I was asked to give a talk to a committee of actuaries who are concerned about modeling the financial future of programs, such as pension plans, given the energy problems that are often discussed. They (and the consultants that they hire) have been using an approach that puts problems far off into the future. I was trying to explain why the approach that they were using didn’t really make sense.

Below are the slides I used, and a little explanation. A PDF of my presentation can be downloaded at this link: The Mirror Image Problem.

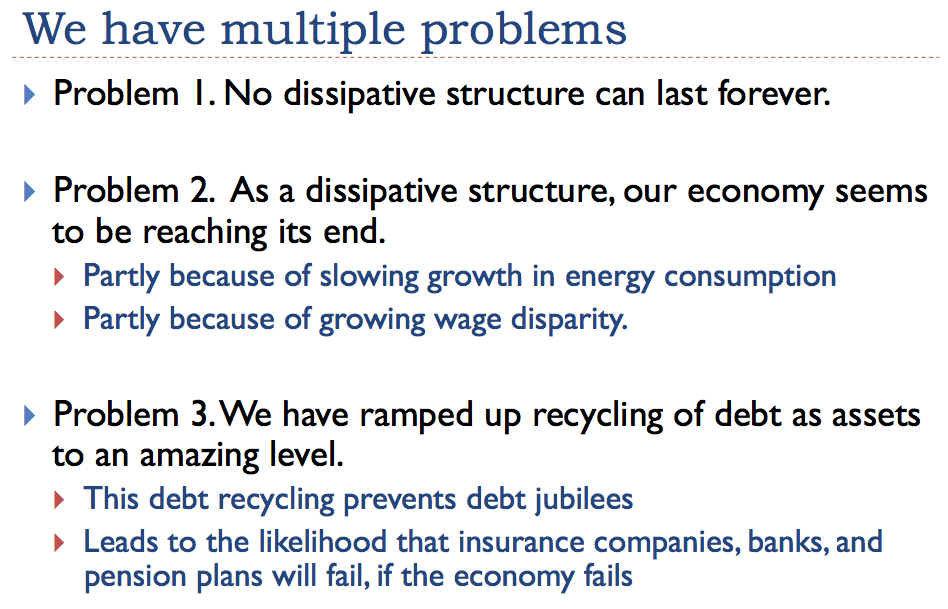

Slide 1

FCAS stands for “Fellow of the Casualty Actuarial Society”; MAAA stands for “Member of the American Academy of Actuaries.” Actuaries tend not to be interested in academic degrees.

Slide 2

I try to explain how a more complex situation can be hidden in plain sight.

Slide 3

It is not obvious that both the needs of energy producers and energy consumers should be considered.

Slide 4

If we look back at what the discussions of the time were, we can see when remarks were that prices were too high for consumers, and when they were too low for producers. See for example my article, Oil Supply Limits and the Continuing Financial Crisis and my post, Beginning of the End? Oil Companies Cut Back on Spending. This latter article shows that companies were already cutting back on spending in 2013, when prices appeared to be high, because even at a $100+ per barrel level, they still were not high enough for producers.

Slide 5

Oil companies tend to extract the cheapest and easiest to extract oil first. Eventually, they find that they need to move on to more expensive to extract fields–even with technology enhancements, costs are rising. There seems to have been a step up in costs starting about the year 2000. The above chart is by Steve Kopits. This EIA data (in Figure 10) also shows a pattern of sharply rising costs about the same time.

The problem, of course, is that wages have not been spiking in the same pattern. As a result, we encounter the problem of prices being either too high for consumers, or too low for producers, as we saw on Slide 4.

Slide 6

The economy is “built up” from many different parts. It includes governments, businesses, and consumers. It also includes people with jobs in the economy, and individuals and businesses making investments in the economy. It gradually changes over time, as new businesses and new laws are added, and as other changes are made. The wages that workers earn influence how much they can spend. The economy keeps re-optimizing, based on the goods and services available at a given time. Thus, slide rules are no longer commonly sold; it is not easy to buy horse-drawn carriages. This is why I show the economy as hollow.

Slide 7

Let’s talk a little about how economic growth occurs in a networked economy.

Slide 8

Clearly, tools and technology can be very helpful in creating economic growth. I am using the term “tools” very broadly, to include any kind of structure or device we build to aid the economy. This would even include roads.

Slide 9

Making tools clearly requires energy. Operating these tools very often requires energy as well, such as energy provided by diesel or electricity. With the use of tools, humans can more efficiently make goods and services. For example, if small parts need to be transported to a business, it is nearly always more efficient to transport them by truck than to deliver the parts by walking and carrying these parts in our hands. Clearly, tools such as trucks also allow us to do things that we could never do otherwise, such as deliver large and heavy parts to users.

Economists often talk about “rising worker productivity,” as if this rising productivity came about because of actions undertaken by the worker–perhaps attempting to work faster. Another possibility would seem to be taking a course on how to work more efficiently. We would expect that most of the time this rising productivity would come about as a result of the use of additional tools, or better tools. Thus, it is really the tools, and the energy that they use, that are acting to leverage worker productivity.

Slide 10

It is not intuitive that adding tools requires debt, unless a person stops to realize that it generally takes quite a bit of resources to make a tool (human labor, plus metal ores and energy products). Using these tools will provide a benefit over quite a long period in the future. A business making these tools has a problem: it must buy the resources to make the tools and pay the workers, before the benefit of the tools actually comes into existence. It is necessary to have debt (or a debt-like financial instrument, such as shares of stock), to bridge this gap.

This same kind of mismatch occurs, even if goods being purchased with debt are not really tools. For example, a home purchased with debt and paid for with a mortgage is not really a tool. The buyer needs to pay interest to a bank or some other intermediary, in order to finance the home over a period of years. Thus, part of the worker’s wages is going to the financial system, rather than to obtain the goods and services he really wants. Financing the home with debt is generally more convenient than paying cash, however. Because of the convenience factor, debt is generally essential for most home purchases. If a new home is being purchased, the builder who builds the home will need to buy lumber and pay workers when the house is built, rather than over the lifetime of the house. Because of this, debt is necessary so that the builder will have the funds to buy lumber and pay the workers.

Analysts coming from engineering and other “hard sciences” often miss this need for debt. Since a person can’t see or touch it, it is easy to think it isn’t needed. Interest payments are important, because they transfer goods and services made by the economy away from workers to other sectors of the economy (such as the financial system, retirees, and pension programs). Thus, they represent a different use for energy products, other than making goods for the use of workers.

Slide 11

Slide 11 shows how an economy produces a growing quantity of goods and services. The three types of inputs I show are

- Energy products and other resources

- Workers

- Tools

I perhaps should include government services, such a roads, as well. If I did, I would show a fourth box down the side. Such a box didn’t fit easily on the slide, so I left it off.

Slide 12

As I noted in Slide 10, it takes debt to be able to have enough funds to pay everyone who makes tools, and in fact, other goods (such as vehicles and homes) that we pay for over the life of the goods. In Figure 12, I show that at least some of those providing inputs to the process receive “Future goods and services, plus interest,” rather than goods that have already been made. In this way, the system distributes more goods and services than would be available through the barter system.

In my notes to Slide 11, I commented that I perhaps should have included a government sector, as a fourth box down the side. That comment is also true here. On Slide 12, we are distributing the benefit of goods and services created, so we probably need to add even more boxes down the side. One of them would be “Payments Under Funded Pension Programs.” Another box would represent payments to individuals who sell appreciated shares of stock and real estate, and hope to buy goods and services with the proceeds of these sales. In the government sector, we would need to be certain that the category is large enough to include goods and services distributed to retiring “Baby Boomers” under Social Security and similar unfunded retirement programs.

People who do modeling can easily lose sight of the fact that we really live in a “calendar year” world. Each year, we can extract only so much oil, coal, gas, and metal ores, and use those resources to make goods and services. These goods and services are generally available for sale the same year. It is easy to add layers and layers of promises of “future goods and services” to the system, without ever checking to see whether the resource base provides enough resources to make promised future distributions of goods and services possible.

