In 2008, I said that an energy shortfall was likely to make it more difficult to pay back debt and to fund government promises, such as Social Security. Now there has been a big step down in US oil consumption:

Figure 1. US per capita oil consumption in the US dropped dramatically starting in late 2007, according to data of the US Energy Information Administration.

The information we hear about GDP growth would make a person think that the economy is almost sailing along. It seems to me that if we look at the situation closely, per capita spendable income in $2005 dollars has dropped significantly, if one considers oil price changes and related drops in credit availability. More importantly, a model I developed suggests a serious gap has developed between what the government is now spending and what can reasonably be funded through tax revenue.

Is this really an energy decline?

I am sure some people will say that this cutback in oil usage was voluntary. We couldn’t afford the oil. Or it was caused by recession. But it seems to me that this may be typical of what a decline in oil usage looks like in the future. The problem isn’t that the oil isn’t there–the problem is that the economy can’t afford high-priced oil that is available.

If we really could afford very high-priced oil–for example, $300 barrel oil–there would be a lot of unconventional oil that could be developed, and oil supply wouldn’t be a problem. Instead, if oil prices rise very much (Dave Murphy says $85 a barrel is high enough), people cut back on other expenditures, and recession ensues.

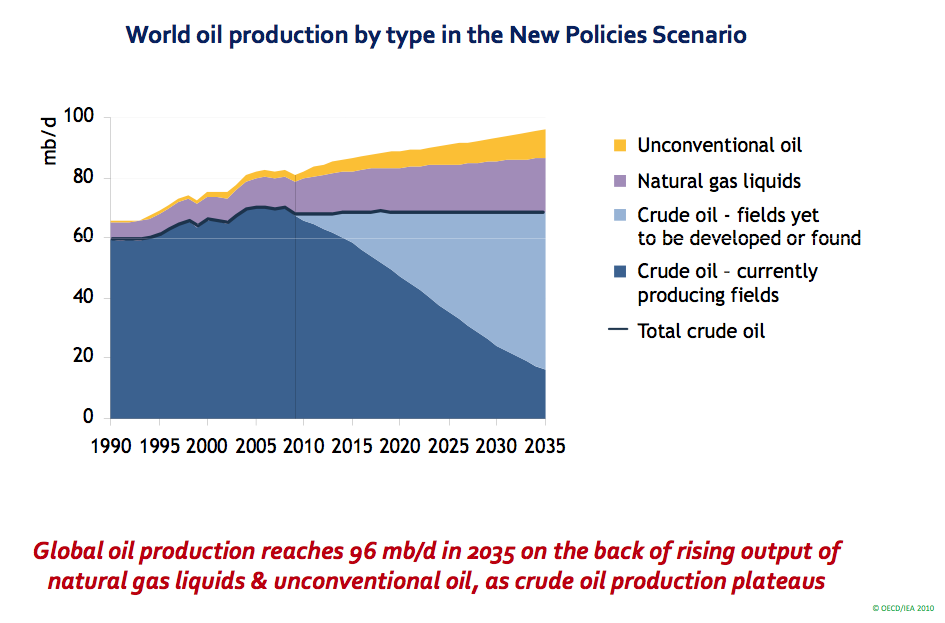

Going forward, it is difficult to see oil availability getting much better. World oil availability is expected to remain quite flat, according to projections made by the International Energy Administration in is World Energy Outlook 2010 issued in November 2010. Demand from China, India, and oil producing nations is expected to continue to rise, leaving less and less oil for developed countries, such as the United States.

What is the problem with funding future promises, such as paying social security to retirees and repaying debt, if the economy isn’t growing?

If the economy is growing, the future holds more than the present (in terms of resources extracted from the earth, goods, and services). A payment to repay debt with interest, or to benefits to the elderly, becomes easier, because there are more goods to divide up in the future. Pretty much everyone can get what was promised, with goods and services left over:

Figure 2. A growing economy makes it easy to fund promises such as debt and social security.

But if resources are shrinking, and as a result the economy is flat or even declining, such promises become much more difficult to fund. Promises that seemed reasonable when they were made, are likely to seem less reasonable when people have to contend with reduced resources in total.

Figure 3. If the economy is declining, it is difficult to have enough left over for "other things" after debt has been repaid with interest and other promises have been paid.

What is happening now?

It seems to me that people’s incomes are not doing well at all. (Click on images for larger view.)

