Economists, including Ben Bernanke, give all kinds of reasons for the Great Depression of the 1930s. But what if the real reason for the Great Depression was an energy crisis?

When I put together a chart of per capita energy consumption since 1820 for a post back in 2012, there was a strange “flat spot” in the period between 1920 and 1940. When we look at the underlying data, we see that coal production was starting to decline in some of the major coal producing parts of the world at that time. From the point of view of people living at the time, the situation might have looked very much like peak energy consumption, at least on a per capita basis.

Figure 1. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects (Appendix) together with BP Statistical Data for 1965 and subsequent, divided by population estimates by Angus Maddison.

Even back in the 1820 to 1900 period, world per capita energy had gradually risen as an increasing amount of coal was used. We know that going back a very long time, the use of water and wind had never amounted to very much (Figure 2) compared to burned biomass and coal, in terms of energy produced. Humans and draft animals were also relatively low in energy production. Because of its great heat-producing ability, coal quickly became the dominant fuel.

Figure 2. Annual energy consumption per head (megajoules) in England and Wales during the period 1561-70 to 1850-9 and in Italy from 1861-70. Figure by Wrigley

In general, we know that energy products, including coal, are necessary to enable processes that contribute to economic growth. Heat is needed for almost all industrial processes. Transportation needs energy products of one kind or another. Building roads and homes requires energy products. It is not surprising that the Industrial Revolution began in Britain, with its use of coal.

We also know that there is a long-term correlation between world GDP growth and energy consumption.

Figure 3. X-Y graph of world energy consumption (from BP Statistical Review of World Energy, 2017) versus world GDP in 2010 US$, from World Bank.

The “flat period” in 1920-1940 in Figure 1 was likely problematic. The economy is a self-organized networked system; what was wrong could be expected to appear in many parts of the economy. Economic growth was likely far too low. The chance for conflict among nations was much higher because of stresses in the system–there was not really enough coal to go around. These stresses could extend to the period immediately before 1920 and after 1940, as well.

A Peak in Coal Production Hit the UK, United States, and Germany at Close to the Same Time

This is a coal supply chart for the UK. Its peak coal production (which was an all time peak) was in 1913. The UK was the largest coal producer in Europe at the time.

Figure 4. United Kingdom coal production since 1855, in a href=”http://www.davidstrahan.com/blog/?p=116″>figure by David Strahan. First published in New Scientist, 17 January 2008.

The United States hit a peak in its production only five years later, in 1918. This peak was only a “local” peak. There were also later peaks, in 1947 and 2008, after coal production was developed in new areas of the country.

Figure 5. US coal production, in Wikipedia exhibit by contributor Plazak.

By type, US coal production is as shown on Figure 6.

Figure 6. US coal production by type, in Wikipedia exhibit by contributor Plazak.

Evidently, the highest quality coal, Anthracite, reached a peak and began to decline about 1918. Bituminous coal hit a peak about the same time, and dropped way back in production during the 1930s. The poorer quality coals were added later, as the better-quality coals became less abundant.

The pattern for Germany’s hard coal shows a pattern somewhat in between the UK and the US pattern.

Figure 7. Source GBR.

Germany too had a peak during World War I, then dropped back for several years. It then had three later peaks, the highest one during World War II.

What Affects Coal Production?

If there is a shortage of coal, fixing it is not as simple as “inadequate coal supply leads to higher price,” quickly followed by “higher price leads to more production.” Clearly the amount of coal resource in the ground affects the amount of coal extraction, but other things do as well.

[1] The amount of built infrastructure for taking the coal out and delivering the coal. Usually, a country only adds a little coal extraction capacity at a time and leaves the rest in the ground. (This is how the US and Germany could have temporary coal peaks, which were later surpassed by higher peaks.) To add more extraction capacity, it is necessary to add (a) investment needed for getting the coal out of the ground as well as (b) infrastructure for delivering coal to potential users. This includes things like trains and tracks, and export terminals for coal transported by boats.

[2] Prices available in the marketplace for coal. These fluctuate widely. We will discuss this more in a later section. Clearly, the higher the price, the greater the quantity of coal that can be extracted and delivered to users.

[3] The cost of extraction, both in existing locations and in new locations. These costs can perhaps be reduced if it is possible to add new technology. At the same time, there is a tendency for costs within a given mine to increase over time, as it becomes necessary to access deeper, thinner seams. Also, mines tend to be built in the most convenient locations first, with best access to transportation. New mines very often will be higher cost, when these factors are considered.

[4] The cost and availability of capital (shares of stock and sale of debt) needed for building new infrastructure, and for building new devices made possible by new technology. These are affected by interest rates and tax levels.

[5] Time lags needed to implement changes. New infrastructure and new technology are likely to take several years to implement.

[6] The extent to which wages can be recycled into demand for energy products. An economy needs to have buyers for the products it makes. If a large share of the workers in an economy is very low-paid, this creates a problem.

If there is an energy shortage, many people think of the shortage as causing high prices. In fact, the shortage is at least equally likely to cause greater wage disparity. This might also be considered a shortage of jobs that pay well. Without jobs that pay well, would-be workers find it hard to purchase the many goods and services created by the economy (such as homes, cars, food, clothing, and advanced education). For example, young adults may live with their parents longer, and elderly people may move in with their children.