Slide 13

Often, it is the owners of resources who are paid in stock or debt. Workers are paid in money (which is a form of debt), but they very often want to spend most of it on goods and services that they can use today.

We can think of debt (and balances in bank accounts) as promises for future energy, and the goods it makes possible. Of course, if that energy isn’t really available, the promise is an empty promise.

Slide 14

There are many kinds of debt, and reciprocal obligations. This is a chart I found recently, giving one person’s view of the amount outstanding today, including a very large amount of derivatives. All of these debts make the assumption that energy will be available in the future so that goods and services can be created to fulfill these various types of promises.

Exeter Pyramid of Debt, created by Dr. Iris Mack.

Slide 15

Debt becomes very important in the whole system, because the higher the debt level, the higher that wages can be. Also, with a higher debt level, commodity prices, such as oil prices, can also be higher. Because more debt seems to make almost everyone richer, governments go out of their way to encourage additional debt, and more debt-like instruments. Of course, if interest rates go up, rather than down, interest on this debt becomes a big burden for borrowers. On Slide 12, the higher interest rates transfer a larger share of goods and services away from workers to other sectors of the economy (such as pensions).

Slide 16

Shrinking debt levels are similar to governmental cutbacks for programs. (In fact, governmental cutbacks in programs often result from shrinking debt levels.) Then fewer workers can be hired, and fewer goods and services can be purchased. The economy tends to shrink–similar to what happened during the 2008-2009 recession.

Slide 17

We often hear about “Supply and Demand.” A better name for “demand” might be “amount affordable.”

I mentioned in previous slides that wages and the amount of debt increase are important in determining the amount affordable. Other items that have a bearing are Item (3) the level of the dollar relative to other currencies, and Item (4) the extent to which productivity is rising. If the dollar is high relative to other currencies, the price of oil tends to be low, because those buying goods made with oil in non-US dollar currencies find the goods expensive.

Slide 18

Slide 18 illustrates the very significant impact that changing interest/debt levels can have on oil prices. Although I don’t mark the point on the graph, the peak in oil prices in 2008 came when US debt levels on consumer loans and mortgages started to fall. (See Oil Supply Limits and the Continuing Financial Crisis for details.) The US began Quantitative Easing (QE) in late 2008, with the intent of lowering interest rates and making debt more available. It was not long after it began that oil prices began to rise. Once QE was discontinued in 2014, other currencies fell relative to the US dollar, and the price of oil again fell.

Slide 19

The situation we have now is very much like a Ponzi Scheme. We need to keep adding more debt to keep wages and commodity prices high enough. At the same time, interest rates need to stay very low, to keep payments manageable, and keep the whole system from collapsing.

The balance sheets of insurance companies, banks, and pension plans include much debt. If these institutions are to make good on their promises to those with bank accounts, insurance policies, and pension plans, it is necessary for this debt to be repaid with interest. Back many years ago, debt jubilees were often given to selected debtors. These are out of the question now, because banks, insurance companies, and pension plans depend upon the future payments that this debt represents.

Slide 20

We like to think that improved technology can add more and more benefit. In fact, technology seems to reach diminishing returns, just as almost any other type of investment does. We make the easy changes (smaller cars, for example) first. Later changes tend to be more incremental. Because of this pattern, we can’t count on huge future changes in technology saving us.

Slide 21

Most people do not realize that the laws of physics determine the way that markets work–for example, the prices at which sales take place, and whether or not there are enough suppliers of a given product in the market place. They assume that as we reach limits, markets will always work as they have in the past. This seems unlikely.

Slide 22

Physics is often taught in terms of what actions are expected in an “isolated” or a “closed” system. In fact, the earth receives energy from the sun. The economy also obtains energy from stored fossil fuels and from uranium. Because of these energy flows, the rules of an “open” system are more appropriate. These have only been studied in recent years. Ilya Prigogine received a Nobel Prize in 1977 for his work on dissipative structures.

What is surprising is that dissipative structures are always temporary. They grow for a time, but eventually collapse. We know that plants and animals have finite lifespans; generally new similar plants and animals replace them. It is less obvious that systems such as ecosystems and economies have finite lifetimes.

Slide 23

Figure 23 shows my idea of how the dissipative structure of an ecosystem might be represented. Its inputs include solar energy, water, air, minerals from the soil, and recycled waste products from plants and animals. There are no real waste products from the system, because waste products are recycled. Ecosystems tend to collapse, when very sharp fluctuations occur. For example, forest fires tend to occur when a large amount of waste wood has accumulated and weather conditions are dry. (Perhaps dry wood and leaves, if they do not degrade rapidly enough, might be considered a temporary waste output that can lead to the demise of the ecosystem through fire, when conditions are right.)

Slide 24

Figure 24 shows my idea of how the economy might be represented as a dissipative structure. One critical part is “other energy,” which makes the economy act much like a rocket. Another critical part of the economy is “tools and technology.” Tools and technology allow the various inputs to be used, and the economy to grow. In a way, they are parallel to the biological systems that allow plants and animals to grow in ecosystems.

With human economies, we have multiple problems that can occur:

[1] Quantity of resources needed for inputs falls short

[2] Population of humans rises disproportionately to inputs of energy and other resources

[3] Waste outputs of various types become a problem

Growing debt is one of the waste outputs. Since we voluntarily seek out debt, we think of debt as an input. But if we think about the situation, debt is really an adverse output. Required interest payments tend to pull funds out of the system that could otherwise be used to pay workers. Also, the rising use of debt tends to concentrate the ownership of “tools” among the already wealthy. Debt can grow for a while, but it has limits, because of the adverse impacts it creates for the economy.

Growing wage disparity occurs because of the increased specialization required by ever-rising use of tools and technology. Some people receive the benefit of advanced education and learning to use tools such as computers; others receive much less benefit. As a result, their wages lag behind. Wage disparity is another limit of the system. If a large share of the workers cannot afford to buy the output of the economy, “demand” falls too low, and commodity prices tend to fall.

Distorted prices (shown on Slide 24) have to do with the changes to prices that occur, both because of added debt, and because we are reaching limits. Prices are not the same as they would be in a pure barter economy. Added debt allows prices to be much higher. As we reach limits, prices can fall below the cost of production. Suppliers continue to produce energy products, at least for a time, until the low prices become a real problem.

Slide 25

There are many reasons why an economy, which acts like a rocket, cannot continue forever.

Many readers have heard of “Energy Returned on Energy Invested” (EROEI). This is a favorite metric of many energy researchers. It is calculated by dividing Energy Out of a system by required Energy Inputs. As I show on Slide 25, EROEI looks at one part of one problem that economies encounter. There are many other problems and parts of problems that EROEI doesn’t consider.

Slide 26

Many believe that renewables can replace “Other Energy.” One reason for this belief is the fanciful claims by some researchers. Another reason for this belief is the apparently fairly favorable EROEI calculations that seem to occur when these devices are examined. These calculations are very limited. They don’t examine the many adverse impacts of adding tools and technology, and the rapid rise in debt that would be required.

Slide 27

Trying to run the economy on solar electricity alone (or solar plus wind plus water) is a futile exercise. One reason is that it would require massive changes to allow long-haul trucks and airplanes to operate on electricity.

Also, electricity is a high-cost energy product. Today, our economy operates on a mix of high and low cost energy products, with low cost energy products keeping the average cost down. Trying to run the economy on electricity alone is a bit like trying to run the economy using only PhDs. In theory it could be done, but it would be expensive to have PhDs waiting on tables in restaurants and delivering mail.

Too often, researchers make models without determining the details of how the system would really need to operate and what the cost would be.

Slide 28

There are many different limits for any kind of system. For example, one limit for humans is having enough oxygen. Another limit for humans is having enough water. A third limit is having enough food. Any of these things are limits. The trick is trying to figure out which one is the first limit, in a particular situation.

EROEI based on fossil fuel inputs was developed when it looked like there would be a shortfall of fossil fuels. If, in fact, our problem is not being able to get the price of fossil fuels high enough, this is a different, more complex, problem.