Figure 4. US Personal Income Breakdown from US Bureau of Economic Analysis.

If we look at US Bureau of Economic Analysis (BEA) data, it shows that private industry wages are lower now than they were in late 2007 and in 2008, even without adjusting for the higher population now and the impact of inflation. Proprietors’ income (including that of farmers) is also lower, on a similar basis. What has increased is government wages and transfer payments.

There are at least two other issues making people feel poorer. One is the higher cost of oil. Oil is used by all segments of the economy (including governments, businesses, and consumers). I would expect that quite a bit of this higher cost will indirectly come back to consumers, through higher taxes and higher costs of products, if not paid directly by consumers.

The other issue making people feel poorer is a reduction in the amount of “domestic non-financial” debt outstanding–the sum of home mortgage debt and consumer credit (including credit card and automobile debt) , as defined by the Federal Reserve.

We all remember a few years ago, when many people were using their homes as “ATM” machines–taking out higher loans (s0me times with lower interest rates) as home values increased. They used the additional cash for many different things–home improvements, or a new car, or a vacation. Growing credit card debt and easy availability of auto loans also acted to make incomes “go farther”.

The amount of consumer credit reached a peak and began to decline at precisely the same time that world oil production (“liquids”) hit its high point–both in production and in oil price–in July 2008:

Figure 5. US Consumer Credit Outstanding, based on Federal Reserve Z.1 data.

The pattern for outstanding balances for home mortgages follows a similar pattern, rising as long as oil prices continued to rise, but beginning to fall at approximately the same time.

Figure 6. US home mortgage amounts outstanding, based on Federal Reserve Z.1 data.

While one could argue that all of this is a coincidence, oil and other energy products have a definite stimulating impact on the economy; they help hold bubbles up and keep discretionary spending high. There are many who argue that debt is something that financial regulators are able to increase and decrease at will, but if things aren’t looking so good–housing are prices down, job prospects are bleak, and loan defaults are high–I would argue that loans amounts can be expected to decrease rather than increase, and the economy will have to make do with less credit, rather than more.

Besides the connection shown in Figures 5 and 6 between oil prices and debt, higher oil prices were the major factor in the Federal Reserve Open Market Committee (FOMC) raising target interest rates in the 2004 to 2006 period. These higher interest rates no doubt helped prick the sub-prime mortgage bubble, leading to the decline in home prices starting in 2006. What happened is that oil prices were rising, leading to inflationary impacts, as far back as 2003. In trying to fight the inflationary impact, the FOMC raised target interest rates. Steve Ludlum (also known as “Steve from Virginia”) traces the connection between target interest rates and oil prices through the minutes of the FOMC in this Oil Drum post.

Income Adjusted for the Impact of Oil Price Changes and Changes in Credit Availability

There is no perfect metric for estimating how much money people have to spend, but it seems as if at least some adjustment needs to be made for the impact of higher oil prices–most of which eventually seems likely to fall back through to the consumer–and reduced home mortgages and consumer credit. (Click for larger image.)

Figure 7. US per capita income measures, using total Personal Income in 2005$ as a base. Personal income is from BEA. See text for adjustments.

In the above graph (click for larger image), per capita income in 2005 $ is shown on three different bases. The blue line, called Personal Income, is directly from the BEA. (It is the amount for which I showed a breakdown in Figure 4.) Of the three lines shown, it shows the least recent drop-off.

The red line in the above graph is the same personal income amount (in 2005$, on a per capita basis) adjusted for the increase (or decrease) in mortgage and consumer credit. Thus, it reflects the extra funds available when people were able to use their homes as ATMs in the 2001 to 2006 period. As these funds were spent, they tended to have a further stimulating effect on the economy, because it gave consumers the impression they could afford more expensive homes. Also, if consumers bought more goods with these funds, they would tend to increase jobs in the sectors where more goods were purchased. If it hadn’t been for this boost, the impact of the 2000 recession would most likely have felt much worse, much longer to consumers.

Recently, the red line has dropped a bit below the blue line, indicating that a contraction in debt is having a small negative impact. And at least equally importantly, the stimulating impact of growing debt that we had all the way until 2008 (see Figures 5 and 6) is gone.

The green line takes the red line and adjusts for oil cost (again adjusted to 2005$), so that what is shown is in total income, adjusted for both oil cost and credit. Clearly, both the red and green lines are showing a big step down in current “income” in recent years–about 13% or 14%–relative to the peak in early 2006. The unadjusted blue personal income line gives the impression that personal income (on a per capita, 2005$ basis) is approximately flat with 2006.