The lack of jobs that pay well tends to hold down “demand” for goods made with commodities, and thus tends to bring down commodity prices. This problem happened in the 1930s and is happening again today. The problem is an affordability problem, but it is sometimes referred to as “low demand.” Workers with inadequate wages cannot afford to buy the goods made by the economy. There may be a glut of a commodity (food, or oil, or coal), and commodity prices that fall far below what producers need to make a profit.

Figure 8. U.S. Income Shares of Top 10% and Top 1%, Wikipedia exhibit by Piketty and Saez.

The Fluctuating Nature of Commodity Prices

I have noted in the past that fossil fuel prices tend to move together. This is what we would expect, if affordability is a major issue, and affordability changes over time.

Figure 9. Price per ton of oil equivalent, based on comparative prices for oil, natural gas, and coal given in BP Statistical Review of World Energy. Not inflation adjusted.

We would expect metal prices to follow fossil fuel prices, because fossil fuels are used in the extraction of ores of all kinds. Investment strategist Jeremy Grantham (and his company GMO) noted this correlation among commodity prices, and put together an index of commodity prices back to 1900.

Figure 10. GMO Commodity Index 1900 to 2011, from GMO April 2011 Quarterly Letter. “The Great Paradigm Shift,” shown at the end is not really the correct explanation, something now admitted by Grantham. If the graph were extended beyond 2010, it would show high prices in 2010 to 2013. Prices would fall to a much lower level in 2014 to 2017.

Reason for the Spikes in Prices. As we will see in the next few paragraphs, the spikes in prices generally arise in situations in which everyday goods (food, homes, clothing, transportation) suddenly became more affordable to “non-elite” workers. These are workers who are not highly educated, and are not in supervisory positions. These spikes in prices don’t generally “come about” by themselves; instead, they are engineered by governments, trying to stimulate the economy.

In both the World War I and World War II price spikes, governments greatly raised their debt levels to fund the war efforts. Some of this debt likely went directly into demand for commodities, such as to make more bombs, and to operate tanks, and thus tended to raise commodity prices. In addition, quite a bit of the debt indirectly led to more employment during the period of the war. For example, women who were not in the workforce were hired to take jobs that had been previously handled by men who were now part of the war effort. (These women were new non-elite workers.) Their earnings helped raise demand for goods and services of all kinds, and thus commodity prices.

The 2008 price spike was caused (at least in part) by a US housing-related debt bubble. Interest rates were lowered in the early 2000s to stimulate the economy. Also, banks were encouraged to lend to people who did not seem to meet usual underwriting standards. The additional demand for houses raised prices. Homeowners, wishing to cash in on the new higher prices for their homes, could refinance their loans and withdraw the cash related to the new higher prices. They could use the funds withdrawn to buy goods such as a new car or a remodeled basement. These withdrawn funds indirectly supplemented the earnings of non-elite workers (as did the lower interest rate on new borrowing).

The 2011-2014 spike was caused by the extremely low interest rates made possible by Quantitative Easing. These low interest rates made the buying of homes and cars more affordable to all buyers, including non-elite workers. When the US discontinued its QE program in 2014, the US dollar rose relative to many other currencies, making oil and other fuels relatively more expensive to workers outside the US. These higher costs reduced the demand for fuels, and dropped fuel prices back down again.

Figure 11. Monthly Brent oil prices with dates of US beginning and ending QE.

The run-up in oil prices (and other commodity prices) in the 1970s is widely attributed to US oil production peaking, but I think that the rapid run-up in prices was enabled by the rapid wage run-up of the period (Figure 12 below).

Figure 12. Growth in US wages versus increase in CPI Urban. Wages are total “Wages and Salaries” from US Bureau of Economic Analysis. CPI-Urban is from US Bureau of Labor Statistics.

The Opposing Force: Energy prices need to fall, if the economy is to grow. All of these upward swings in prices can be at most temporary changes to the long-term downward trend in prices. Let’s think about why.

An economy needs to grow. To do so, it needs an increasing supply of commodities, particularly energy commodities. This can only happen if energy prices are trending lower. These lower prices enable the purchase of greater supply. We can see this in the results of some academic papers. For example, Roger Fouquet shows that it is not the cost of energy, per se, that drops over time. Rather, it is the cost of energy services that declines.

Figure 13. Total Cost of Energy and Energy Services, by Roger Fouquet, from Divergences in Long Run Trends in the Prices of Energy and Energy Services.

Energy services include changes in efficiency, besides energy costs themselves. Thus, Fouquet is looking at the cost of heating a home, or the cost of electrical services, or the cost of transportation services, in inflation-adjusted units.

Robert Ayres and Benjamin Warr show a similar result, related to electricity. They also show that usage tends to rise, as prices fall.

Figure 14. Ayres and Warr Electricity Prices and Electricity Demand, from “Accounting for growth: the role of physical work.”

Ultimately, we know that the growth in energy consumption tends to rise at close to the same rate as the growth in GDP. To keep energy consumption rising, it is helpful if the cost of energy services is falling.

Figure 15. World GDP growth compared to world energy consumption growth for selected time periods since 1820. World real GDP trends for 1975 to present are based on USDA real GDP data in 2010$ for 1975 and subsequent. (Estimated by author for 2015.) GDP estimates for prior to 1975 are based on Maddison project updates as of 2013. Growth in the use of energy products is based on a combination of data from Appendix A data from Vaclav Smil’s Energy Transitions: History, Requirements and Prospects together with BP Statistical Review of World Energy 2015 for 1965 and subsequent.