I think of the ratio that is popularly computed as EROEI as “Fossil Fuel EROEI.” Fossil Fuel EROEI is popularly believed to be a limit, but it is not at all clear to me that it is the first limit. It is also not clear that the limit is any particular number (such as EROEI=1, or EROEI=10).

There is a different kind of EROEI that seems to me to be at least as likely, or more likely, to be the first limit that we will reach. That is the return that workers who are selling their labor simply as labor (without advanced education or supervisory responsibility) obtain. If these workers find that their wages drop too low, this will be a limit on the operation of the economy. Low wages will prevent these workers from buying houses and cars. If the wages of the large number of non-elite workers fall too low, commodity prices will tend to fall, and the system will tend to collapse because producers cannot make a profit at such a low price.

Biologists have been studying the return on the labor of animals for many years, because their populations tend to collapse, when animals are forced to expend too much labor in finding food. EROEI based on wages of non-elite workers would seem to be a closer parallel to the animal return on labor than fossil fuel EROEI.

Slide 29

I have laid out a few of the issues I see with EROEI of intermittent renewables on Slide 29. There are other issues as well. For example, because it is a prospective calculation, it is very easy for wishful thinking to lead to optimistic estimates of future energy production and expected lifetimes of the devices.

Slide 30

Energy researchers have defined “net energy” to be any energy in excess of EROEI = 1. There is a common misbelief that if the economy can continue to produce energy products with an EROEI above 1, everything should be fine. In fact, some studies commissioned by actuaries regarding whether the economy is reaching energy limits seem to be based on an assumption that producing energy products with an EROEI > 1 is sufficient to prevent energy problems in the future. This is not a high threshold. Given such an assumption, our problems with energy seem to be far, far in the future. Pensions can continue to be paid as planned.

On Slide 30, Ugo Bardi is saying that this assumption is not correct. It is not true that the system will crash when the net energy of a particular fuel (here oil) becomes negative. We cannot understand the behavior of a complex adaptive system such as the economy in terms of mere energy return considerations. Clearly, I am not the only one looking at the economy in broader terms than an EROEI ratio.

Slide 31

Where we are now.

Slide 32

It is hard to see any good fixes. Technology reaches diminishing returns. Neither renewables nor nuclear is really working well now.

Slide 33

The standard forecasts seem to be based on the assumption that the economy can grow forever.

Slide 34

We have many problems that have been missed by recent economic modeling, including models commissioned by actuaries.

Slide 35

Actuaries are involved primarily with insurance companies and pension plans. My concern is that the financial system will be the center of the storm, as we hit limits this time. This will affect actuaries and their work.

Whether or not a new economic system can arise to take the place of our existing system remains to be seen. It certainly is a concern.

Two Observations

- My write-up is probably more complete than the actual one-hour talk was.

- I don’t think that anyone can be “blamed” for the confusion about what EROEI means. Our understanding of how the economy works is gradually evolving. Written documentation about EROEI is found in a myriad of academic papers. The name “Net Energy” seems to give energy in excess of EROEI=1 more importance than it really has.

How the Bible Belt lost God and found Trump

Flynt’s answer is that his people are changing. The words of Jesus, as recorded in the Gospels, are less central to their thinking and behaviour, he says. Church is less compelling. Marriage is less important. Reading from a severely abridged Bible, their political concerns have narrowed down to abortion and issues involving homosexuality.

Their faith, he says, has been put in a president who embodies an unholy trinity of materialism, hedonism and narcissism. Trump’s victory, in this sense, is less an expression of the old-time religion than evidence of a move away from it.

https://www.ft.com/content/b41d0ee6-1e96-11e7-b7d3-163f5a7f229c

Hedonism… narcissism… materialism…. them’s the devil’s work!

However, not everyone believes this nonsense.

There are a lot of religions, including many going by the same name. It is not fair to assume that all are bad.

War ‘Works’ – Trump Favorability Hits 50%, Highest In 2 Months

It appears that if you want to be liked by the American public, go to war. After a non-stop plunge to record low ratings for a new president, Rasmussen’s most recent data shows President Trump’s favorability surging to 2-month highs since he started rattling sabres around the world.

http://www.zerohedge.com/news/2017-04-17/war-works-trump-favorability-hits-50-highest-2-months

Christians really do love their wars….

It seems that Americans really do want America to be Great again. Trump knows this. Definition of great simply means showing who is boss. A firm hand on the tiller.

Immediately after his election the President said, ‘if we do have a war we are going to win it’. He’s conscious of the fact that Americans are also weary of war. Weary of engaging in bogged down wars.

I don’t know what the definition of winning is, but I think he’s thinking in terms of parades of returned soldiers being showered with ticker tape as they victoriously march down the main streets of New York City.

i want to ask all ofw readers that which year is collapse of civilization is gonna happened any random guess and why you think it will happened that year

as for me it will 2020 because that will be year when cheap oil producer country saudi arabia is gonna get bankrupt

http://www.mintpressnews.com/imf-says-saudi-arabia-could-be-bankrupt-by-2020/212830/

You think SA can’t adjust it’s deadline? Maybe their people won’t put up with Greek levels of austerity but they’ll probably put up with a lot more than now and the leadership aren’t going down with at least trying to right the ship, it’s why their 5 year plan is to remove subsidies (including those on oil products): https://www.bloomberg.com/news/articles/2016-12-20/saudi-arabia-said-to-consider-rise-in-retail-fuel-prices-in-2017-iwxu7w3z

If they were smart, they’d tax petroleum products instead of subsidizing them and quicken their populace’s transition.

I also feel like oil prices will go up over the next three years and help them out a bit but that depends on whether CBs can collectively keep the expansion game going (at the expense of malforming economies and increasing systemic risk).

In any case, I can’t see how SA kicks off collapse in the next 3 years (maybe in 20 if they’re the last real oil producers and we haven’t mostly transitioned off oil). You’re thinking the people revolt and SA stops producing, demand exceeds supply so prices jump and the global economy collapses? I think the world’s consumption would drop to line up with supply and oil prices would jump back above $100/bbl but life would go on.

https://twocent2c2.files.wordpress.com/2015/08/capture-delusion-blog-08-15.png

Another amazing FE prediction.

Timing is hard to guess.

By the way, I am traveling now, so I may not be able to respond to as many comment.

http://peakoil.com/publicpolicy/is-that-armageddon-over-the-horizon When the world remains in toxic denial in every other way, maybe it will be the neocons in Washington that rule the day.

I have an idea of how the pilots of Japan Air 123 must have felt during their last time on earth.

They knew for 32 minutes they were going to crash, but could not prevent it. They had a lot of technology available, but one component was missing – hydraulic pressure.

Most of the time I kind of wish I didn’t know about the end of the world as we know it. Maybe even the pilots thought they had a chance of survival right up to the end, which I really don’t. I figure ignorance really IS a bliss.

https://en.wikipedia.org/wiki/Japan_Airlines_Flight_123

I agree “knowing” is definitely not easy on the psyche. On the plus side, it has made me realize that there is no way I am reaching old age and I have come to terms with my mortality and am psychologically ready to check out when SHTF (I think, you can’t know for sure until you are actually faced with that reality). This blog is therapeutic in the sense that you can mingle with like-minded people…as you know there are not many out there that see what’s coming (even though the dashboard of Industrial Civ is flashing red across the board)..At least we have more than 32 minutes to go…I think 😉

The thought of most likely not reaching advanced old age, probably drug-ridden and fearful, in a decaying propaganda-soaked, corrupt, society is quite simply exhilarating.

I just smile at contemporaries who after a drink or two fret about pensions and old-age care homes, and ruin their – comfortable – middle-age with pointless anxiety.

One’s life’s work is, after all, mostly done by one’s 50’s (except where people have children too late as so often now).

Although the most impressive people I’ve known and whose memory I revere were still going strong in their 70’s and early 80’s, but then they were people of great character, with much to teach and good company – an artist, a craftsman, an old soldier from British special forces.

They had only reached that age, however, by virtue of modern medical science and antibiotics….

As we are clearly moving into the stage of accelerated decay and destruction which will become increasingly impossible to conceal -above all environmental destruction – a long life is not to be wished for by any sane person.