Comparison to Government Funding Needs

There has been considerable publicity about whether and how the US federal government tax deficit can be fixed. But this is only the tip of the iceberg. State and local programs are in need of additional funding, too. Also, there are various programs that may or may not be fully reflected in the other figures–such as unemployment insurance funding, structural problems with Medicare and Social Security funding, and potential bailouts for government agencies offering home loans.

One way of looking at the amount of the shortfall is to look at what the BEA reports regarding total US government expenditures and receipts. Note that since these amounts are totals, they reflect a combination of different types of taxes and government programs, and the taxpayers are of many different sorts.

Figure 8. Ratio of US government receipts and expenditures to personal income, based on BEA data.

Even though government revenue includes business taxes, in Figure 8 I compare both revenues and expenses to personal income, since I would expect that higher taxes on business will to a significant extent be passed on to consumers through higher prices. If instead higher oil prices lead to lower corporate profit, lower dividends, and layoffs, these too will be felt in the personal income sector.

This comparison shown in Figure 8 produces fairly high indicated ratios to indicated personal income, with expenditures currently near 45% of personal income, and expenditures rising far above receipts.

But I think even this may give too rosy a view of what income is available to pay for this shortfall. It seems to me that the transfer payment portion of Personal Income is really part of the problem, not a source of higher taxes. Likewise, all of the government employees are also part of the problem, although of course one can charge government employees higher taxes. One thing that I noticed that might give an indication of the nature of the problem is the fact that government expenditures of all types (including social security, Medicare, and unemployment insurance) exceed wage and salary disbursements from private industry (Figure 9).

Figure 9. Some annualized quarterly seasonally adjusted amounts using BEA data.

One can argue as to what base might be reasonable to compare needed tax increases to, if Personal Income in total is too high a base. As one approximation–and I am not sure it is the best one–I looked at what I call “Total Non-Government Income”. This is the sum of the first four categories shown in Figure 9.

Figure 10. Per Capita income in 2005$ adjusted for credit changes and oil price changes.

Figure 10 shows what the trend in per capita, 2005$ income looks like, if we use as our base the sum of (1) Wage and salary disbursements from private industry, (2) Proprietors income, (3) Personal interest income, and (4) Personal dividend income. If one compares Figure 10 to Figure 7, one sees that the recent drop in per capita income is even greater on the Figure 10 basis than using Personal Income, with all the government programs included as a base. (The population base is left unchanged in Figures 7 and 10, which is the reason for the big drop in averages in Figure 10.)

In Figure 11, I compare government revenues and expenditures to the personal income amounts that correspond to the red line in Figure 10–that is, the personal income amounts, adjusted by changes in credit amounts (but not by oil cost changes). This line reflects very approximately that fact that the people who will ultimately need to pay higher taxes to fix the current funding problems represent only a subset (and a declining subset at that) of those generating Personal Income. Furthermore, these payers are experiencing declines in credit outstanding. They are likely also experiencing declining home values, which is part of the reason for the lower outstanding mortgages. All of this makes them less able to pay higher taxes.

Figure 11. Ratio of government receipts and expenditures to lower personal income estimate.

Figure 11 represents something closer to what I think is actually happening than what is shown in Figure 8. In Figure 11, government receipts (the blue line) are staying relatively constant relative to the base, while in Figure 8, government receipts are declining relative to the base. In other words, while government receipts are down, it seems to me that a good part of this decrease is because the base that is being taxed is down. Some of this reduction is due to reduced home values that is feeding into lower municipal tax revenues.

We can’t know exactly what the current effective tax rate is, if all types of programs are combined and compared to the income base that is indirectly currently funding it, but we can estimate a rough range based on the indications of Figures 8 and 11. Based on Figure 8, (which uses all Personal Income as a base), the current effective tax rate is at least 30%, and based on Figure 11, (which excludes some government income from the base, and also adjusts for changes in credit availability), the current effective tax rate is perhaps as high as 50%.

The apparently high level of embedded taxes now makes it very difficult to keep raising the tax levels. If taxes are already effectively at something close to the 50% rate, how much higher can taxes reasonably be raised? All of these calculations are very rough, but gives an idea why raising taxes to fix our current funding shortfall is problematic.