How the Economic Growth Pump Works

There seems to be a widespread belief, “We pay each other’s wages.” If this is all that there is to economic growth, all that is needed to make the economy grow faster is for each of us to sell more services to each other (cut each other’s hair more often, or give each other back rubs, and charge for them). I think this story is very incomplete.

The real story is that energy products can be used to leverage human labor. For example, it is inefficient for a human to walk to deliver goods to customers. If a human can drive a truck instead, it leverages his ability to deliver goods. The more leveraging that is available for human labor, the more goods and services that can be produced in total, and the higher inflation-adjusted wages can be. This increased leveraging of human labor allows inflation-adjusted wages to rise. Some might call this result, “a higher return on human labor.”

These higher wages need to go back to the non-elite workers, in order to keep the growth-pump operating. With higher-wages, these workers can afford to buy goods and services made with commodities, such as homes, cars, and food. They can also heat their homes and operate their vehicles. These wages help maintain the demand needed to keep commodity prices high enough to encourage more commodity production.

Raising wages for elite workers (such as managers and those with advanced education), or paying more in dividends to shareholders, doesn’t have the same effect. These individuals likely already have enough money to buy the necessities of life. They may use the extra income to buy shares of stock or bonds to save for retirement, or they may buy services (such as investment advice) that require little use of energy.

The belief, “We pay each other’s wages,” becomes increasingly false, if wages and wealth are concentrated in the hands of relatively few. For example, poor people become unable to afford doctors’ visits, even with insurance, if wage disparity becomes too great. It is only when wages are fairly equal that all can afford a wide range of services provided by others in the economy.

What Went Wrong in 1920 to 1940?

Very clearly, the first thing that went wrong was the peaking of UK coal production in 1913. Even before 1913, there were pressures coming from the higher cost of coal production, as mines became more depleted. In 1912, there was a 37-day national coal strike protesting the low wages of workers. Evidently, as extraction was becoming more difficult, coal prices were not able to rise sufficiently to cover all costs, and miners’ wages were suffering. The debt for World War I seems to have helped raise commodity prices to allow wages to be somewhat higher, even if coal production did not return to its previous level.

Suicide rates seem to behave inversely compared to earning power of non-elite workers. A study of suicide rates in England and Wales shows that these were increasing prior to World War I. This is what we would expect, if coal was becoming increasingly difficult to extract, and because of this, the returns for everyone, from owners to workers, was low.

Figure 16. Suicide rates in England and Wales 1861-2007 by Kyla Thomas and David Gunnell from International Journal of Epidemiology, 2010.

World War I, with its increased debt (which was in part used for more wages), helped the situation temporarily. But after World War I, the Great Depression set in, and with it, much higher suicide rates.

The Great Depression is the kind of result we would expect if the UK no longer had enough coal to make the goods and services it had made previously. The lower production of goods and services would likely be paired with fewer jobs that paid well. In such a situation, it is not surprising that suicide rates rose. Suicide rates decreased greatly with World War II, and with all of the associated borrowing.

Looking more at what happened in the 1920 to 1940 period, Ugo Bardi tells us that prior to World War I, the UK exported coal to Italy. With falling coal production, the UK could no longer maintain those exports after World War I. This worsened relations with Italy, because Italy needed coal imported from the UK to rebuild after the war. Ultimately, Italy aligned with Germany because Germany still had coal available to export. This set up the alliance for World War II.

Looking at the US, we see that World War I caused favorable conditions for exports, because with all of the fighting, Europe needed to import more goods (including food) from the United States. After the war ended in 1918, European demand was suddenly lower, and US commodity prices fell. American farmers found their incomes squeezed. As a result, they cut back on buying goods of many kinds, hurting the US economy.

One analysis of the economy of the 1920s tells us that from 1920 to 1921, farm prices fell at a catastrophic rate. “The price of wheat, the staple crop of the Great Plains, fell by almost half. The price of cotton, still the lifeblood of the South, fell by three-quarters. Farmers, many of whom had taken out loans to increase acreage and buy efficient new agricultural machines like tractors, suddenly couldn’t make their payments.”

In 1943, M. King Hubbert offered the view that all-time employment had peaked in 1920, except to the extent that it was jacked up by unusual means, such as war. In fact, some historical data shows that for four major industries combined (foundries, meat packing, paper, and printing), the employment index rose from 100 in 1914, to 157 in 1920. By September 1921, the employment index had fallen back to 89. The peak coal problem of the UK had been exported to the US as low commodity prices and low employment.

It was not until the huge amount of debt related to World War II that the world economy could be stimulated enough so that total energy production per capita could continue to rise. The use of oil especially became much greater starting after World War II. It was the availability of cheap oil that allowed the world economy to grow again.

Figure 17. Per capita energy consumption by fuel, separately for several energy sources, using the same data as in Figure 1.

The stimulus of all the debt-enabled spending for World War II seems to have been what finally encouraged the production of the oil needed to pull the world economy out of the problems it was having. GDP and Disposable Personal Income could again rise (Figure 18.)

Figure 18. Comparison of 3-year average change in disposable personal income with 3-year change average in GDP, based on US BEA Tables 1.1.5 and 2.1.