I agree with much of what you’ve said. However, I think that the impressive people that you meet who are in their 70’s, 80’s, and even 90’s who are still vital and active got to that advanced age largely by not needing and avoiding modern medicine and antibiotics.

Also, a long life may still be be worthwhile…its too soon to call.

those you describe are the lucky ones

I’m one of those….mentally and physically very fit, avoiding doctors like the plague, but many of my schoolmates are dead—

the reason I’m here??—lucky genes maybe, approach to life maybe, bloody minded blogging on here maybe?

I certainly have a very laidback approach to life and living, don’t get uptight about anything

I’m almost 70, still backpacking and surfing, and intellectually curious and a hunter gather of information and experience.

One of my comrades I backpack with is almost 80.

Good genes possibly, but if you quit moving you are dead.

Most people prefer to watch the teevee — and in more recent times place the facebook… than do any physical activity…. which turns them into sickly blobs…

Times two.

Duncan-

Good for you. I could not agree more that a person must keep moving. I was moving pretty slow by the time I got home on Saturday. I took a plunge into some mighty icy water on the snowmobile in the middle of Highlands here.

Not as bad as I thought it would be but pretty freaking cold by the time I get home.

Delegating stress is helpful….

Xabier, “The thought of most likely not reaching advanced old age, probably drug-ridden and fearful, in a decaying propaganda-soaked, corrupt, society is quite simply exhilarating.” That’s priceless.

These moronic pilots should have asked the passengers to jump from the plane and hope for the best, rather than leading them to certain deaths. They must have felt some kind of joy in their last second that at least they are not going to die alone.

One bad thing about Japan is its rigid culture, which makes them very ill prepared for emergencies. When the US bombers struck wood-based Tokyo, most people ran to the river according to instructions, and were cooked en masse in the boiling riverwater. Only a few people went against the grain, and ran to the park and they mostly lived.

https://www.bloomberg.com/news/articles/2017-04-17/china-gdp-shows-strength-as-investment-picks-up-retail-rebounds

‘China’s Economy Accelerates as Retail, Investment Picks Up!’

“China’s economy accelerated for a second-straight quarter as investment picked up, retail sales rebounded and factory output strengthened amid robust credit growth and further strength in property markets. Gross domestic product increased 6.9 percent in the first quarter from a year earlier, compared with a 6.8 percent median estimate in a Bloomberg survey. It was the first back-to-back acceleration in seven years.”

•Fixed-asset investment excluding rural areas expanded 9.2 percent for the first three months, accelerating from 8.1 percent growth last year

•Retail sales increased 10.9 percent from a year earlier in March, compared with a median estimate of 9.7 percent in a Bloomberg survey

•Industrial output rose 7.6 percent last month from a year earlier, compared with an estimated 6.3 percent rise

“For the first time in the recent years, China starts a year with a strong headline GDP,” said Raymond Yeung, chief greater China economist at Australia & New Zealand Banking Group Ltd. in Hong Kong, who correctly forecast the growth pace. “Thanks to strong investment and property, the economy is performing well.”

See what happened here? Some posters look at graphs and think once they’ve started down they will continue to go down until collapse hits, but the reality is it can go back up just as easily as it can go down as we can see from this recent development in China.

I look at graphs with declining trend lines…. and I expect (and hope – I’d even pray if I thought that would help) the trends to turn based on more stimulus…

So far I have not been disappointed.

However I am not yet to the point in believing in perpetual economic motion machines….

Oh ….and with respect to China – and all other economies…. remember this:

Jean-Claude Juncker: ‘When it becomes serious, you have to lie’

http://www.telegraph.co.uk/news/worldnews/europe/eu/10874230/Jean-Claude-Juncker-profile-When-it-becomes-serious-you-have-to-lie.html

The closer we get to the precipice… the bigger the lies will be…. so take no comfort in govt issued statistics.

After all — were we not recently told that consumer confidence is soaring in America?

Yet we are seeing spending at restaurants and shopping collapse.

And please don’t tell me this is Amazon … I believe Amazon was around last year … and we did not see the retail apocalypse then.

also if this was truth that china economy is recovered than china biggest Aluminum Producer would not in danger of bankrupt

http://www.zerohedge.com/news/2017-04-16/worlds-biggest-aluminum-producer-faces-default-warns-dramatic-social-unrest-without-

At the end of the day, there is absolutely no solution to get us out of this predicament (which is why it’s a predicament!)..my home province loves to tout how we run on clean energy (hydro-electric power)…well that satisfies the masses, however turns out, it’s not green at all..

From Andrew Nikiforuk’s article “Debunking Dams:New research shows how hydro-electric energy can turn carbon sinks into methane bombs.”:

“But the science shows that damming water and flooding forest soils does not deserve the adjective clean. In fact, hydroelectric dams serve as a powerful reminder that every form of human-mined energy comes with significant ecological cost.”

http://www.alternativesjournal.ca/science-and-solutions/debunking-dams

So even if the Financial System was to hold for years to come (which it won’t of course), there is not one solution out there that does not involve wrecking the ecosystems…to create energy we must extract resources which in turn destroy the planet…

And why it is that no one can grasp the impossibility of supplying any sort of centralized energy in any sort of centralized global system, I can’t understand.

https://thewest.com.au/news/world/donald-trumps-plans-to-destroy-kim-jong-uns-nuke-sites-ng-b88447572z

Trump plans to Destroy Kim Jong Uns Nuke sites. Is it just me or does Trump make anyone else nervous and ordering freeze dried food? I hear sales are up.

https://www.bloomberg.com/news/articles/2017-04-16/faithful-flock-to-vatican-as-pope-celebrates-easter-sunday

And then the pope went off for a wonderful lunch prepared by the Vatican kitchen’s outstanding chefs……. followed by a round of golf… then like a good CEO he had a look at the business papers… the church’s stock portfolio…. and the market pre-Easter closing numbers….

Listen to the pope speak:

‘Would you like to see the Pope on the end of a rope – do you think he’s a fool?’

Very much so. I would enjoy that immensely.

And here is what I refer to as good news.

Electric Grid Study Ordered by U.S. Energy Chief to Boost Coal

In an April 14 memo obtained by Bloomberg News, Perry highlights concerns about the “erosion” of resources providing “baseload power” — consistent, reliable electricity generated even when the sun isn’t shining and the winds aren’t blowing.

President Donald Trump has already moved to dismantle Obama-era policies that discouraged coal-fired power plants.

https://www.bloomberg.com/politics/articles/2017-04-15/electric-grid-study-ordered-by-u-s-energy-chief-to-boost-coal

Burn Baby Burn!

Every tried to explain to someone that solar panels are made using huge amounts of coal – that the amount of energy you get out of a solar panel over its life time is about the same amount of energy that you used to make it.

That if you decide you want to store the energy and use batteries — the amount of energy that went into making the batteries and panels and other gear… is substantially more than the energy that what the system will generate over its life span.

I suggest you do not.

I tried to explain this to an engineer recently… he did not dispute it — he just ignored it and continued to tell me how the future was all about renewable energy.

Another instance of where smart people can be very stupid.

Has something to do with repressing thoughts of grand kids being hunted and roasted….

Yes kids this is the last of the Fast Eddy tomorrow its weekenders from Manhattan.

Growth is futile.

Norman, your article An Infinity of Futility, is (as always) excellent. I am posting it here because I’m sure others her on OFW will be interested to read it:

https://extranewsfeed.com/an-infinity-of-futility-819630ea935f

Just noticed DJ posted it a few days ago…kind of get lost in the sea of comments on what has been posted lol…anyway for those who had not seen it, its well worth the read!

thank you

Thanks Norman—

Very good analysis.

Yes, that hit the nail on the head. Good work Norman, and very well written.

I find it quite interesting how tunnel-visioned is the author of this blog and most of commentators. It seems like every group is so preoccupied with their own stuff: here we have peak oilers, than we have people at ZeroHedge into economy, Zionists are completely consumed with multiculturalism, anti-semitism and holocaust, white nationalists with white genocide, libertarians with constitution, environmentalists with ecosystem, then we have global warming sect, Bannon&co with four turnings theory and plenty other groups. Some groups overlap less or more, some people are members of more than one group.