It seems likely that a reduction in expenditures will be needed in addition to tax increases, to bring revenue and expenses to a situation where the better match. Continued huge borrowing is not likely to work well, because of the issue illustrated in Figures 2 and 3.

Further Thoughts

The idea of indirect taxes may seem a bit odd. Clearly we pay income taxes, social security taxes, and state and federal taxes. But we also indirectly pay taxes included in the price of everything we buy, and even in contributions we make. Some of these taxes are obvious, like gasoline taxes and sales taxes, and some are buried in the price of the product we buy, because the business pays various taxes, and considers these taxes in figuring its overall pricing. Even if we make a contribution, say to a church, part of that contribution will go to pay the taxes of the employees of the church.

The figures I show are for the US. I expect that the European countries with all of the current debt problems would likely have similar or worse values, if calculations were done for them.

I think the way GDP is calculated today misses many of the linkages as to what is really happening. I know my model is not exactly right–but I hope it gives some insight as to what is really happening, as oil prices and the credit markets interact to affect the economy.

As I look at this model, one question comes up: “What if a similar oil price run-up occurs again, followed by more recession, and even more reduction in lending?” Governments are already spending far more than they take in. The high spending already in place, and the large gap between revenue and expenditures, makes it clear that there isn’t much room for a repeat stimulus program. The next time around could be much worse!

{kind=link}

Pingback: Oil limits lead to state budget squeezes | Our Finite World

<>

Hi, Len. If you place the conversation in terms of money, the conversation loses its validity pretty quickly as fiat currencies blast out of control, especially in relation to each other. I like your end point of when imports stop (maybe I don’t “like” the endpoint, but there it is). Odum suggested that we would eventually have to make do with about 70% less emergy globally as we fall back to renewable resources. In the US that 70% could come more immediately, since we’ve gotten far out on a limb using everyone else’s oil.

http://upload.wikimedia.org/wikipedia/commons/c/c5/US_Oil_Production_and_Imports_1920_to_2005.png

Well, you raise an interesting point (fiat currency changes value rapidly) however, if you insist on having the discussion I proposed without considering prices and other economic issues, all that can be said is “In my opinion xxx will happen” which is not fruitfull at all. What’s needed (and proposed above) is to control for changing currency as part of the calculation, which should be do-able.

Without price “to be paid” for resource-based energy, nothing is knowable because as we all know from discussions on theOilDrum etc., how much resource is available for recovery depends entirely on a) market selling price b) cost of inputs to the recovery process and c) EROEI of the recovery process.

Agreed it’s complex, but either we do it or do nothing.

Prices should always be taken into account–both nominal prices and real prices, i.e. corrected for inflation.

Within five years I expect a huge increase in the rate of inflation.

I commend your efforts to expand the discussion beyond “is oil supply peaking?” to “well, then what?”. What seems meaningful to me is to attempt to quantify factors and apply those results to some selection of measurements to try to establish “the range” of possible outcomes, with the range primarily established by society’s responses to problems, which is essentially un-knowable.

It “sounds right” to me to pick a point in future, then try to apply hard math to the factors to try to gain a look at what things might look like then. To me, that point should be the end of petroleum imports to N. America, which is a specific time in future which should be a fairly knowable date. Arrive at that date (range) by applying multiple regressions of economic (and related, eg. demographic) changes domestically, in the exporting world, and in the “competing for imports” world. eg. “What price can domestic N. Americans possibly pay for oil above domestic supply 1 year, 5 years, 10 years, 20 years out?. What price will competitors be able to pay? What supplies will be available? When does importation drop to zero, and what will the domestic price be then? How much reserves will then remain domestically at that price? etc.”

Then having arrived at that date, establish what supplies will be available to the market, and what can be accomplished with those? Apply a range for high or low renewables substitutions. Then apply a range for that part of supplies priority appropriated to produce exported food and other trade products required to maintain minimal foreign trade for essential commodities etc. Factor in domestic population changes (size, demographics, etc.).

Then determine what the per-capita GDP would be, and what historic era that compares to.

Then, given only the diferences in relative knowledge from now to that historic era, what could life be like in that circumstance?

A huge project I suppose, but interesting.

I think that is one approach. It assumes all of our current systems “stay together”. If they don’t, then the discontinuity arrives in a very different way, sooner (for example, financial system crash->electric utilities companies all fail->no oil products delivered, even from local sources). So your approach would seem to give more or less an upside estimate–if things work out as we hope, type estimate. If something truly bad happens, we really have much less capability to make plans for it.

