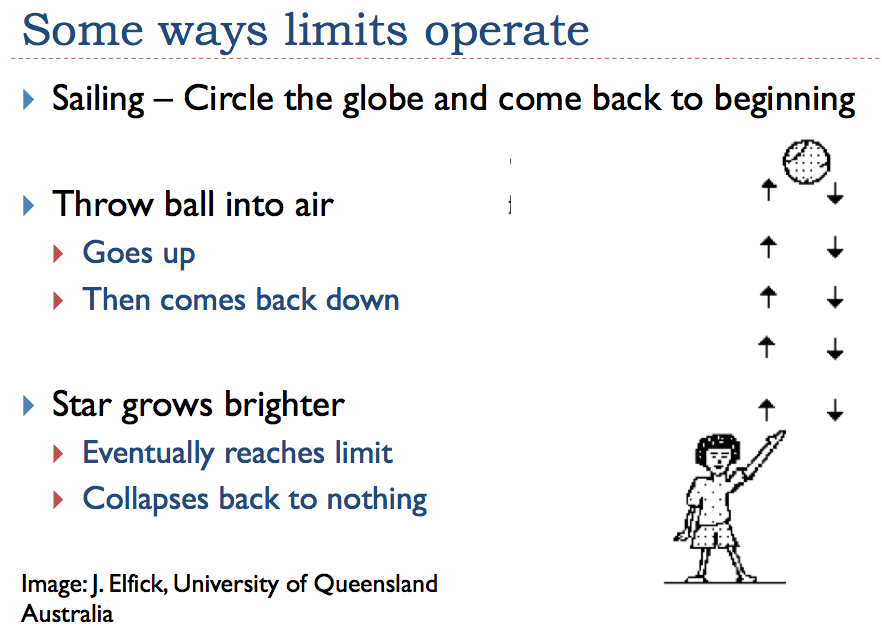

Let’s look at some examples (Slide 4) of how limits work in finite systems. Often there seems to be a change of direction.

Slide 4

The standard story that we hear says that energy prices can rise and rise, indefinitely. But as I look at the data, this doesn’t seem to be true in practice. At some point, there is a problem with affordability, because wages don’t rise as the price of energy products grows.

Slide 5

In many ways, the problems that overtake the economy are similar to ailments that beset a human being. A person can have multiple ailments, some of which grow in severity over the years. The catch, of course, is that if an early ailment becomes severe, it may kill the patient, eliminating the need to fix the later ailments.

The way I see the economy, there are many hurdles that have the potential to inflict severe damage on the economy. Slide 6 shows a few of them. Some examples of other issues include lack of fresh water and erosion of topsoil.

In my view, we are right now reaching an affordability crisis. One way it manifests itself is as high commodity prices that fall and thus become low commodity prices. Falling commodity prices are likely to cause debt-related problems because of all of the debt incurred in their production. We may find financial problems, much worse than those experienced in 2008, back again.

Slide 6

Many others have focused on climate change. In their view, we can extract pretty much all of the fossil fuels that are in the ground, because prices will rise higher and higher, allowing this to be done.

If, in fact, prices fall after a point, then there is a good chance that we must leave most of them in the ground because of affordability issues. If this is the case, the situation may be very different: we may lose fossil fuel production in not many years because of disruptions caused by low prices.

We often think of affordability in terms of what a gallon of oil costs or in terms of how much a kilowatt-hour of electricity sells for. While these costs are one part of the problem, a big part of the affordability problem relates to big-ticket items, as listed in Slide 7. If customers cannot afford these big-ticket items, such as homes and cars, the economy loses both (a) the energy use that would be required to make these big-ticket items, and (b) the later energy use that these big items would require.

Slide 7

If we look at the data, we find that inflation-adjusted median income for families has been falling.

Slide 8

Part of this lower family income involves a smaller share of the population working.

Slide 9

When a person looks at the labor force growth split between men and women, there is a very different pattern. Men show a small downward trend over time; women increasingly joined the labor force, but this trend topped out in 1999, and became a decline since 2008.