But very few people really try to analyze several off these things and how they interact with each other. For one multiculturalism is barely tolerable in times of prosperity. I don’t wanna know what will happen to diverse places once the music stops. It will be bloody.

Current system needs to be reformed into zero growth model and huge culling of the [human] herd is needed. This cant be done before current system starts collapsing, but everyone can see there are strong forces rushing it towards collapse. Georgia Guidestones suggest there are already plans for post collapse.

I cannot see any zero growth system as working. Diminishing returns are a problem in a finite world. Thus, any economy cannot use any resources, except a tiny amount of renewable resources. No metals. Maybe not even stones, because they don’t renew either. Population cannot rise at all either, so humans probably cannot cook their food. The system cannot really work.

You are pushing your vision of sustainability to extreme. Why is it not OK to use stones, but OK to use tiny bit of trees and fish? In strictest physical terms no resource is truly renewable. E.G. forests and fish are being renewed by using Sun’s energy which itself is not renewable.

Excellent comment. Please go in to details on how to get it done. Please be specific and make sure it is logical and doable. Also put on the thinking cap so that the solutions that you provide consist of common sense and that it can be executed (not pie in the sky type of solution). I am all ears.

As Zerohedge moto goes: on long enough term the survival rate for anything drops to zero. But we could greatly extend our civilization by properly reforming it.

The biggest obstacle to that is our own human nature. Evolution has always punished sustainable groups and rewarded those that go into overshot, grow quickly and take from their competitors. This survival strategy is deeply ingrained into our DNA. Another thing I know about human nature is that once you internalize something, there is almost nothing that will change your mind, so I have no intention trying to prove anything or to make some airtight model that will work.

There are doomsayers on this site who predict end of world when it all collapses. Even Gail is saying that once BAU ends that all remaining resources will never be utilized. Her ideology and many of followers on this site believe that in order to make system infinitely sustainable, we need to completely stop using non renewable resources. This is ridiculous. If we operate in such strict terms than we need also to understand that no resource is truly renewable. So when im talking about making system sustainable I understand this hard reality.

There is no doubt that if we dont reform current system that we will trigger massive dieoff within this century. But if we succeed then our civilization can continue for foreseeable future and with future innovations this will be further extended.

How would you reform the current system.

Specifics please.

In the meantime …. I will get ready

http://www.kitchenknifeking.com/wp-content/uploads/2015/12/What-is-a-Whetstone.gif

I am looking at this for little over a year and it is extremely complex issue. I dont have any specifics worked out. Most importantly we need to create a system where sustainability is rewarded and overshot is punished (no idea how). Capitalism wont work, you depicted the reason in post below, multiculturalism cant work either because in zero growth environment minority right become zero sum game. We need upper limit on population (a lot less than current number), on resource extraction. We need balance between individual freedom and social duties. I am almost certain that plan to create a zero growth system is already in the works.

You mentioned max 500M people, how does that rhyme with we and reform?

‘I am almost certain that plan to create a zero growth system is already in the works’

Oh yes — the CBs definitely have a plan … not to create a zero growth system because that would be suicidal — rather the plan is for what to do when the stimulus no longer has any effect …

Here’s the plan: https://www.forbes.com/sites/ralphbenko/2013/03/11/1-6-billion-rounds-of-ammo-for-homeland-security-its-time-for-a-national-conversation/#65768957624b

I am almost certain that plan to create a zero growth system is already in the works.

Yes, it’s called die-off…

http://www.countercurrents.org/pc15.jpg

Psile said: “Yes, it’s called die-off…”

Hahahahahahaha it’s funny coz it’s true!!!

Miha, please be specific how you want to achieve it. We have way too many people coming in to this blog with lots of talk but nothing on details. Be specific on how you want to achieve it.

Yes.. I want to be a billionaire and I want to have all trappings of the rich and famous. How to get there? I can talk and I don’t have the details on how to do it.

Now is your chance to say it out. Otherwise, I think this blog may not be suitable for you.

The current system is globally interconnected. If it remains a globally interconnected–one size fits all–system, I don’t know how you would propose to reform it. I appreciate how you began your post, just the same.

What does your zero growth model look like?

This is mine:

http://2.bp.blogspot.com/-gJiwxsIcjeg/VLi6ZO0-2kI/AAAAAAAALD0/LIZf7xugC4w/s1600/Deflation%2Bcycle.gif

Which would result in this:

http://www.didier-bertin.org/medias/images/p1050196.jpg

Flooding cuts off aid supplies, escape route from west Mosul

(the smoke is starting to clear)

http://www.reuters.com/article/us-mideast-crisis-iraq-mosul-river-idUSKBN17I0GC?feedType=RSS&feedName=worldNews&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+Reuters%2FworldNews+%28Reuters+World+News%29

http://s3.reutersmedia.net/resources/r/?m=02&d=20170416&t=2&i=1180811901&w=&fh=&fw=&ll=780&pl=468&sq=&r=LYNXMPED3F0JK

On the question of loneliness, discussing with others: don’t waste your time. Discussing collapse is like telling people how to raise their kids, or what to eat, or that their political and religious views are wrong. They don’t want to hear it, they will shun you more than they would a serial killer.

But why? Because humans are optimistic, it’s wired in. It sort of has to be that way.

On the question of bubbles: the difference this time is that everything, everywhere is a bubble. We are at peak everything. This is as good as it gets, this is the farthest humanity can advance. We are moving into a millenial dark age, there is nothing you can do.

It’s like trying to explain to dolph that BAU Lite is impossible.

It’s like trying to explain to Fast Eddy that we wil be eating turkey for Xmas this year.

And roasted children soon enough….

When there are only two things on the menu:

– broiled sewer rats

– broiled succulent child

What would you order?

Ah, you may be partly jesting there Eddy, but that comment comes back to my original comment on the theme of parental fear. If you put very graphic material in front of individual parents that shows that their dear little Amy, or Christen, or Billy or Helen…. is likely to live through (or not live through) a horribly painful future this does have an immediate, and sometimes, lasting impact on them. It’s important to bring it to the personal.

A few posters disapproved of that original comment in that it sounded too hopeful en masse, as if this exercise was some sort of panacea. I’m sure others would disapprove of focussing on negative fears and I accept that it’s just one interesting strategy and not necessarily the best. (At times I also wonder: if the dice is now irrevocably cast what purpose there is at all in stressing people pointlessly with our collective fate.)

No … not jesting at all.

I am quite certain that we will be eating each other in due course.

It’s what was done during past famines….

But this famine will be different – it will be total – it will be global — it will not be an isolated event — this time there will be no authorities to stop us from eating each other.

The formula looks like this:

– first we loot the grocery stores

– then we kill the domesticated animals – dogs cats etc… as well as all farm animals

– then we start killing the wild animals — that won’t last long as there are not many and they will flee

– we will of course have a go at the neighbours veg garden

– then we will resort to eating grass and bark

– it will be around this time that we start looking for easy prey – much as a lion looks to take down a young antelope…. children come onto the menu — along with the weak and dying who cannot fight back

No parent wants to think about this. No parent will accept this is what will happen. I suspect my posting this on FW along with graphic images — has shocked a few people.

But make no mistake — this is what the future holds. This – and slavery and torture and rape and suffering.

You cannot feed a population of any type of animal unlimited amounts of food — allow the population to expand to 7.5 billion — then take the food away…

And expect anything but a truly horrific outcome.

I don’t mind reading that at all, Eddy. It’s a great antidote to all those posts on other venues that are salivating about autonomous cars and 3D printers as if these are heralding in a new golden age of prosperity.

I wonder what those who believe in the AI BAU Lite future think … when they read that.

Ah 3D printers reduce the scale required to keep the goodies flowing for the owners. AI, 0.1% paradise looking better and better. 0.9% to shuck and jive.

I’ll have a roasted gold buffalo please.

Sewer Rat. Definitely the Sewer Rat. 🙂

It we don’t get nuked!

Getting nuked seems greatly preferable to FE’s scenario. But his scenario is probably the default one for where we’re headed now. Yes, A brilliant flash of light is best. This could explain why I’m a warmonger.

