The most prevalent view regarding future oil supply, as well as total energy supply, seems to be fairly closely related to that expressed by Peak Oilers. Future fossil fuel supply is assumed to be determined by the resources in the ground and the technology available for extraction. Prices are assumed to rise as fossil fuels are depleted, allowing more expensive technology for extraction. Substitutes are assumed to become possible, as costs rise.

Those with the most optimistic views about the amount of resources in the ground become especially concerned about climate change. The view seems to be that it is up to humans to decide how much energy resources we will use. We can easily cut back, if we want to.

The problem with this approach is the world economy is much more interconnected than most analysts have ever understood. It is also much more dependent on growing energy supply than most have understood. Surprisingly, we humans aren’t really in charge; the laws of physics ultimately determine what happens.

In my view, Peak Oilers were correct about energy supplies eventually becoming a problem. What they were wrong about is the way the problem can be expected to play out. Major differences between my view and the standard view are summarized on Figure 1.

Figure 1. Prepared by Author.

Let me explain some of the issues involved.

[1] Modeling is a lot more difficult than it looks.

Let’s take one common model of the part of the earth where we live, a street map:

Figure 2. Source: Edrawsoft.com

If we want to scale the model up to cover the whole world, we need to add a whole new dimension. In other words, we need to make a globe.

The same problem occurs with what seem to be simple economic models, like supply and demand:

Figure 3. From Wikipedia: The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

If we are trying to model the situation a long way from limits (running out, or whatever the real limit is) then this model is perhaps “good enough.”

But if energy is the item that is in scarce supply as we approach limits, it can affect both quantity and price. Lack of energy supply at an inexpensive enough price can reduce both the quantity of the goods produced and the wages of workers. For example, distributors of goods in the United States may choose to buy imported goods from China or India to work around the problem of too high a cost of production (including energy costs).

The resulting competition with low-wage countries reduces the wages of many workers, especially those with low skill levels and those just finishing their educations. With such low wages, workers cannot afford to buy as many cars, motorcycles, and other goods that use energy products. The lack of demand from these workers indirectly brings down the prices of commodities of all kinds, including oil. In fact, prices can fall below the cost of production for extended periods. This has happened since 2014 for many energy products, including oil.

The model by the economists isn’t right. It doesn’t have enough dimensions to it. Peak Oil researchers did not understand that economists had put together a badly incomplete model. Their model only represents simple cases away from energy limits. Their model doesn’t explain what we should expect near energy limits.

[2] Simple two-dimensional models can work for some purposes, but not for others.

One thing that has been confusing to Peak Oil researchers is the base model in the 1972 book The Limits to Growth seems to present a fairly accurate timeline regarding when energy limits might hit. The indications are that the limits will happen about now.

The model reflects a simple, quantity-based approach that does not consider problems such as how debt might be repaid with interest if the economy is shrinking, or how pension payments would fare in a shrinking economy. The model is based on the assumption that our problem is only inadequate supply, not economic problems that indirectly result from short supply.

Figure 4. Base scenario from 1972 Limits to Growth, printed using today’s graphics by Charles Hall and John Day in “Revisiting Limits to Growth After Peak Oil” http://www.esf.edu/efb/hall/2009-05Hall0327.pdf

The thing that is easy to miss is the fact that this model is too simple to show how the limits will hit. For example, will the limits apply to oil or all fuels combined? What will be the impact on wage disparity? How will the impact on wage disparity affect demand for goods and services? Will the economy start growing too slowly and fail for that reason?

The authors of The Limits to Growth wisely pointed out that their models could not be relied on to show what would happen after collapse, but this warning seems to have been missed by many readers. I have suggested that it might have been better if the model had been truncated at an earlier date, to emphasize how limited the model’s predictive abilities really are because of its omission of a financial system that includes debt, wages, and prices.

Figure 5. Limits to Growth forecast, truncated shortly after production turns down, since modeled amounts are unreliable after that date.

[3] Energy is a critical need for the economy. Many prior economies collapsed when energy consumption stopped rising sufficiently rapidly.

Much research has been done on the huge number of historical economies that have collapsed. Peter Turchin and Sergey Nefedov examined eight agricultural economies that collapsed. This is a chart I prepared, explaining the approximate timing of the eight collapses, and the population growth pattern that seemed to occur.

Figure 6. Chart by author based on Turchin and Nefedov’s Secular Cycles.

According to Turchin and Nefedov, when a new resource became available (for example, land available after cutting down trees, or a new discovery of improved food yields because of irrigation), the population grew rapidly until the population reached the carrying capacity of the land with the new resource. The carrying capacity would reflect the energy resources that were easily available: land for farming and biomass that could be harvested and burned.

As limits were reached, population growth tended to plateau. The plateau would tend to come when the area could only support its existing population, without adding some sort of complexity to try to produce more goods and services using the existing energy resources. Joseph Tainter, in The Collapse of Complex Societies, tells us that by adding complexity (including improved technology, larger businesses and expanded government functions), it was possible to increase the output of the economy over what initially seemed to be available. There are at least two reasons why using technology to work around natural limits doesn’t work for very long, however:

[a] There are diminishing returns to adding new technology. Eventually, it costs more to add technology than its benefit is worth.

[b] Growing technology is associated with growing wage disparity. New technology replaces some jobs. Some new jobs may be high paying (managers, highly trained technical people), but if growth in economic output is not sufficient, a disproportionate share of the jobs may be very low-paying. In fact, some former workers may be left without jobs because technology replaces earlier jobs.

History shows that there are many things that contribute to the collapse of economies:

[a] Governments cannot collect sufficient taxes, because as wage disparity grows, many workers are increasingly impoverished and can barely support themselves.

[b] The slow economic growth rate makes it difficult to repay debt with interest.

[c] Investments in new businesses don’t pay enough to make them worthwhile.

[d] The health of the marginalized lower-paid workers deteriorates, at least partly because of poorer nutrition. They tend to catch diseases more easily, and epidemics spread farther.

[e] Prices of essential goods may fall below the cost of production because of wage disparity among workers. The lower-paid workers cannot afford to buy very many goods and services. Because these workers cannot afford many goods and services, the price of commodities used in creating these goods and services falls.

[f] The economy has less resilience against chance variations, such as temporary variability in climate, or a neighbor that suddenly has a stronger army, if the economy is operating near its carrying capacity. A problem that might not have brought the economy down may bring it down, because of a lack of reserves to handle chance fluctuations.

[4] We get evidence of a need for rising energy consumption per capita by analyzing the ratio of US wages to GDP, and how it has fallen over the years.

Figure 7. US wages as a percentage of GDP (based on BEA data) compared to Brent oil price in $2016 dollars, based on BP Statistical Review of World Energy data.

If the only energy need of humans were food, we would expect human per capita energy consumption to be flat. The issue, however, is that humans are not living within normal food limits of the economy. Humans gained an initial advantage over other plants and animals over one million years ago, when they learned to burn biomass and use it for many purposes (cooking food to get more energy value, scaring away predators and catching prey, expanding the range of humans to colder climates).