Slide 10

Something we all are aware of:

Slide 11

Many fewer homes are now being built in the United States.

Slide 12

There has been a very different trend in auto purchases in the United States, Europe, and Japan compared to the rest of the world. In the developed areas, interest rates have been very low, and lenders have increasingly offered loans to subprime buyers. An increasing number of the loans are 7-year loans, and the loan to value ratio is often 125%. We seem to be creating a new subprime auto bubble. Based on our experience with subprime housing loans, this is not a sustainable pattern.

Slide 13

I am convinced that most economists have missed a basic principle regarding how economic growth takes place (Slide 14). I define efficiency in terms of what it takes in terms of human labor and resources to produce finished output, such as a barrel of oil or a kilowatt-hour of electricity. Are these finished goods becoming cheaper or more expensive in inflation-adjusted terms?

On Slide 18, note the change in the size of the output boxes, compared to the input boxes. Increased efficiency produces more output compared to the resources used; increased inefficiency produces less output compared to the resources used.

If an economy is becoming increasingly efficient, a given number of workers and a given amount of resources can produce more and more goods. This is good for economic growth. Growing inefficiency is a problem, because it quickly uses up both available worker-time and available resources. Many economists never seem to have gotten past the idea, “We pay each other’s wages.” Yes, we do, but if those wages are being used to encourage the use of increasingly inefficient processes, we go backwards in terms of economic growth.

Slide 14

If we look back historically, we can see a growing efficiency pattern with electricity, in the 1900 to 1998 period. As the price dropped, both consumers and businesses could afford more of it (illustrated with rising black “demand” curve). Part of the lower cost came from increased efficiency of electricity generation during this period.

Slide 15

If we look at the oil sector, since about 1999 we have had exactly the opposite pattern taking place. The cost of oil “exploration and production capital expenditures” has been rising at a rapid rate. This is an issue of diminishing returns. We have already extracted the easy-to-extract oil, and as a result, we need to move on to more difficult (and expensive) to extract oil. Thus we are becoming increasingly inefficient, in terms of the cost of producing the end product, oil.

Slide 16

As we move on to more expensive oil, the higher cost tends to squeeze budgets. The thing that is important is the fact that wages don’t rise sufficiently to cover the cost increase; in fact, the images I showed earlier seem to suggest that in the recent era of high prices, we have seen unusually slow growth in wages. The amount of wages is represented by the size of the circles in Figure 17. The wage circles don’t grow.

Slide 17 shows that as workers need to spend more for oil, and for the things that oil is used to make, such as food, the discretionary portion of their budgets (“everything else”) is squeezed. This shift in discretionary spending is what tends to lead to recession. The same principle works if consumers suddenly find themselves with higher electricity bills–discretionary spending is again squeezed.

Slide 17

The problem that squeezes all commodities at the same time is falling discretionary income. The amount of debt that can be borrowed also tends to fall as discretionary income falls. The combination leads to falling affordability for expensive goods, like new autos and new homes.

The price patterns for commodities of many types move together, reflecting a combination of rising cost of oil (because of higher extraction costs) and falling ability of consumers to afford the high prices of these goods. I have not included food on Figure 18, but many food prices have recently fallen as well.

Of course, the costs for producers creating these commodities have not fallen proportionately, and many have huge amounts of outstanding debt. Repayment of debt becomes difficult, as prices remain low.

Slide 18

Back at Slide 14, I talked about increased efficiency leading to economic growth, and increased inefficiency causing economic contraction. Because our leaders have not looked at things this way, they have encouraged increased inefficiency in many areas, as I describe on Slide 19. To some extent, this increased inefficiency is required. For example, as population grows in areas with low water supplies, the need for desalination grows. Also, pollution problems increase as we use lower qualities of coal and oil.

Slide 19

What are the expected impacts on the electricity industry and on natural gas? Are there any workarounds?

Let’s look at a few implications of the problems we now see.