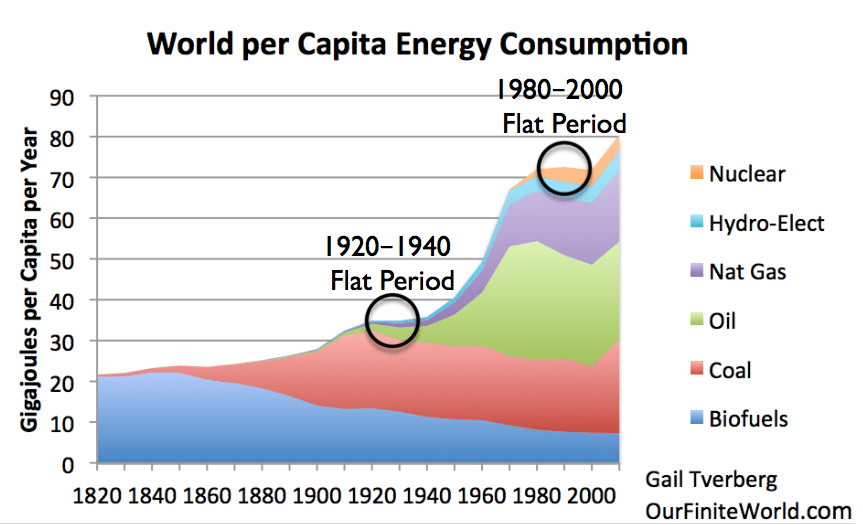

Furthermore, total per capita energy consumption began to rise, with growing oil consumption (Figure 1). This growth in energy consumption per capita seems to be what allows the world economy to grow.

I might note that there is one other exceptional period: 1980 to 2000. Space does not allow for an explanation of the situation here, but falling per capita energy consumption seems to have led to the collapse of the former Soviet Union in 1991. This was a different situation, caused by lower oil consumption related to efficiency gains. This was a situation of an oil producer being “squeezed out” because additional oil was not needed at that time. This is an example of a different type of economic disruption caused by flat per capita energy consumption.

Figure 19. World per Capita Energy Consumption with two circles relating to flat consumption. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects (Appendix) together with BP Statistical Data for 1965 and subsequent, divided by population estimates by Angus Maddison.

Conclusion

There have been many views put forth about what caused the Depression of the 1930s. To my knowledge, no one has put forth the explanation that the Depression was caused by Peak Coal in 1913 in the UK, and a lack of other energy supplies that were growing rapidly enough to make up for this loss. As the UK “exported” this problem around the world, it led to greater wage disparity. US farmers were especially affected; their incomes often dropped below the level needed for families to buy the necessities of life.

The issue, as I have discussed in previous posts, is a physics issue. Creating GDP requires energy; when not enough energy (often fossil fuels) is available, the economy tends to “freeze out” the most vulnerable. Often, it does this by increased wage disparity. The people at the top of the hierarchy still have plenty. It is the people at the bottom who find themselves purchasing less and less. Because there are so many people at the bottom of the hierarchy, their lower purchasing power tends to pull the system down.

In the past, the way to get around inadequate wages for those at the bottom of the hierarchy has been to issue more debt. Some of this debt helps add more wages for non-elite workers, so it helps fix the affordability problem.

Figure 20. Three-year average percent increase in debt compared to three year average percent increase in non-government wages, including proprietors’ income, which I call my wage base.

At this time, we seem to be reaching the point where, even with more debt, we are running out of cheap energy to add to the system. When this happens, the economic system seems more prone to fracture. Ugo Bardi calls the situation “reaching the inflection point in a Seneca Cliff.”

Figure 21. Seneca Cliff by Ugo Bardi

We were very close to the inflection point in the 1930s. We were very close to that point in 2008. We seem to be getting close to that point again now. The model of the 1930s gives us an indication regarding what to expect: apparent surpluses of commodities of all types; commodity prices that are too low; a lack of jobs, especially ones that pay an adequate wage; collapsing financial institutions. This is close to the opposite of what many people assume that peak oil will look like. But it may be a better representation of what we really should expect.

Can We Afford Renewable Energy?

https://www.linkedin.com/pulse/can-we-afford-renewable-energy-erico-matias-tavares/

Global Debt Hits Record $233 Trillion

https://www.bloomberg.com/news/articles/2018-01-05/global-debt-hits-record-233-trillion-but-debt-to-gdp-is-falling

https://techcrunch.com/2018/01/07/two-large-apple-shareholders-say-it-needs-to-research-the-impact-of-smartphones-on-kids/

A little late in the game to be questioning our tech obsessions and whether the negative aspects outweigh the positive (especially for children)…but a good move anyway.

Dear Ms. Tverberg, I have a question due to recent news:

News report Donald T. wants to increase off-shore oil exploration.

I wonder, how is the EROI, or efficiency, of off-shore oil drilling? As far as I concluded out of your blog and John Michael Greer’s and Nafeez Ahmed’s writings, fracking was a stunt that used existing resources, tools, materials in order to produce less energy than it actually cost in order to produce the inputs. So less than a zero sum game.

And off-shore oil? Could the US pull such a stunt a second time? Does anyone know about it, maybe Art Berman?

I would love to get much deeper into energy analysis, but my time is very limited and I don’t even know where to look. Nafeez Ahmed’s study was a relatively decent summary of what you did, mayber Norman Pagett’s works…it’s dificult to receive salient information on energy economics.

regards,

JH, that article is 12 years old…

That might have been his point.