Now, humans must maintain their earlier advantage over other species, or they will lose the contest to some predator, such as microbes. With today’s huge population, maintaining humans’ prior advantage requires a surprising amount of energy supplies, in addition to food energy.

Human labor represents only part of the economy. Figure 7 shows that wages as a percentage of GDP were fairly flat between 1940 and 1970, when oil prices were low, and oil was in abundant supply. The big drop in the ratio of wages to GDP started after 1970, when oil prices have been higher. To work around the problem of higher oil prices, the economy has become more complex: businesses and governments have grown; international trade has become more important; debt and the financial system have taken on a greater role.

If, over the long term, wages have been falling as a percentage of GDP, then the remainder of the economy is growing even faster. Government is growing. The size of businesses and the amount of technology used by those businesses, is increasing. All of these things need to be supported, indirectly, by energy products. For these reasons, energy consumption needs to grow faster than population, even if technology is making individual processes more efficient.

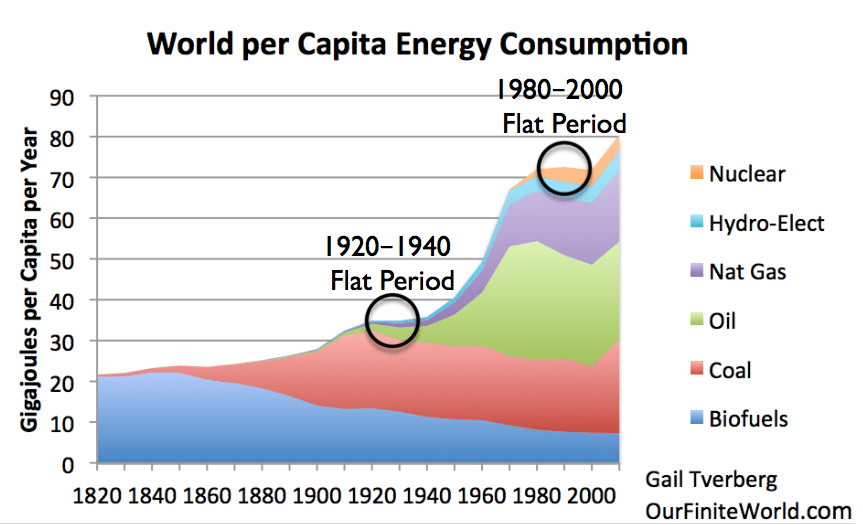

[5] Analysis of historical data since 1820 shows what happens when the world economy hits flat spots in per capita energy consumption.

Figure 8. World per Capita Energy Consumption with two circles relating to flat consumption. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects (Appendix) together with BP Statistical Data for 1965 and subsequent, divided by population estimates by Angus Maddison.

The 1920-1940 Flat Period was definitely a period of “not enough energy to go around.” The Great Depression of the 1930s was a time of little GDP growth and great wage disparity. There is evidence that both World War I and World War II (coming immediately before and immediately after the 1920-1940 period) were, indirectly, energy wars.

The 1980-2000 Flat Period represents a time when the US and Europe both intentionally reduced their oil consumption because it was feared that oil would be in short supply in the future. This was a period that required huge debt growth to make the necessary changes (Figure 9).

Figure 9. Growth in US Wages vs. Growth in Non-Financial Debt. Wages from US Bureau of Economics “Wages and Salaries.” Non-Financial Debt is discontinued series from St. Louis Federal Reserve. (Note chart does not show a value for 2016.) Both sets of numbers have been adjusted for growth in US population and for growth in CPI Urban. As mentioned previously, it is also the period that a huge amount of complexity was added, and wages fell as a percentage of GDP. It is doubtful this pattern could be repeated again, without serious economic problems occurring

There were other problems in the 1980 to 2000 period. The collapse of the central government of the Soviet Union occurred in 1991. Low oil prices for several years prior to the collapse reduced the revenue of the Soviet Union. This seems to have been a major contributor to the collapse. Oil exporters are again encountering the issue of inadequate tax revenue, as a result of low oil prices since 2014.

[6] It is total energy growth (not simply oil consumption growth) that correlates well with GDP growth.

Figure 10. X-Y graph of world energy consumption (from BP Statistical Review of World Energy, 2017) versus world GDP in 2010 US$, from World Bank.

Peak Oil followers haven’t stopped to think through how the economy works. It is really the growth of total energy that we need to be concerned about, from the point of view of operating the economy.

[7] Indirectly, debt and asset prices are promises of future energy consumption.

We don’t think of debt as a promise of future energy consumption. The connection comes because debt can only be redeemed (through a financial transaction) for future goods and services. Making these future goods and services will require energy consumption.

The same principle applies to asset prices of all kinds: prices of shares of stock, home prices, land prices, and pension values. If an asset-owner wants to sell an asset and use the proceeds to buy other goods and services, the asset-owner encounters the same situation as the bond-owner: the goods and services that will be provided in exchange depend on the energy supplies available at the date of the exchange. Thus, indirectly, the prices represent promises of future energy consumption.

[8] One essential part of the economic growth system seems to be an ever-falling price of energy services, where energy services are defined as the cost of energy, plus whatever efficiency savings are available that make the cost of energy services less expensive.

For example, the cost of transporting a 100 kg. package 100 kilometers, or of heating a 100 square meter residence for a winter, must keep falling. If this happens, businesses can afford to buy ever more tools for their workers. With these tools, the workers can become ever more productive.

Furthermore, because of their growing productivity, workers find that their wages are rising, so that they can buy ever more goods and services. In this way, demand continues to rise. Changes such as these allow the economy to keep growing.

Figure 11. Energy services chart is by Roger Fouquet, from Divergences in Long Run Trends in the Prices of Energy and Energy Services. Second chart is figure from UNEP Global Material Flows and Resource Productivity.

In fact, the prices of energy services do seem to keep falling, even if the cost of providing these services is not falling. This is a major reason why energy prices seem to have fallen below the cost of production for practically every type of energy in recent years. This situation is not sustainable; it can be expected to lead to the collapse of the system.

[9] If the growth rate of the economy is not fast enough, the danger is that the economy will collapse.

We can think of the GDP situation as being similar to that of a bicycle. GDP needs to be rising rapidly enough, or the economy will collapse. A bicycle needs to be traveling fast enough, or it will fall over. Economists often talk about an economy slowing to stall speed.

Figure 12. Author’s view of analogies of speeding upright bicycle to speeding economy.

Reported world GDP growth rates in recent years are likely somewhat overstated for several reasons.

- World GDP represents a weighting of country reported GDP. One approach to weighting gives disproportionate influence to China, India, and other developing countries.

- The use of Quantitative Easing and of higher government debt temporarily inflates the quantity of goods and services an economy can make.

- Artificially low energy prices give a boost to oil importing counties. They also keep the prices of goods and services artificially low, compared to wages. These artificially low energy prices cannot continue without the failure of governments of oil exporters, and without businesses producing energy products collapsing.