In my view, low oil and natural gas prices are likely to be a huge problem for the natural gas industry, leading to the bankruptcy of many natural gas suppliers.

We cannot expect natural gas supply to grow. In fact, we cannot expect a coal to natural gas transition because the natural gas price won’t rise high enough, for long enough.

Slide 21

If we look at the history of US natural gas prices (using Henry Hub data), we see that prices have tended to stay low, after the 2008 spike. This was a great disappointment to those who built new natural gas extraction capability. They expected prices to rise, to justify their new higher costs. In my view, the continued low natural gas prices to some extent already reflect affordability issues.

Slide 22

The Marcellus Shale was perhaps the most successful of the new natural gas production, but it seems to now be topping out because of low prices (Slide 23).

Many producers will have their lending terms reevaluated using September 30, 2015 data. This reevaluation is likely to lead to bankruptcy of some producers, and cutbacks of production of other producers.

Slide 23

Coal use has been declining, as shown in Slide 24. Coal has some of the same problems as natural gas, as I will explain on Slide 25.

Slide 24

The basic issue is that coal prices are too low for most producers. Even if a particular producer has low extraction costs, this benefit is not enough to keep producers from bankruptcy. The problem that occurs is that coal companies are locked into high cost structures because of patterns that continue to persist from when prices were high. Lease costs are high; taxes and royalties are high; often debt was entered into, assuming that revenue would remain high in the future. Now revenue is lower, and there is no way to fix the “hole” that results from low prices. Production stays high, because each producer must produce as much as possible, to try to avoid bankruptcy for as long as possible.

Slide 25

Coal is in a sense ahead of natural gas, in terms of bankruptcies, with big bankruptcies already starting.

With prices as low as they are, there is little chance for a new producer to come in, buy the production facilities at a low price, and restart operations. A big issue is ongoing costs such as royalty payments that cannot be eliminated. Another is debt availability to support the new operations.

Slide 26

Bankruptcies are likely to interrupt supply chains as well. Part of the problem may simply be the excessively high cost of credit, for those members of the supply chain with poor credit ratings. Once a supply chain breaks, replacements parts may not be available. Other services that a company contracts for with outside suppliers may disappear as well.

As I note on Slide 27, customers may have financial difficulties. Those who remain in business will tend to buy less, so demand is likely to be lower, rather than higher. Companies producing electricity should not be misled by the rosy forecasts of the EIA and IEA regarding future demand amounts.

Slide 27

Slide 28 shows that industrial consumption of energy products has been falling since the 1970s, as industrial production has moved overseas. Now the dollar is high relative to other currencies, encouraging more of this trend. On a per capita basis, residential energy consumption is down, and commercial energy consumption is level. It is hard to see that this mix will provide very much of an upward trend in natural gas and electricity consumption in the future. (Note: Slide 28 shows energy of all types combined, including both electricity and fuels burned directly. This approach is used because there has been a shift over time to the use of electricity. This method shows the overall trend in energy use better than, say, an electricity-only analysis.)

Slide 28

The major ways subsidies for wind and solar PV are available are through greater government debt or through higher costs passed on to customers. There are now getting to be pushbacks in both of these areas.

Slide 29

In Europe, the cost of intermittent electricity tends to be passed on to consumers. Dr. Euan Mearns put together the chart shown in Slide 30 comparing price of electricity with the per capita wind and solar PV generation installed for European countries. There is a striking correlation. Countries with more installed wind and solar PV tend to have higher electricity prices for the consumer.

Slide 30

Given the problem with commodity producers not being able to collect high enough prices for their products, and the large number of resulting bankruptcies, a person comes to the rather startling conclusion that the ideal structure for electricity providers in today’s economy is that of a vertically integrated utility. In other words, an electric utility should directly own its suppliers, as well as transmission lines and everything else needed to produce and distribute electricity.