Bed bugs only need blood to survive, and can travel easily on clothing and luggage. As people around the world travel more, bed bug infestations are also on the rise on almost every continent.

https://www.bloomberg.com/news/videos/2018-01-08/the-world-s-bed-bug-problem-is-getting-worse-video

Nasty brutish and short…. and miserable… for anyone alive post BAU

http://www.resilience.org/stories/2006-10-28/how-long-can-world-feed-itself/

“For the sixth time in the past seven years, the human race will grow less food than it eats this year. We closed the gap by eating into food stocks accumulated in better times, but there is no doubt that the situation is getting serious. The world’s food stocks have shrunk by half since 1999, from a reserve big enough to feed the entire world for 116 days then to a predicted low of only 57 days by the end of this year.”

Your link is from 2006, so this is 11 years ago. What happend?

http://www.bbc.com/news/world-asia-china-42600720

‘Burning tanker off Chinese coast ‘in danger of exploding’

“The tanker had been carrying an ultra-light form of oil known as condensate which in the case of a spill can be more dangerous for the environment than regular crude.

“Condensate is more likely to evaporate and mix in with the water,” John Driscoll of JTD Energy Services told the BBC.

“It also can be colour- and odourless – so it is a lot harder to detect, contain and clean up.”

Oh no, now we are going to find out what condensate does to the environment when that ship fully leaks its load.

The miracles of the CBs:

Greece 2yr Bond Yield lower than US 2yr Bond Yield

https://postachio-images.s3.amazonaws.com/969472f4-d209-4fa1-abb1-f1310f1f2c50/50301545-0c26-4782-8d26-36479f3fe630/60f7fa37-2558-4e1d-9beb-c1b24d1a1269.png

http://therealityofrisk.com/post/greek-2yr-trades-below-the-ust-2yr-wow

In Slovak:

https://finweb.hnonline.sk/komentare-a-analyzy/1671143-sialenstvo-na-dlhopisovych-trhoch-grecko-si-poziciava-lacnejsie-ako-usa

All that is considered not risky is below zero, so Greece a little bit above zero…

My understanding is the German’s came to the rescue and backed up the Greek bonds – maybe that’s why their perceived risk has declined.

Surely, the German’s armies of robots came to rescue them, too:

https://media.gettyimages.com/photos/robots-work-on-audi-cars-at-the-assembly-line-of-the-plant-of-german-picture-id156574564

Greece will br backed by Germany for at least two years and the dollar is expected to lose a little again the euro?

The weaker USD is better for the global economy – it means lower prices of energy.

Maybe you are correct.

I just wanted to make the case for 2yr greek:

– Germany backs Greece

– EU don’t collapse, at least not without US doing it also

– $ losing about .5% per year to €

Ha ha ha! I need to reach for a bucket about now…

Renewable Energy Needs Huge Mineral Supply

https://upload.wikimedia.org/wikipedia/commons/thumb/f/f4/The_Scream.jpg/1200px-The_Scream.jpg

…to match the power generated by fossil fuels or nuclear power stations, the construction of solar energy farms and wind turbines will gobble up 15 times more concrete, 90 times more aluminium and 50 times more iron, copper and glass. Right now wind and solar energy meet only about 1 percent of global demand; hydroelectricity meets about 7 percent.

…if the contribution from wind turbines and solar energy to global energy production is to rise from the current 400 terawatt hours to 12,000 terawatt hours in 2035, and 25,000 terawatt hours in 2050, that will require 3,200 million tons of steel, 310 million tons of aluminium and 40 million tons of copper to construct state-of-the-art generating systems.

This in turn would mean an annual increase in global production of these metals of from 5 percent to 18 percent for the next 40 years, and that would be in addition to the already accelerating demand for metals of all kinds in both the developed and the developing world.

https://gossipground.files.wordpress.com/2016/10/image.jpg

https://ic.pics.livejournal.com/eyeteeth/197241/2699/2699_320.jpg

I vote for the rat… looks a bit like a mini hippo

after the inevitable human extinction…

will the rats evolve to become the next self-conscious species?

yes, but everything will have a gnawed on look.

I have yet to see or hear more talk about the effects of peak oil on the armed forces. If any group of people has more to lose than any other in society it is the armed forces and I can’t for the life of me imagine them having no contingencies in place for that inevitable day. It raises many profound questions and yes I had a look through that German study on peak oil and its effects on the armed forces. It even discusses recycling lol

“The major part of military mobility in the Bundeswehr will thus most likely remain dependant on fluid fuels in the next decades. In the wake of peak oil, the use of fuels derived from biomass will become increasingly attractive. The capacities of such fuels are currently being expanded all over the world. This includes classic biofuels produced from agricultural products and/or waste materials. Their further development promises considerably higher yields per hectare. However, the use of these biofuels in particular has security implications, as discussed in Chapter 3.1.3. There have also been reports of promising attempts to produce biofuel from algae.206 Such systems could possibly have another advantage: fuel could be produced where it is required, thus reducing the need for transport into the area of deployment.207 A further advantage of the extensive use of biofuel would be that the drive propulsion systems of numerous transport and weapon systems – from aircraft to ships to main battle tanks and infantry fighting vehicles – would not necessarily have to be changed fundamentally but would merely have to be adapted.208”

https://permaculturenews.org/files/Peak%20Oil_Study%20EN.pdf

Any Generals or Admirals here in the mix of bloggers?