Whether or not the economy can continue operating is determined by the economy itself, because the economy is a self-organized system. Its continued operation doesn’t depend on published statistics of varying quality.

[10] Researchers studying oil limits thought that they had found a whole new phenomenon, “Peak Oil.”

In fact, they had found a special case of a phenomenon that tends to lead to collapse, namely, conditions that lead to energy consumption per capita that is not rising rapidly enough. Such conditions can occur in many different ways, such as these:

[a] Population rises sufficiently that it is hard to keep energy consumption per capita rising. This seems to be a major problem in many historical collapses.

[b] Collapse indirectly comes from diminishing returns in energy extraction. The standard workaround for diminishing returns is growing use of complexity (including technology). This tends to encourage the non-wage portions of the economy to grow, as in Figure 7. Adding complexity becomes increasingly expensive for the benefit obtained. Ultimately, wage disparity and falling commodity prices become a problem, and the system collapses.

[c] Random fluctuations in climate occur. An economy collapses because it doesn’t have the strength to respond to such random fluctuations.

[11] Peak oil researchers did the best they could, with the limited understanding of the day. The unfortunate problem was that the model they put together wasn’t really correct.

The fundamental problem of the Peak Oil researchers was that the economic researchers, upon whom they depended, did not really understand the interconnected nature of the economy. They continued to use two-dimensional economic models, when they needed multidimensional models. Economists predicted that prices would rise near limits, when it is increasingly clear that this cannot be true. The world has been struggling with low prices for many commodities since 2014. Prices now are temporarily less low, but they still are not high enough to allow adequate tax revenue for oil exporting countries.

The Energy Return on Energy Invested (EROEI) Model of Prof. Charles Hall depended on the thinking of the day: it was the energy consumption that was easy to count that mattered. If a person could discover which energy products had the smallest amount of easily counted energy products as inputs, this would provide an estimate of the efficiency of an energy type, in some sense. Perhaps a transition could be made to more efficient types of energy, so that fossil fuels, which seemed to be in short supply, could be conserved.

The catch is that it is total energy consumption that matters, not easily counted energy consumption. In a networked economy, there is a huge amount of energy consumption that cannot easily be counted: the energy consumption to build and operate schools, roads, health care systems, and governments; the energy consumption required to maintain a system that repays debt with interest; the energy consumption that allows governments to collect significant taxes on exported oil and other goods. The standard EROEI method assumes the energy cost of each of these is zero. Typically, wages of workers are not considered either.

There is also a problem in counting different types of energy inputs and outputs. Our economic system assigns different dollar values to different qualities of energy; the EROEI method basically assigns only ones and zeros. In the EROEI method, certain categories that are hard to count are zeroed out completely. The ones that can be counted are counted as equal, regardless of quality. For example, intermittent electricity is treated as equivalent to high quality, dispatchable electricity.

The EROEI model looked like it would be helpful at the time it was created. Clearly, if one oil well uses considerably more energy inputs than a nearby oil well, it would be a higher-cost well. So, the model seemed to distinguish energy types that were higher cost, because of resource usage, especially for very similar energy types.

Another benefit of the EROEI method was that if the problem were running out of fossil fuels, the model would allow the system to optimize the use of the limited fossil fuels that seemed to be available, based on the energy types with highest EROEIs. This would seem to make best use of the fossil fuel supply available.

[12] There are corrections to the EROEI method that might allow it to work in the manner that it should. The catch is that these corrections seem to show wind and solar not to be solutions to our problems. In fact, the system is so integrated, and our need for rising energy consumption per capita so great, that it is doubtful that any substitute for fossil fuels can really be a solution.

Professor Hall observed that if a fish had to swim too far to get food, it could not use very much of the food’s energy to catch the food, because most of its energy was needed for everyday metabolism and reproduction. A fish would typically need an EROEI of at least 10:1 for catching its prey, if it expected to have enough energy left to cover its full metabolic needs (including reproduction), plus the energy required to catch its prey.

If catching some prey only provided an energy return of 1:1, it would be pretty much worthless as a food source, since it would not cover any of the metabolic costs. Certainly, it would not make sense to call any energy in excess of an EROEI of 1:1 “net energy,” because it makes no contribution to covering a fish’s metabolic or reproduction activities. “Net energy” should only come from food sources with an EROEI very close to, or above, a ratio of 10:1.

A similar approach can be used to incorporate the large amount of energy that is lost by zeroing out the equivalent of the metabolism of the fish, for the economy. Based on Figure 11, the required average EROEI (to match what the economy can afford to pay for) needs to rise over time. Thus, if the required average EROEI is 10:1 now, it might be 11:1 later, simply because the increasingly complex world economy needs energy services that are becoming ever less expensive.

The story, “Higher energy prices will work in the future” is simply a myth, created by economists who do not understand how the economy really operates, considering all of the feedbacks involved. In inflation-adjusted terms, the price of energy services needs to keep falling as a percentage of GDP, to keep the system operating.

To fix the net energy calculation, some suitable minimum EROEI ratio for the economy needs to be determined–probably about 10:1–to incorporate the large share of energy consumption that is missing from the economy. Net energy would be then determined as the energy in excess of 10:1 EROEI, rather than in excess of 1:1 EROEI. This approach would make solar and wind look much less beneficial than most calculations to date.

In the case of intermittent renewables, a determination needs to be made whether the role of wind or solar in a particular situation is to replace electricity or fuel. If the role is to replace electricity (as is generally the case), then sufficient buffering must be provided in the model, so that the model can calculate the proper EROEI for dispatchable electricity (not intermittent electricity). Adding buffering will generally substantially reduce the EROEIs of intermittent electricity types. This adjustment makes it clear that there is much less benefit of wind and solar.

If the purpose of the intermittent electricity is only to replace fuel (such as a proposed new Saudi solar installation), then there is no need for buffering in the calculation. Of course, a cost comparison could also be used, and this might be the simpler approach. The cost comparison will generally be favorable if the fuel being replaced is oil, because oil is a high-priced fuel.

Too often, wind or solar is added to the system in a way that overlooks the real cost of buffering. Coal and nuclear electricity production find themselves with the unpaid job of providing buffering services for wind and solar. The net impact of adding intermittent renewables is that they push necessary backup power out of business. We end up with an electrical system that is worse off for adding intermittent renewables, even though this was not the intent of those requiring the use of such generation.

Conclusion

The number one need of the world economy is rising per capita energy consumption. In order to maintain economic growth, the price of energy services needs to fall as a percentage of GDP. The system will try to rebalance to the least expensive cost of energy production using globalization and other techniques. When this is no longer possible, the current world economic system is likely to fail.

Peak Oil modelers did not understand how complex our economy is. In their defense, no one else did either, especially back in the 1970 to 2005 era. They did the best they could, using the models that economists had put together. Because of the assumption of ever-rising energy prices, Peak Oil models assume that far more fossil fuels are extractable than is likely to really be the case. Optimists (oil companies, politicians, government agencies) assume even higher extraction of fossil fuels than is reasonable. The result is considerable concern about climate change.