On this Easter Sunday, let us all pause and remember when Sean Spicer was the White House Easter Bunny in 2008.

https://pbs.twimg.com/media/C9hrUaXXcAAv04z.jpg

Only a small drop in percentage of vaccinated persons can cause that the epidemics like measles are back:

http://praguemonitor.com/2017/04/12/northern-moravia-has-unprecedented-38-cases-measles

“Daily Lidove noviny (LN) writes today that epidemiologists say if 95 percent of the population is vaccinated, the spread of the virus stops.”

Now, the vaccination dropped to 93 % towards the end of 2015, and the measles are back…

https://spravy.pravda.sk/domace/clanok/426405-epidemiu-osypok-mame-za-dverami-na-morave/

http://www.thenews.pl/1/9/Artykul/198983,Measles-virus-spreading-in-Poland

Poland of all places, then it should not be an imported problem.

Actually, the world meliorismnow described, in which the 1% had everything and the rest living like animals, did exist back in 1913, when the number of cars and airplanes (called ‘aeroplanes’ back then) could be counted individually. A lot of advanced occurred that people called it the “Belle Epoque”.

BAU did not exist – instead an elaborate system of trade existed, and only 8 nations mattered – USA, Britain, France, Germany, Russia, Austria-Hungary, and Italy & Japan as ‘lesser’ great powers. Much less complexity.

http://siteresources.worldbank.org/INTPGI/Resources/13243_The_size_distribution_of_income.pdf

Page 27 shows that on 1910, the top 10% of Europe and its offshoot (USA and what is now Canada, and excluding Russia and poorer Balkan countries) had 64% of total income. At that time the rest of the world could be safely ignored. (The figure for 1950 is misleading since on 1950 only USA had some kind of prosperous economy)

The pop of Western Europe + USA on 1910 is about 300m. 10% of them is 30m, or less than 2% of the world pop (about 1.6 – 1.7bil). They had 64% of the world’s industrial income, but things worked quite well.

We can thank Gavrilo Princip, a name the Serbs still remember to honor him with a statue in the Serbian capital, Brigadier Chuck Fitzclarence, a name the Brits dumped into the memory hole, and a few ‘heroes’ breaking such safe arrangement and arming the masses, who had to be shmoozed by the elites after 1918.

Such arrangements are sustainable, and was done before without BAU. The Great War was fought with coal, petroleum playing just a tiny role. We are simply going back to 1913; that’s all.

We are not and cannot go back 100 years due to the gathering environmental catastrophe -very different circumstances, and so much remained still untapped then in terms of resources.

Environmental degradation and poisoning will overwhelm nearly everything this century. One only has to watch nature closely to understand this, it is in the air.

Perhaps there will be some pockets in which basic non-industrial lives can be lived, but it is doubtful and almost impossible to hazard a guess at.

Although I agree, a 1910 model of society is something which the rich are rather hoping to recreate, as public references to ‘reducing entitlements’ show, and the obvious scaling-back of pensions and social security in nearly every advanced economy demonstrate.

Alas for them, even in the era 1830 to 1914 the threat of revolution was ever-present, and they knew it – read what educated and wealthy people wrote at the time and it is very clear, they didn’t expect anything of their social and economic structure to last very much longer.

‘If it lasts my time I’ll be happy’ was a common saying in the early 1900’s.

We hear a similar saying by many, wishing the environmental collapse does not hit them in their lifetimes. Every age has people worrying about things.

The fear of revolution was exaggerated; the rev of 1905 was financed by the Japanese,

http://eprints.lib.hokudai.ac.jp/dspace/bitstream/2115/8055/1/KJ00000034012.pdf

I stand by the fact that the stupid order by Brigadier Chuck , the most stupid act of the 20th century if not the entire world history, has created about 99% of the problem the world is facing now.

Reducing the number of consumers will solve a lot of the shortage and other issues we have now,, although we can’t do anything to the stuff already depleted or destroyed.

After Seven Years of Austerities 40% of Greeks Cannot Afford to Pay Their Utility Bills

http://greece.greekreporter.com/2017/04/07/after-seven-years-of-austerities-40-of-greeks-cannot-afford-to-pay-their-utility-bills/

Can’t they detroit it? Yes I read in the link it is what they do.

For all the noise they seem to be doing fine

https://surplusenergyeconomics.wordpress.com/2017/04/14/93-the-prosperity-equation/

Only -3.9%, I suppose stop paying for electricity offsets that.

Have any those who say that we will have robots and AI did any work on AI or robots? Engineers? software and hardware anyone?

A simple robot is so complex that it is usually filled with bugs.

Do the AI/Robots proponents know that how many electronic parts in the robot? How many mechanical actuators, solenoids,

How difficult it is to program a robot? AI is even worse. You really need the full complement of BAU to do that. Who is going to service the robots?

I really get pissed off by people who just blabbered about how technology can save us when they themselves don’t know what technology is. These are the guys will say “Call IT support” when their computer cannot boot up. I have seen and personally experience working with these people….. and people trust their future on this “visionary”…

Want to bet that Elon Musk will do that ? Call IT support? Maybe he does not even use a computer.

http://static3.businessinsider.com/image/5711368252bcd05b008bd03b-1653-2339/elon%20musk%27s%20re%CC%81sume%CC%81.png

He has a degree in Physics. Unless he did very badly in his physics, he should know the limits of physics. However, with easy money flowing in from all sides for all his grandiose projects, it is intoxicating to dwell in the best of BAU (and in the process of prolonging it).

This is probably partly directed to me, for having mentioned AI bjobots twice yesterday.

No, I’m not a believer in AI. Programming a computer for a specific task is one thing, for a complex problem not known in advance … nope.

Wake me up when you have a spell checker that works (yes I know …)

I don’t pinpoint at people. I just say it out loud because there will be people coming with self-driving cars, robotic waiter, chef, etc. This is the type of Elon Musk will be happy to promote.

The trouble with good programs are you have to write them yourself.

I am nowhere near writing an AI.

I am a programmer and an engineer…. I understand what you mean and I understand all the crap on self-driving car and AI.

What is the self driving car all about? I can imagine self driving Bradleys and MRAPs that could patrol and do mop up after the zombieapocalype. They could be programmed to fire on anything that moves. But how do self driving cars fit into today’s world? I’d be glad if they made cars that took off automatically when the light turns green. It’s hard to be patient setting at a green light behind some screenzombie that texting instead of driving.

First world problems.

Aubrey,

Desperation?

EVs are expensive but that doesn’t matter because they will be self-driving so they don’t need a parking spot, they will drive around making errands for you and cabbing other people and they will function as a battery for your solar panels and balancing the grid with smart loading tech.

None of that matters because the range is barely enough to get you to work where it will need to load for a few hours.

DJ, shirley you can’t be serious?

Holy Elon, the Great Visionary, will look down on us smiling wherever we are, he will solve all problems, there is no need to worry at all…..

Elon Musk is an actor. That is all he is – an actor!

+++++

He was given a tap on the shoulder some years ago and told – here is the situation — we need you to play this role because it will help keep BAU alive a little longer — you will get everything you want — unlimited funding — the MSM will support you with unlimited positive spin.

There is no downside — and the upside is you get to be a hero in the eyes of the people — you represent hope.

Your character and code name will be Solar Jesus.

He is able to apply liberal amounts of lipstick to lots of piggys.

“That one sentence,

Every American will be forced to register or suffer not being able to work and earn a living.”

I’m sorry to be the one to inform you Jerry that most Americans already suffer not being able to work and earn a living…so maybe they won’t register.

If only you knew how many homeless are in my city and like myself we all have a social insurance number! Registered!

Beyond that I’m reminded so well of that banker Warburg who said way back in the 1920’s or 30’s

“The world lives in a fools paradise based upon fictious wealth, rash promises and mad illusions. We must beware of booms based upon false prosperity which has its roots in inflated credits and prices.”

Wow here we go again I guess having learned nothing?