General David reporting for duty… (not really)…

the bottom line is that a military such as here in the USA will be darn sure that it gets the last oil, and enough to keep operating for many years ahead…

unless the leadership is clueless, which I doubt.

so Jerry…

are you a Creeping Collapser?

or an Instadoomer?

or, (gasp!) a Cornucopian?

The reason why Tesla has such a massive market cap…. is because it has a top secret agreement with the US military … to supply battery powered tanks, aircraft, and other vehicles post BAU…

Additionally Tesla is building massive solar farms complete with battery storage — as well as Total Recycling —- to allow the military to continue to function in perpetuity.

I was not supposed to tell anyone about this but I have a very flappy mouth….. I hope Assange has a spare room for me…. with a few Swedish vixens on hand?????

make a run for the Ecuadorian embassy there in NZ…

or yeah, fly to London.

Twilight Zone Time

https://www.zerohedge.com/news/2018-01-07/why-pension-funds-should-invest-bitcoin

Given that pensions will soon not exist… and most are way under-funded….and there is the chance of a home run in the short run —- maybe not such a bad idea.

I would also recommend using the cash to buy lottery tickets —- or punt it all on the Super Bowl

All investment is a lottery now, as the capital is consumed in bigger and bigger quantities.

We can no longer talk about reforming the system. The system is past reform. The wealth has been misallocated. The environmental destruction has been done. The irreversible climate change is happening. The energy supplies are dwindling. We are out of resources.

Cryptocurrencies: 1384

Market Cap: $819,562,015,506

all illusionary cryptocurrencies $820 billion…

should be $1 trillion in a few weeks or months.

Or 0.

ha!

I’m guessing $1 trillion, but who knows?

zero by 2030 sounds possible.

a good friend of mine used to comment regarding collapse that it would not happen in our lifetime. well, i just got word that he passed on today.

“… our lifetime.”

so…

how long for you?

hard to say, father died at 75, mother at 100. hoping i took after mom. genetic theory is on my side. in fact, since that is a 25 year spread, and i’m not near 75 yet, i can bet that we are going down much sooner than 2045. so maybe I will get to see the lights go out, permanently.

that’s why i tried to explain bitcoin here

https://extranewsfeed.com/bitcoin-24b3efd58ec

The Violent Afterlife of a Recycled Plastic Bottle

What happens after you toss it into the bin?

“Typically, 50% of what you put in your recycling bin is never recycled. It’s sorted and thrown out,” said Tom Szaky, CEO of TerraCycle, a recycling company. This is partly due to user error, a common problem which occurs when people place unrecyclable materials into recycling bins.***

https://www.theatlantic.com/technology/archive/2015/12/what-actually-happens-to-a-recycled-plastic-bottle/418326/

Did I mention that I recently checked on costs associated with recycling at my office in Hong Kong — and found a bill for over USD100 per month….. I ordered this contract to be terminated after the next collection.

This is a decidedly unpopular decision ….. yet try to explain that to a group of green-indoctrinated managers….. I think they are planning a movie called Scrooge 2 – the Anti Green Bad Guy

Fortunately — I am The Boss (as well as World Champion) — and in 2018 —- instead of paying to send all this sh it to China …. to be burned and buried in The Great Recycling Farce…. it will instead go with the normal garbage collection paid for in my tax bill.. to be burned and buried in China.

I would hope that none of it is recycled — because it is must more efficient to just make more stuff… from scratch.

Did I mention that someone said ‘but if we do that all isn’t all our garbage going to end up in the harbour’

If it did that would be an improvement… considering this is one of the most polluted bodies of water on earth….

When the toxicity of marine sediment in Hong Kong was evaluated, it was found that the seven sediments collected within Victoria Harbour were severely contaminated with heavy metals, at concentrations many times higher than those in sediments collected from outside the harbour. The highest metal content was recorded in site VS14 (located near the airport runway and the industrialized area), with copper, zinc, lead and chromium values of 3789, 610, 138 and 601 mg kg−1 dry wt, respectively. This site also had the greatest alkaline phosphatase activities (15 fluorescent intensity unit g−1 wet wt), the largest number of total coliforms (910 CFU g−1 wet wt) and sulphate-reducing bacteria (8.5 × 104 cells g−1 wet wt), implying that site VS14 was also contaminated with organic matter and nutrients.

https://www.sciencedirect.com/science/article/pii/0025326X96819278

And this is what happens to recycled electronic waste:

One key fear expressed by environmentalists is the seepage of toxic waste into the ground, contaminating the food chain. A pig farm sat next to one site, a field of crops by another.

In 2003 Leung and Puckett visited the Guiyi cluster of villages in Guangdong province, which had earned the dubious title of becoming the biggest electronic waste dump site in China – and possibly the world.

They saw “mom and pop” workshops dismantling computers and melting down plastic in large containers using what they described as primitive techniques, exposing workers to toxic materials and contaminating the soil and water. Footage of the site shows blackened streams, and soil samples were found to be contaminated with heavy metals and other pollutants.