When a person realizes how tightly integrated the world economy is, and its need to grow, it becomes clear that using less is not a solution. Prices of commodities would plunge even farther below the cost of production. The economic system would experience a far worse recession than the Great Recession of 2008-2009. Some governments would fail. The spiral might permanently be downward.

Standard solutions don’t work either. Substitutes don’t scale up quickly. Biomass cannot be used heavily because the world’s ecosystems depend on biomass; we are already using more than our share. Intermittent renewables such as wind and solar have their own high energy cost, but it is hard to count. They depend on international trade to make and repair the devices. They depend on debt for financing. They are really only part of the fossil fuel system, contrary to what the name “renewables” would suggest.

Energy modelers did their best. Unfortunately, with modeling it is hard to see what is going wrong. This is especially true when the academic world is divided into silos, each of which tends to look primarily at the writings of the people in its own field. It is easy for an incorrect model to get firmly embedded into people’s minds.

The new political divide

Farewell, left versus right. The contest that matters now is open against closed

AS POLITICAL theatre, America’s party conventions have no parallel. Activists from right and left converge to choose their nominees and celebrate conservatism (Republicans) and progressivism (Democrats). But this year was different, and not just because Hillary Clinton became the first woman to be nominated for president by a major party. The conventions highlighted a new political faultline: not between left and right, but between open and closed (see article). Donald Trump, the Republican nominee, summed up one side of this divide with his usual pithiness. “Americanism, not globalism, will be our credo,” he declared. His anti-trade tirades were echoed by the Bernie Sanders wing of the Democratic Party.

America is not alone. Across Europe, the politicians with momentum are those who argue that the world is a nasty, threatening place, and that wise nations should build walls to keep it out. Such arguments have helped elect an ultranationalist government in Hungary and a Polish one that offers a Trumpian mix of xenophobia and disregard for constitutional norms. Populist, authoritarian European parties of the right or left now enjoy nearly twice as much support as they did in 2000, and are in government or in a ruling coalition in nine countries. So far, Britain’s decision to leave the European Union has been the anti-globalists’ biggest prize: the vote in June to abandon the world’s most successful free-trade club was won by cynically pandering to voters’ insular instincts, splitting mainstream parties down the middle.

News that strengthens the anti-globalisers’ appeal comes almost daily. On July 26th two men claiming allegiance to Islamic State slit the throat of an 85-year-old Catholic priest in a church near Rouen. It was the latest in a string of terrorist atrocities in France and Germany. The danger is that a rising sense of insecurity will lead to more electoral victories for closed-world types. This is the gravest risk to the free world since communism. Nothing matters more than countering it.

Higher walls, lower living standards

Start by remembering what is at stake. The multilateral system of institutions, rules and alliances, led by America, has underpinned global prosperity for seven decades. It enabled the rebuilding of post-war Europe, saw off the closed world of Soviet communism and, by connecting China to the global economy, brought about the greatest poverty reduction in history.

A world of wall-builders would be poorer and more dangerous. If Europe splits into squabbling pieces and America retreats into an isolationist crouch, less benign powers will fill the vacuum. Mr Trump’s revelation that he might not defend America’s Baltic allies if they are menaced by Russia was unfathomably irresponsible (see article). America has sworn to treat an attack on any member of the NATO alliance as an attack on all. If Mr Trump can blithely dishonour a treaty, why would any ally trust America again? Without even being elected, he has emboldened the world’s troublemakers. Small wonder Vladimir Putin backs him. Even so, for Mr Trump to urge Russia to keep hacking Democrats’ e-mails is outrageous.

The wall-builders have already done great damage. Britain seems to be heading for a recession, thanks to the prospect of Brexit. The European Union is tottering: if France were to elect the nationalist Marine Le Pen as president next year and then follow Britain out of the door, the EU could collapse. Mr Trump has sucked confidence out of global institutions as his casinos suck cash out of punters’ pockets. With a prospective president of the world’s largest economy threatening to block new trade deals, scrap existing ones and stomp out of the World Trade Organisation if he doesn’t get his way, no firm that trades abroad can approach 2017 with equanimity.

In defence of openness

Countering the wall-builders will require stronger rhetoric, bolder policies and smarter tactics. First, the rhetoric. Defenders of the open world order need to make their case more forthrightly. They must remind voters why NATO matters for America, why the EU matters for Europe, how free trade and openness to foreigners enrich societies, and why fighting terrorism effectively demands co-operation. Too many friends of globalisation are retreating, mumbling about “responsible nationalism”. Only a handful of politicians—Justin Trudeau in Canada, Emmanuel Macron in France—are brave enough to stand up for openness. Those who believe in it must fight for it.

They must also acknowledge, however, where globalisation needs work. Trade creates many losers, and rapid immigration can disrupt communities. But the best way to address these problems is not to throw up barriers. It is to devise bold policies that preserve the benefits of openness while alleviating its side-effects. Let goods and investment flow freely, but strengthen the social safety-net to offer support and new opportunities for those whose jobs are destroyed. To manage immigration flows better, invest in public infrastructure, ensure that immigrants work and allow for rules that limit surges of people (just as global trade rules allow countries to limit surges in imports). But don’t equate managing globalisation with abandoning it.

As for tactics, the question for pro-open types, who are found on both sides of the traditional left-right party divide, is how to win. The best approach will differ by country. In the Netherlands and Sweden, centrist parties have banded together to keep out nationalists. A similar alliance defeated the National Front’s Jean-Marie Le Pen in the run-off for France’s presidency in 2002, and may be needed again to beat his daughter in 2017. Britain may yet need a new party of the centre.

In America, where most is at stake, the answer must come from within the existing party structure. Republicans who are serious about resisting the anti-globalists should hold their noses and support Mrs Clinton. And Mrs Clinton herself, now that she has won the nomination, must champion openness clearly, rather than equivocating. Her choice of Tim Kaine, a Spanish-speaking globalist, as her running-mate is a good sign. But the polls are worryingly close. The future of the liberal world order depends on whether she succeeds.

https://www.economist.com/news/leaders/21702750-farewell-left-versus-right-contest-matters-now-open-against-closed-new

Actually, the problem is “not enough energy to go around.” The only way countries can see to solve this is to put up barriers. “Let’s all continue the integration” involves sending more jobs abroad, and allowing more migrant workers in. It becomes an increasingly unpopular agenda.

We are not allowing “More” migrants in. We are allowing “Less” migrants in than ever before.

https://imgur.com/a/DB8Cq

I am saying that letting immigrants in, becomes an unpopular agenda. So I think we agree on this.

Give me a break. Justin Trudeau as brave? It doesn’t take any courage to give away other peoples resources and pat yourself on the back while importing voters for your party.

Brave men don’t cry

WHY A CRISIS IS GETTING NEARER

In The Arabian Nights, the heroine Scheherazade told one thousand and one tales. We, on the other hand, need only choose between two songs.