Utilities have traditionally had the ability to price on a cost-plus basis. With vertical integration, the utility can use its pricing ability to keep prices for fuel producers from falling too low, and thus sidestep the problem of bankruptcies. To the extent that the required price for electricity keeps rising, it will tend to pressure discretionary spending. (See Slide 17.) But at least grid electricity will be among the last to “go” under this structure.

Slide 31

Black Hills Corporation lists the many electricity-generating facilities it owns (coal and natural gas), and the places it has arrangements to sell this electricity as a utility. The Black Hills Corporation indicates it has had 45 years of dividend increases. This increase in dividends is in stark contrast to the many coal and natural gas producers that are currently near bankruptcy, as a result of low coal and natural gas prices.

Slide 32

How does one resolve the conflict between industrial companies wanting to generate their own electricity (for a variety of reasons) and the need to have an electric grid for everyone else? It seems to me that we have to keep in mind that having an operating electric grid for everyone else is absolutely essential. Without the electric grid, gasoline stations would stop pumping gasoline and diesel. Transportation would stop. Electric elevators would stop. Treatment of fresh water and sewage would stop. Companies everywhere would lose their consumers. The economy would quickly come to a halt.

With our current affordability problems, we are in danger of losing the electric grid. That is why it is essential that those who opt out not be given too large a credit for providing some or nearly all of their own electricity. The credit given to industrial companies should reflect the savings to the system, no more.

Slide 33

One concern is the bankruptcy of peaker plants, if their use is significantly reduced by, for example, the use of solar PV. If these peaker plants continue to be needed for balancing purposes, this may be a problem. Another concern is the rising cost of grid transmission for those who continue to get their electricity from the grid.

Slide 34

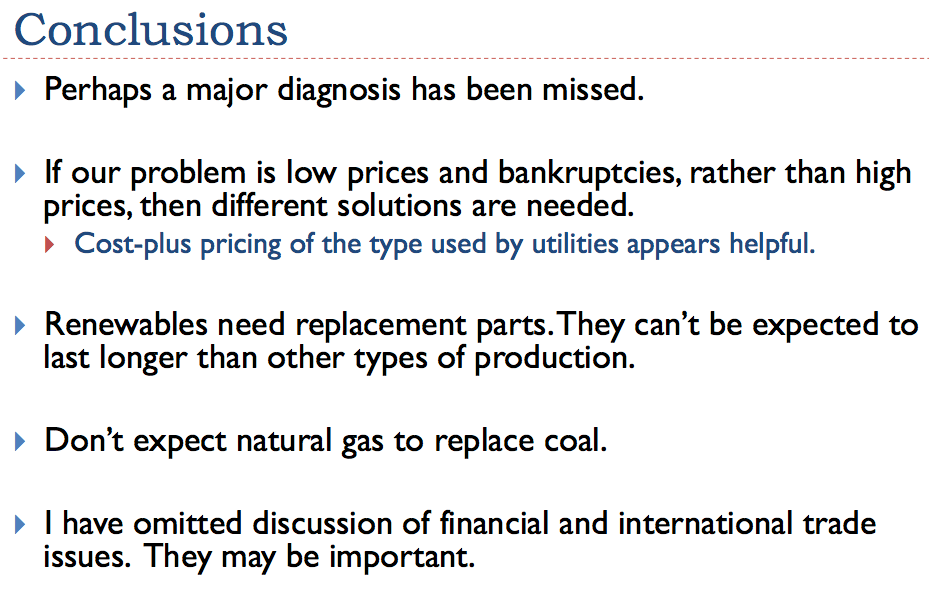

To sum up, the story we read from most sources is so climate-change focused, a person wonders if there aren’t other issues that are important as well. Most observers have overlooked the importance of low commodity prices, and the impact that they can have on coal and natural gas producers’ ability to produce the fuels that are needed by electric utilities.

Too much faith is being placed in natural gas, as the fuel of the future. And too much faith is being placed on intermittent renewables, without fully understanding their costs and limitations.

I haven’t tried to address the many indirect problems arising from many bankruptcies. These may be severe.

Slide 35