Gail:

I always enjoyed your posts on The Oil Drum, but never commented. You, IMHO, maintain a good balance between peak oil and the financial implications of it. After all the technical discussions of production, reserves, exports vs internal consumption, etc most folks want to know how this will affect them.

While I enjoy many of the posts and comments on The Oil Drum I often walk away thinking only half of the story has been told. From history we are taught that leadership involves not offering false hope. Three days after Winston Churchill became Prime Minister he told the people, “I have nothing to offer but blood, toil, tears and sweat.” and later in the day was quoted as saying, “Poor people, poor people. They trust me, and I can give them nothing but disaster for quite a long time.”

Where are the leaders who can rally us and give us hope down the road but in meantime tell us hardship must first be endured?

Thanks for your efforts and glad you found another outlet to offer your insights.

Thanks for commenting! I think some people are feeling more and more threatened by where we are now, and are uncomfortable thinking about implications. This makes it harder to try to present the full picture, but I still think it is something that needs to be done.

Gail,

Of course you are correct: People do not want to think about unpleasant futures. Indeed, they will both consciously and unconsciously resist such thinking.

On the average, psychoanalysis takes anywhere from six to eight years to be finished. Short of psychoanalysis (and yes, I have been psychoanalyzed) for all, I do not see what we can do to change most people’s minds.

On the other hand, the U.S. has shown remarkable resilience in responding to crises (Civil War, Great Depression, World War II, the Cold War) in the past. Perhaps when the crisis is rubbed in our noses, even the economists will get rid of their outmoded ways of thought and premises.

I think the correct question to ask would be, can America afford to import 600 billion dollars of oil year after year ? If this problem where fixed, the deficit would fix it’s self.

Plan the end of the production and sales of new personal fosil fuel passenger vehicles world wide

“What if a similar oil price run-up occurs again, followed by more recession, and even more reduction in lending?”

We can’t pay the bill even now. Here’s the big picture; $670,000 in debt per family.

http://www.usdebtclock.org/

I think the US is praying that they’re last in the come-to-Jesus moment after the PIIGS and the disbanding of the EURO. The problem is, the populace of these countries is beginning to catch on and demand the Iceland solution of demanding default of the bankers–not bailing out the wealthy bankers. By the time the US has to face the music, it will be much clearer to the populace what needs to be done. We will default. But we will still have to pay for oil, and that will cause massive inflation in commodities, especially with a bankrupt dollar. So our ploy is to extend and pretend, and be last in line for Madame Guillotine, praying for universal default before it becomes our turn. Might still makes right.

The FIRE economy is a zombie. After universal default, who still has the oil will become very clear as trade breaks down.

If something cannot go on indefinitely, then it won’t. Business As Usual cannot go on indefinitely–maybe for another decade or two, but in 2030 we’re going to live in a very different world from the one people have lived in since 1945.

Nobody knows the future. Economic forecasts make weather forecasts look good by comparison. Nevertheless, I’ll venture onto a couple of SWAGS:

1. Real economic growth is over for the U.S. Real per capita disposable income is roughly where it was ten years ago. Because of declining oil production and rising oil prices, I expect real U.S. GDP per capita to decline for at least the next thirty years. I hesitate to put a number on the rate of this decline, but I think it will be greater than 2% per year and less than 10% a year, on the average, between now and 2040 for the U.S.

In the long run, fiat currency is always wiped out by inflation. Current rates of inflation as shown by the GDP deflator for the U.S. are a bit over 2% per year. As government deficits grow, and as QE2 is succeeded by QE3 . . . QEn, I expect the rate of inflation to increase–slowly at first, then higher and higher. Whether we ever get to hyperinflation is impossible to say. But note that a continued 10% rate of inflation will cut the value of the dollar in half in just 7.2 years.

I am not a fast-crash doomer, but I do think we’re in for hard times comparable to those of the Great Depression–and probably worse than the Great Depression within fifteen years. I do not think we will make a successful transition away from fossil fuels, though it would be technologically possible to do so by mobilizing all of the U.S. resources to do so. What we face is political limits, rather than limits imposed by the second law of thermodynamics or limits imposed by finances. IMO the U.S. will be largely a command economy within twenty years, with emphasis placed on defense and maintaining internal order. Worst case scenario is George Orwell’s 1984. Best case may be a fumbling fascist dictatorship such as that of Mussolini.