The first, cheerfully whistled by the consensus, is that the world economy is enjoying “synchronised growth”. We needn’t worry about debt and other measures of financial exposure, because a financial crash is very unlikely – and, even if it happened, the authorities would know what to do about it.

The alternative refrain is that most of the “growth” claimed by the authorities is cosmetic; that we really should worry about financial stress indicators; that a crash will happen, because it’s hard-wired into the system; and that plans for dealing with it probably won’t work.

Which of these is the true music – and which is off-key?

The aim here is to weigh the evidence, which comes in many shapes and sizes. The first conclusion is that the consensus view is a Pollyanna song (and Pollyanna, you might remember, found “something to be glad about in every situation, no matter how bleak it may be”). The optimistic consensus is every bit as complacent now as it was back in 2007, when growth was to be celebrated – and debt, we were told, didn’t matter.

The second conclusion is that the odds are shortening on a crisis happening a lot sooner than most people think – it could, indeed, happen latter this year.

Third, and from what we can surmise about them, the plans for responding to a crisis probably won’t work.

https://surplusenergyeconomics.wordpress.com/2018/04/18/122-a-tale-of-two-ditties/

From the above article, my favourite excerpt;

‘Second, governments are likely to assume public acquiescence in their rescue plans. But politics has changed fundamentally since 2008 – and any government which thinks it can sell another “rescue of the bankers” to the public is probably practising one of the worst types of complacency imaginable’.

But, in my experience, the sheople are way way too muddled up to understand the hand they have been dealt. The governor of the NZ reserve bank (I know, small fry) today spoke of bailing-in bank depositors in when the next crisis hits; but depositors don’t share the massive profits (withdrawals from the economy) these monopolies make in NZ. How about going after the assets of the owners of these business, as happens in other bankruptcies; the interviewer (National Radio – taxpayer funded) was too star struck/dumbed down to ask such a question.

We are sooooo f…..

Other than Tarp… which was spare change… and a token gesture ….. I do not recall the public being asked about the big time bail outs/stimulus plans (tens of trillions of dollars… and counting) ….

Tim has this wrong… the public will do and say nothing … in fact the public will not even be made aware of what the CBs are doing… most people have not a clue how much money as been thrown at this raging beast since 2008…. most probably have no idea what TARP is….

I am 100% certain that even those of us who are aware of the extreme policies of the CBs… are only seeing the tip of the ice berg….

Therefore there is no way that a revolt by the masses against bail outs etc… will take BAU down… they won’t be asked — they won’t be told….

Recall Jean Claude Junkman saying ‘when it gets serious you have to lie’

Well it is very serious…. it gets more dire by the day….

But… the centre continues to hold….

And in the comments by Tim Morgan;

‘At the same time, 2008 effectively marked the end of “capitalism”, because it took away the consequences of failure – and these, hitherto, had always legitimised the large rewards flowing from success.’

Banks have been protected for quite a while because of the need to protect depositors, or there will be a big problem–depositors without money can’t buy goods and services.

Remember the Savings and Loan Crisis earlier? https://en.wikipedia.org/wiki/Savings_and_loan_crisis

We keep going through new versions of the old problem.

‘ In fact, as shown below, starting in 2009 the cumulative amount of new federal debt surpassed the cumulative amount of GDP growth going back to 1967…. Said differently, if it were not for a significant and consistent federal deficit, GDP would have been negative every year since the 2008 financial crisis. ‘

https://www.zerohedge.com/news/2018-04-18/triffin-warned-us

Iran switches from dollar to euro for official reporting currency

https://www.reuters.com/article/us-iran-currency-euro/iran-switches-from-dollar-to-euro-for-official-reporting-currency-idUSKBN1HP25W

Iran just dumped the dollar! The elders won’t be happy about this!

Goodbye, Iran. You gave it a solid try.

https://www.godlikeproductions.com/sm/c3549d16.gif

Saudi Arabia might not be able to afford its multibillion dollar mega-projects

http://www.businessinsider.com/saudi-arabia-may-not-be-able-to-afford-multibillion-dollar-projects-2018-4

I would very much agree: Saudi Arabia may not be able to afford all of its multi-billion dollar projects.

We recently saw the article, https://www.washingtonpost.com/news/energy-environment/wp/2018/03/28/why-saudi-arabia-is-trying-to-pull-off-an-utterly-massive-new-solar-project/?noredirect=on&utm_term=.eb46ccd725fc

Why Saudi Arabia is trying to launch an utterly massive solar project.

The plan seems to be scale todays two projects up to 200 gigawatts by 2030. I will believe that when I see it.

Amongst the top 100 papers in the US by circulation, not a single editorial board opposed Trump’s airstrikes on Syria

https://fair.org/home/out-of-20-major-editorials-on-trumps-syria-strikes-zero-opposed/

This will make you laugh Gail…

One of the ways self-organization works is by people trying to conform to the expectations of others. It works in much the same way that the atoms in a magnet line up in a particular way, if magnetism is involved.

Somewhere I must have missed out on the conformity gene.

those 100 top papers are owned/controlled by 15 men. They are part of the group who are your masters.

https://www.forbes.com/sites/katevinton/2016/06/01/these-15-billionaires-own-americas-news-media-companies/#7ae38276660a

http://www.businessinsider.com/these-6-corporations-control-90-of-the-media-in-america-2012-6

https://twitter.com/MuradGazdiev/status/986666029446324224

IMF issues warning on global debt

http://www.bbc.com/news/business-43809872

U.S. Pension Fund Collapse Isn’t a Distant Prospect. It Could Come in 5 Years

https://www.bloomberg.com/view/articles/2018-04-18/collapse-of-public-pension-funds-is-no-longer-a-distant-prospect

The article talks about the possibility of pension “reform.” The problem is really that pensions were set up assuming that the economy would be growing much more quickly than it really is. There is no way that they can make up for wrong assumptions that are getting worse, year after year.

How economic inequality is killing us

https://www.marketwatch.com/story/how-economic-inequality-is-killing-us-2018-04-18?link=sfmw_tw

Charles Hugh Smith’s blog is featured here.

Here’s how hackers could cause chaos in this year’s US midterm elections

https://www.technologyreview.com/s/610774/heres-how-hackers-could-cause-chaos-in-this-years-us-midterm-election/

IMF sounds alarm on excessive global borrowing

The world’s $164tn debt pile is bigger than at the height of the financial crisis a decade ago, the IMF has warned, sounding the alarm on excessive global borrowing.

The fund said the private and public sectors urgently needed to cut debt levels to improve the resilience of the global economy and provide greater firefighting capability if things went wrong.

“Fiscal stimulus to support demand is no longer the priority,” the IMF said on Wednesday in a report published at its spring meetings in Washington.

Vitor Gaspar, director of fiscal affairs at the IMF, singled out the US for criticism, saying it was the only advanced country that was not planning to reduce its debt pile with tax cuts keeping public borrowing high.

The fund urged policymakers to stop providing “unnecessary stimulus when economic activity is already pacing up” and called on the US to “recalibrate” its fiscal policy and increase taxes to start cutting its debt.