Yesterday I visited a friend and we went for a walk and talked life and real estate came up and to my utter disbelief he showed me a piece of land which had a house torn down and gone just bare land and to hear that it was for sale for 420,000 left me aghast. We are not talking a great location. I looked at him and said that was unbelievable bullshit actually. What when they build a house on it that little corner lot will be over a million? Well yeah he said my own house which is quite new and modern I could sell for 1.2 million. What I screamed at him are you kidding me? Who can actually afford this? Who makes or has a career that can support such a thing? There aren’t enough jobs even for elite workers who can handle that. Yeah he replied that why I have three immediate families under my roof and when I do sell I will have to share the proceeds with everyone.

The 1920’s crashed as a result of these ‘booms based upon inflated credits and prices’ and wow are we in for a correction. Since when does a house cost millions when there are no jobs that can even support half that price?

Here is a great article about this very thing https://asm-air.com/uncategorized/los-angeles-housing-bubble/

Everything is just so absurd today and why is it than in America anyone who try’s to do the right thing politically winds up dead and this under very strange and unusual circumstances? They even tried to take out Catherine Austin Fitts who was doing or trying to do something great for her people. You should read her story wow.

God I know there are those who wish the Church to be a solution and it should be but the enemies we are faced with today well it leaves me with a heavy heart. St. Paul summed it up best I think::

29 I know that after I leave, savage wolves will come in among you and will not spare the flock. 30 Even from your own number men will arise and distort the truth in order to draw away disciples after them. 31 So be on your guard! Remember that for three years I never stopped warning each of you night and day with tears. Acts 20:29-35

Perhaps it is Daniel who says it best rather:

When the power of the holy people has been finally broken, all these things will be completed.” Daniel 12

Hard work it is to stay righteous and imagine how wicked a people and planet must become to break the strength of someone like a Peter or Paul or even Noah for that matter. This world is a terribly evil place.

Anyway Grayfox we are all registered its called ‘SIN’ Social Insurance System. A proverbial crock of government imposed control or soon will be. The good news we are warned before hand.

Enough of the Bronze and Iron Age Fiction.

Childish creation myths from ignorant goat herders 3000 years ago is not the best reference point for basing reality.

FE the Aldrich Plan Jekyll and Hyde was instituted when over Christmas break. Sneaky evil dogs. In their apparent hatred for everything Christ they pushed through this bill under the cover of darkness. Betrayed we all were but mark my words God will have the last laugh..

So god also has a sense of humour?

Does he make witty comments when he’s not urging his followers to commit genocide?

A psychopath with a sense of humour — how fabulous!

its just a figure of speech,

The Psychopathic Sky Daddy has always had a sick sense of humor.

His sense of humour is often dark…. for instance… when during the famine in Ukraine he laughed deeply as he watched his starving creations chase after young children killing them and roasting them then eating them…. very very amusing – in a dark sort of way.

While on the topic of god — does the bible explain why an entity that is all powerful — who could have anything he wanted… would bother to create Earth — and humans… and animals… and all the rest…

What is the purpose?

Was he bored so he decided – I’ll have one of these…. is the Earth and all on it like a toy to amuse him?

I guess it gets boring knowing the fate and destiny of everyone. It has to be really boring to be God – it would be like watching endless re-runs. He turns up the wick every now and then and creates really outlandish scenarios to play out in his mind. It is all so futile to be human.

I’ll tell you what blows my mind though is this quote by a Colonel Edward House. In his novel called PHILIP DRU: ADMINISTRATOR: A STORY OF TOMORROW 1920-1935 {how prophetic a title} this is what the author fully says:

“[Very] soon, every American will be required to register their biological property in a National system designed to keep track of the people and that will operate under the ancient system of pledging.

By such methodology, we can compel people to submit to our agenda, which will affect our security as a chargeback for our fiat paper currency. Every American will be forced to register or suffer not being able to work and earn a living.

They will be our chattel, and we will hold the security interest over them forever, by operation of the law merchant under the scheme of secured transactions. Americans, by unknowingly or unwittingly delivering the bills of lading to us will be rendered bankrupt and insolvent, forever to remain economic slaves through taxation, secured by their pledges.

They will be stripped of their rights and given a commercial value designed to make us a profit and they will be none the wiser, for not one man in a million could ever figure our plans and, if by accident one or two would figure it out, we have in our arsenal plausible deniability.

After all, this is the only logical way to fund government, by floating liens and debt to the registrants in the form of benefits and privileges. This will inevitably reap to us huge profits beyond our wildest expectations and leave every American a contributor to this fraud which we will call “Social Insurance.”

Without realizing it, every American will insure us for any loss we may incur and in this manner; every American will unknowingly be our servant, however begrudgingly. The people will become helpless and without any hope for their redemption and, we will employ the high office of the President of our dummy corporation to foment this plot against America.” http://www.gutenberg.org/ebooks/6711

That one sentence,

Every American will be forced to register or suffer not being able to work and earn a living.

sounds earliy familiar to this

“He also forced everyone, small and great, rich and poor, free and slave, to receive a mark on his right hand or on his forehead, so that no one could buy or sell…

This is just too much of a coincidence to be a coincidence and America was the one to send us down that road back in the 1930’s? and now the push for a cashless society so again

{‘FORCED TO REGISTER OR SUFFER NOT BEING ABLE TO WORK AND EARN A LIVING.’ Col. House}

and I guess I don’t have to mention quotes that we are all familiar with but here goes:

“I am a most unhappy man. I have unwittingly ruined my country. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated governments in the civilized world. No longer a government by free opinion, no longer a government by conviction and the vote of the majority, but a government by the opinion and duress of a small group of dominant men.” Woodrow Wilson

“This act establishes the most gigantic trust of Earth…When the President signs this Act, the invisible government by the Money Power, proven to exist by the Money Trust investigation, will be legalized…This is the Aldrich Bill in disguise…The new law will create inflation whenever the Trusts want inflation…From now on, depressions will be scientifically created…The worst legislative crime of the ages is perpetrated by this banking and currency bill.” Congressman Charles August Lindbergh, Sr.

“We have in this country one of the most corrupt institutions the world has ever known. I refer to the Federal Reserve Board and the Federal Reserve Banks…Some people think the Federal Reserve Banks are United States Government institutions. They are not Government institutions. They are private credit monopolies which prey upon the people of the United States for the benefit of themselves and their foreign customers… The Federal Reserve Banks are the agents of the foreign central banks…In that dark crew of financial pirates, there are those who would cut a man’s throat to get a dollar out of his pocket.” Every effort has been made by the Federal Reserve Board to conceal its power, but the truth is the Fed has usurped the government. It controls everything here {in Congress} and controls all our foreign relations. It makes and breaks governments at will…When the Fed was passed, the people of the United States did not perceive that a world system was being set up here. A super-state controlled by international bankers, and international industrialists acting together to enslave the world for their own pleasure.” Louis T. McFadden June 10, 1932

Still behind to Yevgeny Zyamatin’s “We” (1921), the father of Aldous Huxley’s “Brave New World”, George Orwell’s “1984” and Kurt Vonnegut’s “Player Piano”.

Zyamatin helped to build the USSR, but didn’t like how things were going and he was powerful enough to petition Stalin to kick him out from there. His “We” is now in public domain (he died just before Hitler invaded France so his copyright ran out).

https://mises.org/library/we

The Last Country America “Liberated” From An “Evil” Dictator Is Now Openly Trading Slaves

It is widely known that the U.S.-led NATO intervention to topple Libya’s Muammar Gaddafi in 2011 resulted in a power vacuum that has allowed terror groups like ISIS to gain a foothold in the country.

Despite the destructive consequences of the 2011 invasion, the West is currently taking a similar trajectory with regard to Syria. Just as the Obama administration excoriated Gaddafi in 2011, highlighting his human rights abuses and insisting he must be removed from power to protect the Libyan people, the Trump administration is now pointing to the repressive policies of Bashar al-Assad in Syria and warning his regime will soon come to an end — all in the name of protecting Syrian civilians.

But as the U.S. and its allies fail to produce legal grounds for their recent air strike – let alone provide concrete evidence to back up their claims Assad was responsible for a deadly chemical attack last week – more hazards of invading foreign countries and removing their heads of state are emerging.