More http://www.scmp.com/news/hong-kong/health-environment/article/1984534/revealed-toxic-trail-e-waste-leads-us-hong-kong

To summarize…. when you pay taxes or direct fees to recycle an old laptop …. what you are essentially paying for …. is to ship the laptop to a junk yard in China …. where they remove a few of the components that can actually be reused or recycled profitably…. and the vast majority of the components are smashed and tossed into a rubbish heap … where the toxic ingredients leach into the soil and water.

http://www.scmp.com/sites/default/files/styles/486w/public/images/methode/2016/07/03/58ede25c-4075-11e6-8294-3afaa7dcda6c_486x.jpg?itok=WTB0LfDl

And of course Africa gets a taste …

Video: Workers filmed dumping glass bottles intended for recycling into trash

In March 2013, street cleaners employed by the government were caught illegally throwing away items intended for recycling into landfills together with general waste.

Rather than being dumped at landfills, local materials to be recycled are meant to be “exported for overseas processing”, according to NGO Green Power.

https://www.hongkongfp.com/2015/07/29/video-workers-filmed-dumping-glass-bottles-intended-for-recycling-into-trash/

This is what happens —- when there is no profit to be made in recycling — because it makes no sense…. it encourages companies to low bid contracts…. then dump shit where it should have been dumped in the first place

I guess the only consolation is that 5 million years from now the Earth will be pristine again.

Yep… the earth has a very effective recycling program…..

I have just realized… I am the ultimate pariah:

– anti-recyling

– pro coal and oil

– antil-EVs

– anti-solar and wind power

– anti-Elon Musk

– Goblworming is fake

– MSM is purveyor of fake

– pro consumerism

– pro population growth

Did I miss anything?

iceages also fake

I am not anti ice age.

Oh one more…

– atheist

and ocean acidification. Not happening.

“there are certain advantages in being cursed by all and sundry … especially, it dispenses you with having to be nice to anybody … there’s nothing more emollient, stultifying, emasculating than wanting to be liked … “not nice!” … that does it, you’re free! …”

― Louis-Ferdinand Céline, North

You don’t hate Donald Trump or Teresa May enough?

I politely turned down a New Year invitation from a renewables advocate “to commiserate about the depths that the governments in the US and UK have fallen to” over a beer or two.

My New Year’s resolution is to disengage from bickering and let the grumblers and the green progressives get on with it. Had I gone for a drink, I would have only told my friend…

https://youtu.be/4ZV3kGRY1j0

I had a very politically incorrect new years eve (I am usually asleep well before midnight)…. in a hole in the wall bar on the west coast … I was the only one without a big beard (well…and M Fast…) …. mega marijuana being puffed in the open … plenty of profanity … most were completely hammered (in some instances crawling drunk) … and everyone drove home (all back roads with no cops…) … and best of all — nobody counted down midnight…. I always hated that….

Our metaphorical asteroid is all too visible to anyone brave enough to look up. Our decision not to address our problems back in the 1970s when scientists first warned us about them has proved to be a serious error of judgement.

I am sorry. Even if we had attempted to address our problems back in the 1970s, we could have done virtually nothing. We are dealing with the laws of physics. The people writing Limits to Growth were far too optimistic on what could be done. They were proposing severely limiting population at that time–figuring out how many people would die each year, and allowing only that many births, so many families would have only one child. There were many other very optimistic assumptions. What they were proposing were as unrealistic as what we hear people proposing today.

You’ve answered my question. Thanks

What could they have done?

Had I been sufficiently alarmed after first hearing Paul Ehrlich’s warnings in the early 1970s, I could have urged BabyDoomer’s mum to abort him. But if she’d have listened and made that sacrifice, it would have made no measurable difference to humanity’s roller-coaster ride and we would all be so much the poorer for his subsequent absence from this forum.

Why stop there.

All Green Groopies could have been offered free sterilization…

Now this is funny….

In that Penn and Teller video about recycling…. they keep adding to the number of recycling bins to the point of where there are around 10 different coloured ones… each for different rubbish… and the Green Groopies keep nodding yes… this is fine…. this is ok … I can do it…. no matter how onerous … they would agree to it….

Now imagine how these clowns would react if they were informed that there is a much more effective way to save the environment …. that would reduce trash exponentially….

The Green Groopies lean in … with their best keener faces …. tell us Fast Eddy…. World Champion that you are….. tell us how we can save the world!!!!

Well …. if ya’ll can just pull your pants down….. we’ll give you a shot to numb the area… then we’ll just snap your balls off… so that you cannot introduce any new consumers to the planet….

https://perfectionplus.com/wp-content/uploads/2017/01/Kelly_scissors_curved.png

http://l450v.alamy.com/450v/dtkwjn/close-portrait-on-the-face-of-a-funny-man-with-crazy-surprised-look-dtkwjn.jpg

Can’t someone just punch the data into Excel and compute when it’s over? I’m half serious, since really we’re dealing with a lot of things that can be measured quite well…

If the peak oilers were wrong, then for f**s sake correct the error and put up the new chart!!

so you ask!

I have done exactly that data computation…

and…

in spite of what adonis says…

my 100% reliable result is that The Collapse will happen July 7, 2027…

so…

happy now?

Great that feels better. Here is at least one place to track your prediction:

https://ycharts.com/indicators/world_crude_oil_production

81 million barrels of oil per day…

times 42 gallons per barrel…

let’s see… 80 x 40 = 3200 so…

3200 million gallons… wow… per day… wow…

I wouldn’t worry until it drops below 3000 million per day.