Worldwide borrowing is more than twice the size of the value of goods and services produced every year and at 225 per cent of global gross domestic product, is 12 percentage points higher than during the peak of the previous financial crisis in 2009.

Half of the $164tn was accounted for by three countries: the US, Japan and China. The latter’s borrowing surged from $1.7tn in 2001 to $25.5tn in 2016, accounting for three-quarters of the increase in private sector debt in the past decade.

The fund was concerned that “an abrupt deleveraging process” in the private sector could trigger another financial crisis as borrowers tightened their belts simultaneously.

“In the event of a financial crisis, a weak fiscal position increases the depth and duration of the ensuing recession, as the ability to conduct counter-cyclical fiscal policy is significantly curtailed,” the fund said.

With the global economy expanding strongly, it recommended that countries such as the US stop using lower taxes or higher public spending to stimulate growth and instead try to reduce the burden of public sector debts so that countries have more leeway to act in the next recession.

“In the United States . . . fiscal policy should be recalibrated to ensure that the government debt-to-GDP ratio declines over the medium term. This should be achieved by mobilising higher revenues and gradually curbing public spending dynamics, while shifting its composition toward much-needed infrastructure investment.”

There is no sign that the Trump administration has any intention of increasing taxes as the IMF recommends and, instead, hopes that faster growth will supply the necessary revenues, something the fund and the US fiscal watchdog thinks is highly unlikely.

The debt problem is not limited to advanced economies: middle-income countries are also racking up borrowing at a higher level than they did during the debt crises of the 1980s.

The outliers were Germany and the Netherlands, which the IMF said had “ample fiscal space” to boost public investment in infrastructure and enhance the long-term resilience of their economies.

https://www.ft.com/content/d4bf2984-42d2-11e8-93cf-67ac3a6482fd

Econ 101 No Longer Explains the Job Market

https://www.bloomberg.com/view/articles/2018-04-05/supply-and-demand-does-a-poor-job-of-explaining-depressed-wages

Argentina Falls Into a Pit of Poverty, Hunger

BUENOS AIRES — Argentines, who lived as well as the Italians and the French a few decades ago, face a staggering prospect: The minimum wage by the end of June could be worth $10 a month–less than that of Haiti, the world’s poorest country.

One of the world’s great granaries and beef producers is now coping with the unprecedented reality of hunger. The posh downtown bistros are still crowded, but the decaying industrial belt around the capital has slid into depression.

In May, the hardships and disparities became insupportable. Rioters destroyed hundreds of stores in an explosion of looting that left 15 dead, the first such unrest in Argentine history.

Argentines long have sought to find the causes of their protracted decline, hoping that, in the process, they might discover the road back to prosperity. All sectors seem closer than ever to a consensus on the diagnosis: equally greedy siphoning by the state itself, business and labor, that finally coalesced into a hypercrisis in a country accustomed to crises.

Inflation used to be expressed in annual terms, then monthly and even weekly. Now people think of a daily inflation rate: Prices were climbing in early June by 3% a day. In 1985, one Argentine austral was worth $1.20; by the middle of this month, a dollar was buying nearly 400 australs. The biggest bill, until recently, was 100 australs. This month, the mint began printing 50,000-austral notes.

The powerful trade unions, which staged 13 general strikes for better wages and benefits in the past five years, now are reduced to asking employers to give advance notice of layoffs and to rotate suspensions among the staff.

The food riots underscored President Raul Alfonsin’s brinksmanship as he struggled to serve out his term. The government imposed a 30-day state of siege and rounded up 2,000 people in containing the violence. Aware that none of the basic causes has been addressed, few analysts are confident that the trouble will not recur.

The sense of desperation has never been more profound.

In San Miguel, an industrial suburb 20 miles northwest of the capital, three young men and a woman stood chatting a block from the site of some of the worst rioting the previous day. Their stories suggested the impact of the hyperinflationary implosion and the dangers ahead for Argentina.

One youth had been laid off by an air-conditioning firm two weeks before. Suppliers could not quote prices and refused credit, so the business closed. Another, laid off from construction, said: “Cement went from 80 australs a bag to 400 in two months. Who can build anything?”

Salaries Plummet

The woman, Maria Lopez, 46, said she had been dismissed two months earlier by a video machine assembler and was given 10,000 australs, then worth about $100, as severance pay after 14 years’ work. She survives with her husband on his 4,000-austral ($20) salary as a security guard. Waving toward the looted shops and the cordon of helmeted police along the avenue, she said, “We are not subversives. We are hungry and have no work.”

They are some of the victims of a graphic decline. Illustrations of the problems abound:

– Real salaries are at one-half to one-third of their level when Alfonsin took office in 1983.

– Retail prices rose 78.5% in May alone, and wholesale prices surged 104%.

– Suppliers who used to give customers 30 to 45 days to pay, now want cash on delivery, and credit is virtually unavailable.

Cesar Suraski, a downtown furniture store owner with his own factory in the suburbs, said his sales are 10% to 15% of the level they were two months ago, barely covering his store rent. With inflation approaching 100% a month, he can no longer sell on the installment plan or by credit card. He plans to close his store July 1–and his factory two months later–if things do not improve.

http://articles.latimes.com/1989-06-18/business/fi-3652_1_australs-argentines-riots

18 June 1989?

IMF Warns of Rising Threats to Global Financial System

https://www.bloomberg.com/news/articles/2018-04-18/rising-risk-appetite-recalls-pre-crisis-exuberance-imf-warns

Shocking images of VW cars dumped in Californian desert by German manufacturer after it was forced to buy back 350,000 cars for $7billion over diesel scandal

http://www.dailymail.co.uk/news/article-5562609/Shocking-images-VW-cars-dumped-Californian-desert.html#ixzz5D3WT1Ida

Lessons From The Last Time Civilization Collapsed

https://www.npr.org/sections/13.7/2014/08/19/341573332/lessons-from-the-last-time-civilization-collapsed

Comparing apples to bamboo….

This time is different.

There have been many collapses since then.

Bed Bath & Beyond is in serious trouble

http://money.cnn.com/2018/04/18/investing/bed-bath-beyond-standard-poors-downgrade/index.html

Is the U.S. Shale Boom Choking on Growth?

Permian basin, America’s fastest-growing oil field, is hitting its limits

The oil field at the heart of the U.S. shale boom is hitting the limits of its growth faster than anticipated, a surprise with big ramifications for energy profits and global markets.

The Permian basin of West Texas and New Mexico has been one of the few growth engines for oil production world-wide. The region’s output is on track to single-handedly rival that of Iran or Iraq and has lifted American production to all-time highs. Output is projected to climb from 3 million barrels a day to more than 4 million barrels a day within two years. The International Energy Agency forecasts that production will double by 2023.

But Permian producers are starting to encounter congested pipelines and shortages of materials and workers—bottlenecks that have caused some investors to sour on the region. Some energy executives question whether sky-high forecasts for the field are achievable.