This week, new findings revealed another unintended consequence of “humanitarian intervention”: the growth of the human slave trade.

The Guardian reports that while “violence, extortion and slave labor” have been a reality for people trafficked through Libya in the past, the slave trade has recently expanded. Today, people are selling other human beings out in the open.

“The latest reports of ‘slave markets’ for migrants can be added to a long list of outrages [in Libya],” said Mohammed Abdiker, head of operation and emergencies for the International Office of Migration, an intergovernmental organization that promotes “humane and orderly migration for the benefit of all,” according to its website. “The situation is dire. The more IOM engages inside Libya, the more we learn that it is a vale of tears for all too many migrants.”

More more more … how do you like it how do you like it… more more more

http://www.zerohedge.com/news/2017-04-15/last-country-we-liberated-evil-dictator-now-openly-trading-slaves

Shall we sing along?

https://www.youtube.com/watch?v=IsbEkQBYZPQ

And meanwhile enjoy the Easter weekend …. hope everyone has a very nice Sunday meal — don’t let this Libya fiasco trouble you .. don’t give it a second thought…

And I don’t imagine anyone will need to worry about any of the preachers at the various churches mentioning this war crime committed on behalf of all Americans…. after all – you did elect Obama … and you do believe that he is the most powerful man on earth …. so you would be complicit in the nightmare that is Libya (and Iraq… and Syria)…

For those who believe in good and evil …. America would have to be defined as pure evil … no?

Yes Eddy of course that is why I am often left wondering about a certain biblical chapter Rev.16 and a city referred to as Babylon that will experience something similar to Sodom and Gomorrah. Babylon apparently is a city which rules over the affairs of mankind and commits a huge share of the evil upon the world and because of it is destroyed by God Himself. We are given to know that she sits on 7 hills {Rev. 17:9} and you would think that it would have to be the city of Rome and her famous seven hills. The Quirinal Hill, Aventine Hill, Caelian Hill, Viminal Hill, Capitoline Hill, Esquiline Hill, and Palatine Hill. At least that is the historical/geographical perspective. http://www.vatican.com/articles/rome/the_seven_hills_of_rome-a4131 Some believe and interpret it as Jerusalem but how can that be given that Jerusalem has a future {Zech. 14 & Rev. 20:6} whereas Babylon once she is destroyed she is destroyed forever never to be inhabited or rebuilt ever again. {Rev. 18:21-23} Babylon is going the way of Sodom and Gomorrah!

‘Then a mighty angel picked up a boulder the size of a large millstone and threw it into the sea, and said:

“With such violence

the great city of Babylon will be thrown down,

never to be found again.

The music of harpists and musicians, pipers and trumpeters,

will never be heard in you again.

No worker of any trade

will ever be found in you again.

The sound of a millstone

will never be heard in you again.

The light of a lamp

will never shine in you again.

The voice of bridegroom and bride

will never be heard in you again.

Your merchants were the world’s important people.

By your magic spell all the nations were led astray.

In her was found the blood of prophets and of God’s holy people,

of all who have been slaughtered on the earth.”

The Rome of today though is a far, far cry from the Rome of yesterday. Roads no longer lead to her doorsteps, her military is practically non-existent, economically there is no Wall Street, no Federal Reserve, no reserve currency, and she is certainly no port city as exemplified in Rev. 18. To find a city of comparable description and one need only look across the Atlantic Ocean to a city like New York or Washington for that matter. Note Washington has its own seven hills the names of which are Capitol Hill, Meridian Hill, Floral Hills, Forest Hills, Hillbrook, Hillcrest, and Knox Hill.

New York/Washington – Babylon? Well, don’t throw out the possibility just yet for as it is often said truth is stranger than fiction. Actually, given America’s power and influence over practically the entire world and if she doesn’t sit as a king or queen over it all? Especially pertinent are these words however:

“In her heart she boasts, I sit as queen; I am not a widow and I will never mourn.” {Rev. 18:7}

Doesn’t this sound remarkably similar to New York with her Statue of Liberty and her political philosophy of Manifest Destiny which is a uniquely Masonic ideal? It is certainly strange how this city along with Washington and London, England are inextricably intertwined with Freemasonry, in fact apparently every capital of the world next to even the most obscure of towns has some measure of this secret society working within their midst? http://vigilantcitizen.com/category/sinistersites/

Idolatry pure and simple but why!? Furthermore, just do a google search of obelisks and pyramids and ask yourselves why and what fore these things? http://www.themoderngnostic.com/?p=73510

Even the American dollar bills boast of this, a pyramid with the all-seeing eye? This is their symbol! Who are they honoring and worshipping? I believe the name JAHBULON comes to mind? She has always portrayed herself as a city of wealth, power and prestige truly a city that never sleeps. If she isn’t the modern day Rome of old!? Something just doesn’t seem right, so unless some kind of a miraculous/demonic event occurs that returns Rome to its former glory under another Caesar we are left with a ‘mystery.’ Note though how most if not all nations capitals are very well interconnected with one another {obelisks}particularly Europe with her monarchies and given how money and banking {Federal Reserve etc.}is the center around which all power rules next to these huge multi-national corporations of today and one need only look there for the key to Babylon’s existence. For as law enforcement so often says if one wishes to find the thieves and murderers just follow the money an interesting example of which can be found in the words of one Marine General Smedley Butler {1881-1940} who referred to himself as little more than “a high class muscle man for Big Business, Wall Street and the bankers.”

“I helped make Mexico, especially Tampico, safe for American oil interests in 1914. I helped make Haiti and Cuba a decent place for the National City Bank boys to collect revenues in. I helped in the raping of half a dozen Central American republics for the benefits of Wall Street. The record of racketeering is long. I helped purify Nicaragua for the international banking house of Brown Brothers in 1909-1912. I brought light to the Dominican Republic for American sugar interests in 1916. In China I helped to see to it that Standard Oil went its way unmolested.” {War is a Racket 1935} http://www.warisaracket.com/

So whatever the case may be ‘New York/Washington or Rome’ ultimately her identity will be identified for look who exactly is God referring to when He says in Chap. 18:4:

“To come out of her my people, so that you will not share in her sins, so that you will not receive any of her plagues.”

FE America is not a Christian Nation though for a very short period of time it actually was. Our enemies though have been hard at work putting an end to that and I for one can’t for the life of me understand how so many preachers in pulpits are actually practicing freemasons? Since when does idolatry and Christianity go hand in hand with one another?

So when did America stop being a Christian nation — would it have been when they genocided the native people or afterwards?

Keeping in mind your trusty bible recommends genocide…. over and over….

So you best be careful you don’t contradict yourself.

Was it Christian when enslaving millions of africans…

Pseudo Christian would be a better expression. When did it stop being a Pseudo Christian nation. The most cherished practices have nothing to do with Christianity. Take Easter the name comes fro Estarte the fertility goddess of the Greeks. It’s symbols include the egg used in Victorian molding copied from her temple in Greece. But the origin of that comes from the image of her in the temple and they’re not eggs or breasts lacing her front. Dec 25 is another good one likely the birth of Nimrod according to Babylon records. Or Santa Clause most likely the Roman god Saturn same as Greek god Cronos. A cannibal who eats his children. The Christmas tree? A hold over from Canaanite Baal worship which was practiced in the forests. The decorations represented sacrificed children’s heads. The priests of Baal were named Cana – Preist Bel – Baal. They would eat part of the sacrifice. The Yule log was from the belief in the rebirth of Nimrod as Tammuz. It’s found on Babylonian coins. Worship of a Mother Goddess originated in Babylon with Semiramis the Mother of Tammuz.

Not seeing much Christianity in “Christianity” other than the use of the word.

This is what really bothers me about the God in the Bible:

God is all powerful and all knowing so he must know your desinty

God created everything so he must have created hell and satan too.

Hell is more torturous than anything you can imagine.

A sentence to hell is eternal torture.

So,the Bible makes me ask myself: Do I want to spend eternity with a being who create hell? That would be worse than worshiping Wayne Gacie or Jeffery Dahmer. Would you want to be sleeping in the same house with one of those two?