The volumes are incredible…. it amazes me that there can be that much oil in the ground….

I have another good idea…

let’s burn all of it…

https://www.indexmundi.com/energy/?product=gasoline&graph=production-growth-rate

Data stops at 2012. Very irritating…

I can live with that…

The end of cheap oil sits alongside a rapid increase in climate-related extreme weather events, food and water stress, resource depletion and economic overload to create a situation that threatens the very life support systems that we have come to depend upon. Nevertheless, our complete dependency upon several irreplaceable critical infrastructure systems leaves us highly vulnerable to a rapid, cascading collapse that our political leaders and their economic advisors are unlikely to understand even as our civilisation collapses around them.

-Watkins, Tim

true enough…

the 2030s will be tough.

‘our political leaders and their economic advisors are unlikely to understand even as our civilisation collapses around them’

They are doing exactly as one would expect them to do – when faced with an Apocalyptic outcome …. they are throwing gasoline on the fire….

Because when the fire goes out….. we die

Tim clearly does not understand that

As M. King Hubbert (1962) shows, Peak Oil is about discovering less oil, and eventually producing less oil due to lack of discovery.

https://imgur.com/a/6dEDt

IEA Chief warns of world oil shortages by 2020 as discoveries fall to record lows

https://www.wsj.com/articles/iea-says-global-oil-discoveries-at-record-low-in-2016-1493244000

Saudi Aramco CEO sees oil shortage coming as investments, oil discoveries drop

https://www.reuters.com/article/us-aramco-oil/aramco-ceo-sees-oil-supply-shortage-as-investments-discoveries-drop-idUSKBN19V0KR

And what would be the results of world oil shortage?

German Military (leaked) Peak Oil study: oil is used in the production of 95% of all industrial goods, so a shortage of oil would collapse the world economy & world governments

https://www.permaculture.org.au/files/Peak%20Oil_Study%20EN.pdf

Now you know when and what will cause the economic collapse….

Actually, a shortfall in coal use, simply because we think it produces too much CO2, will have precisely the same effect.

There is in much economic and political discourse a strong belief that there remains a guarantee of rising living standards so long as policy is correctly set in the circumstances of the new world to achieve them. Yet any assumption that there must be a way out of the present economic crisis that returns the West to steady year-on-year growth punctured only by relatively short recessions is hard to justify. Such a faith rests on denying even the possibility that the ongoing rise in material living standards witnessed

Over the past two centuries is coming to an end, or indeed that the carrying capacity of the earth may be less than the material expectations of the world’s sharply rising population. History suggests such a faith has no foundations in past experience. What happens to this presumption as the fallout of the multiple problems around oil at work play out will challenge expectations of democracy and the idea that time guarantees progress.

The shift, however, from high debt to high debt sustained by QE and ZIRP has taken western states into unprecedented territory. Under these conditions any presumption that economic problems can ultimately always be addressed is likely to be tested to destruction over the next few decades. What happens to this presumption as the fallout of the multiple problems around oil at work play out will also challenge expectations of democracy.

But democracy cannot stay the geological limits of shale production or alter the credit requirements they engender. Moreover, the predicaments that now confront democratic governments around oil are significantly more difficult than those they faced in the twentieth century before conventional oil production stagnated. Since there can be no return to an oil price that is sustainable in relation to the economic capacity and political power of net-consuming and net-producing states, managing oil and its fallout has become a permanent economic

Nonetheless, if the stagnation of conventional oil production around the middle of the last decade has yielded immense predicaments for western democracies to navigate we should, not be surprised. For several centuries the material viability of human life as lived in western societies has depended on access to energy sources created millions of years before human life began. It is a supreme irony that the concept of progress with its near metaphysical inflation of human agency to providential status has been sustained through a time of vastly increased material living standards that was made possible by the geological storage of ancient sunlight. Many hope that human ingenuity will provide an escape from the possibility that the West’s material progress is ultimately bound by limits dictated by that energy supply, whether those limits arise from its physical production or the disruption to the biosphere of burning it. However, whether this hope is plausible or not, the economic and geo-political world that oil dependency has hitherto made cannot be undone, and its consequences will endure across the spheres of collective life for many years to come.

-Thompson, Helen. Oil and the Western Economic Crisis

(Building a Sustainable Political Economy: SPERI Research & Policy) (Cambridge University, UK). Springer International Publishing.

It was also telling for me to see that shortly after the closing of the Alberta Oilsands and what shows up in the news? A picture of a brand new built offshore oil platform heading out into the Atlantic from none other than Nova Scotia. I guess the oil companies can’t have it both ways, mining for oil and drilling for it offshore at the same time along with I guess all the fracking? It all comes down to what can we afford to do now and for how long? Next to this is all of the amalgamation of companies which at one time were bitter rivals. Those days are long gone I’m afraid and it all only proves the truth of Gail’s hypotheses about affordability.

The problem is being fixed with the combination of rising the debt and lowering the prices of the energy. When, simultaneously, the debt levels fall and energy prices rise, we have a big problem…

The dependence on cheap energy, including cheap workforce, is forming slowly, then accelerates, and, finally, the collapse comes unavaited: all of suddeny, there is nothing/no one to help you.

That is the way how it happens: you believe that you are powerful, but it is always the external energy that makes you strong.