While production is expected to continue rising, the Permian’s stumbles could ripple out to the global oil market at a time when OPEC has curtailed output and many companies have cut back on megaprojects. That could become a source of volatility that propels oil prices elsewhere higher, just as the market is recovering from a world-wide collapse in energy prices in 2014.

“It makes sense that the basin with the lowest costs, seeing the biggest increase in growth would also see the most bottlenecks and the most challenges to that growth,” said John Dowd, manager of the Fidelity Select Energy Portfolio. “At the end of the day, it’s not physically easy to grow production 1 million barrels a day in the U.S.”

After crude prices fell from more than $100 a barrel in 2014 to less than $30 two years later, companies in many areas shut down rigs and cut spending.

But in the Permian basin, production never stopped. As oil prices have climbed, the pace of work in the region has become frenetic, with production rising by about 800,000 barrels a day in the past year. Pipeline capacity is emerging as a problem. Oil is starting to back up in West Texas and has recently sold at a $6 to $9 discount to crude prices elsewhere in the U.S. That is a warning sign that some oil might have to travel by more expensive ways like trucks to market and that producers could be forced to take drastic measures like halt drilling.

The natural gas gushing from wells also threatens to overwhelm pipelines. Some producers face the prospect of shutting wells.

“We are beginning to hear that shut-ins are becoming a very real nightmare for some producers,” John Zanner, an analyst at RBN Energy LLC, wrote in a recent note.

A number of major Permian operators reduced their output forecasts last year, often citing weather-related issues—claims that have led some industry executives to believe the bottlenecks could be more severe than some companies have acknowledged.

Permian operators are likely to see their costs rise up to 15% in the area, an issue that could affect profit margins even as oil prices rise. Investors will be watching the pace of output as companies report earnings in coming weeks. Several seasoned U.S. oil executives have begun to extol the prospects of other areas. Steve Chazen, the former chief executive of Occidental Petroleum Corp. , the biggest producer in the Permian basin, built Magnolia Oil and Gas, a company that drills in South Texas.

“When you get to a certain size, growing at 25% every year becomes a mathematical impossibility,” Mr. Chazen said in an interview. “I think we’re close to where the growth rate is going to decline.” Many analysts expect prices in the region could tumble further before new pipelines arrive in 2019.

Labor and supply scarcity are adding to the challenges. Operators are scrambling to acquire the sand and water needed for enormous fracking jobs.

About 87% of the supplies and equipment needed for fracking jobs in the Permian are in use, and producers are likely to reach full capacity within months, said Matt Johnson, a principal at Primary Vision Inc., a firm that tracks crews, sand, water and other services needed for drilling across the U.S.

Chris Cuyler, vice president of exploration and geoscience at Elevation Resources LLC, a private oil and gas producer, said his small firm has to schedule fracking crews at least a month in advance—compared with two or three weeks a year ago.

Companies are bringing workers from out of town. John Volke owns companies that find housing for oil-field workers and owns trailer parks known as “man-camps.” Hotel rates have spiked as high as $600 a night. Mr. Volke has already ordered 30 new trailers and will likely have to order another 30.

The constraints threaten the profitability of the industry just as investors are expecting a payout due to rising crude prices, taking some of the shine off Permian producers, which were Wall Street darlings in recent years.

The shares in a group of 15 such companies, including Pioneer Natural Resources Co. and Concho Resources Inc., CXO +1.58% have fallen by an average of less than 1% this year. A broad index of U.S. producers has risen 1.3% in that time. In 2016, the Permian group rose by more than 60%, almost double the increase to a broad subset of U.S. operators.

The Permian’s growth rate is expected to account for “half of what’s supposed to happen in the whole planet,” said John Groton, director of equity research at Thrivent Asset Management. “If that’s compromised it’s a big deal.”

Write to Alison Sider at alison.sider@wsj.com and Bradley Olson at Bradley.Olson@wsj.com

https://www.wsj.com/articles/is-the-u-s-shale-boom-choking-on-growth-1524056400

WTF? Donald Trump has weird pre-dawn Twitter meltdown

In the span of 280 characters, Trump attacked the Governor of California, accused the state of having launched a civil war against the United States, hurled a bunch of racist accusations at Mexican immigrants, and used a term that doesn’t appear to exist. Here’s what he tweeted: “There is a Revolution going on in California. Soooo many Sanctuary areas want OUT of this ridiculous, crime infested & breeding concept. Jerry Brown is trying to back out of the National Guard at the Border, but the people of the State are not happy. Want Security & Safety NOW!”

Wait, what the hell is a breeding concept?

No one who replied to Trump’s tweet could seem to figure out what the phrase was supposed to mean. One respondent tweeted “Breeding Concept?? What are you even talking about?” Another replied with “That’s what I’m wondering,” and yet another with “I’d like to know too.” Was Trump trying to accuse immigrants of coming to sanctuary cities to “breed” by having children?

https://twitter.com/realDonaldTrump/status/986544648477868032

“Wait, what the hell is a breeding concept?”

Breeding = Proliferating (probably)

Oh come on. He obviously meant that this situation is “breeding contempt.” Which is exactly what illegal immigration is doing – i.e. people are contemptuous of freeloaders.

“Here are the facts: there is no massive wave of migrants pouring into California. Overall immigrant apprehensions on the border last year were as low as they’ve been in nearly 50 years (and 85 percent of the apprehensions occurred outside of California).”

http://www.politifact.com/california/statements/2018/apr/13/jerry-brown/jerry-brown-says-theres-no-massive-wave-migrants-p/

Trump has serious paranoia and mental illness…He is going to end like Kusnher’s father, in a prison cell..

Entertainment.

World trade system in danger of being torn apart, warns IMF

https://www.theguardian.com/business/2018/apr/17/world-trade-system-imf-trump-tariff-china-us-world-economic-outlook

Christine Lagarde: “clutches pearls”

bingo!

IMF Spots Trouble Ahead for the Global Economy After 2020

https://www.bloomberg.com/news/articles/2018-04-17/imf-spots-trouble-ahead-as-solid-global-growth-poised-to-slow-jg3oe4z8

42% of Americans are at risk of retiring broke

https://www.cnbc.com/2018/03/06/42-percent-of-americans-are-at-risk-of-retiring-broke.html

Actually, 100%, but CNBC doesn’t know this.

bingo!

Princeton Study: Boosting employment rate is unlikely to curb opioid use

https://www.sciencedaily.com/releases/2018/04/180417155621.htm

Give me a break.

They need a different way to deal with pain.

Opioids of the Masses

https://www.foreignaffairs.com/articles/world/2018-04-16/opioids-masses

CBO’s Economic Forecast (GDP) for the 2018–2028 Period (1.9%)

https://www.cbo.gov/publication/53764

But faster at first, I see.

Famed War Reporter Dr Robert Fisk Reaches Syrian ‘Chemical Attack’ Site, Concludes “They Were Not Gassed”

https://www.independent.co.uk/voices/syria-chemical-attack-gas-douma-robert-fisk-ghouta-damascus-a8307726.html

http://stmedia.startribune.com/images/ows_152184671217675.jpg

The National Debt Is Worse Than You Think

Today’s outlook for revenue growth is based on policy that’s unlikely to pan out.

I know that worrying about the deficit and debt is hopelessly retro, but please indulge me for a few minutes.

Last week the Congressional Budget Office issued its outlook for the next 10 years. The news was not good. Over the next decade, the annual federal deficit averages $1.2 trillion. It rises from 3.5% of gross domestic product in 2017 to 5.1% in 2027. The national debt, which is driven by annual deficits, rises from $15.7 trillion to $28.7 trillion over the same period, and surges from 78.0% to 96.2% as a share of GDP—the highest mark since just after World War II.

These projections have worsened significantly since the CBO’s report last June, and public-policy decisions are the culprit. The 2017 tax law reduced projected federal revenue by $1.7 trillion over the next decade, while the recent appropriations bill increased spending by $1 trillion.

And if this outlook weren’t bad enough, the real story will probably be worse. The CBO is legally required to make its estimates on the basis of current law, but the federal government is likely to end up spending more and taxing less than the law specifies.

Here’s why: To make the numbers add up, the tax law specifies that most individual tax breaks will disappear after 2025. But neither political party is likely to let this happen, at least for low- and middle-income taxpayers.

In a similar vein, the appropriations bill assumes defense and domestic spending will decline after the current two-year agreement ends. But Republican defense hawks and Democratic defenders of social programs will work hard to prevent this from happening.

The CBO estimates that if current policy continues—rather than current law—the cumulative deficit will rise a further $2.6 trillion over the next decade, to a staggering $15 trillion. This would push the national debt to 105% of GDP, a level exceeded only once in our history.

Supply-siders may object that these estimates don’t account for projected economic growth from the tax cuts. In fact, they do. The CBO projects that the tax law will increase real GDP by an average of 0.7% and employment by an average of 1.1 million jobs each year over the next decade. These economic gains will reduce the reform’s net cost by 22% during this period, meaning the bill doesn’t come close to paying for itself even with dynamic scoring.

The picture would be much brighter if the tax reform boosted growth to the Trump administration’s target of 3%, but the CBO doesn’t expect this to happen. In the short term, it estimates that growth will surge to 3.3% in 2018 and a respectable 2.4% in 2019. In 2020, however, growth is expected to subside to just 1.8% with no significant rise thereafter. Average growth in the coming decade is projected at a mere 1.9% per year.

The reason for the slowdown is straightforward. Economic growth reflects two key variables: the total number of hours worked and output per hour, known as productivity. Over the next decade the CBO expects annual productivity increases to average 1.4%, a dramatic improvement over the dismal 0.9% of the previous decade. But the labor force, which grew 2% annually as recently as the 1990s, is expected to increase by only 0.5% per year over the next decade. The aging of the population will exert steady downward pressure on labor-force participation during this period while increasing the pool of retirees by one-third.

Several measures could produce marginal improvements in labor-force participation. We could stem the flow of women leaving the U.S. workforce by investing in the type of pro-work and pro-family programs that European countries have implemented in the past decade. We could do much more to reintegrate felons into the workforce.

We could also make bigger gains if we were prepared to increase the number of working-age immigrants entering the U.S. This would require both reducing the number of slots dedicated to family reunification, which most Democrats oppose, and increasing the total number of immigrants, the reverse of the Trump administration’s position.

Absent big changes in the labor force, advocates of 3% growth are left hoping for a productivity miracle. Economists aren’t sure what makes productivity wax and wane, meaning a return to the 2% annual productivity gains of the 1990s can’t be ruled out. But even this surge would leave us well short of the 3% target.

It would be more realistic to accept that in our aging society, the economy will expand more slowly while retirement spending expands more quickly. Congress should adopt a fiscal policy consistent with these realities. Academic economists can make improbable assumptions, but policy makers don’t have that luxury.

https://www.wsj.com/articles/the-national-debt-is-worse-than-you-think-1524004495

The truth is that the national debt is a lot worse than you think. The forecast assumes better than a “best possible case.”

Haynes and Boone has tracked 144 N. American oil and gas companies that have filed for bankruptcy since the beginning of 2015. These bankruptcies, including Chapter 7, Chapter 11, Chapter 15, and Canadian cases, involve approximately $90.2 billion in cumulative secured and unsecured debt. One hundred and twenty six of the cases were filed in the United States. As of March 31, 2018, six producers have filed for bankruptcy in 2018, representing $7.5 billion in cumulative secured and unsecured debt.

http://www.haynesboone.com/publications/energy-bankruptcy-monitors-and-surveys

Could the Fed Set Off a Debt Bomb?

Tighter monetary conditions will squeeze borrowers.

The U.S. Federal Reserve minutes released Wednesday show that central bank officials are increasingly committed to raising rates and shrinking the bank’s balance sheet. While economic signs remain mixed, continued growth, rising inflationary expectations, tightening labor markets and the need to temper asset prices would all seem to argue in favor of higher rates.

Other central banks are likely to follow. The Bank of England and the European Central Bank have foreshadowed normalization of interest rates. The ECB seems likely to scale back its bond purchases. Markets are now factoring in multiple U.S. interest rate rises in 2018. The yield on the 10-year U.S. Treasury note has risen from 2.4 percent to 2.8 percent in 2018 alone.

Rising rates seem like a valedictory return to “normality” — a marker of how successful the central banks’ heroic actions to counter the Great Recession were. What the celebration misses, though, is how swelling levels of debt will amplify the effect of any rate rises.

According to the Institute of International Finance, global debt reached a record $237 trillion in 2017 — more than 327 percent of global GDP. Since 2007, when borrowing levels were a key factor in the financial crisis, debt has increased by $68 trillion, or more than 50 percent of global GDP.

In developed markets, the ratio of debt-to-GDP is around 380 percent. In emerging markets, the ratio is above 200 percent. While the rate of growth has slowed, this is only because of higher GDP growth — driven, in part, by increased borrowing. A decade of unprecedently low global rates and abundant liquidity appears to have encouraged a spree of public and private debt accumulation.

If the current calm is an argument for raising interest rates, those higher rates may in turn be more destabilizing than many anticipate. This will be especially true if U.S. rate hikes flow through into other markets, as they did during the 2013 “taper tantrum.”

For one thing, higher interest rates will exacerbate the risk of financial distress for highly indebted corporate and sovereign borrowers. This will particularly affect illiquid, riskier corporate and high-yield bonds, which have attracted significant attention as investors have sought out yield in the prevailing low-return environment.

Losses will flow into the banking sector. Since the start of 2018, the LIBOR–overnight index swap spread — a metric of bank credit risk — has increased from around 0.2 percent to 0.6 percent. The increase reflects, in part, a risk premium for the uncertain effects of U.S. monetary policy, increasing bank credit risk and rising demand for funds to guard against anticipated market stress.

Second, higher rates will generate large mark-to-market losses on existing debt holdings. The loss from a 1 percent increase in U.S. government bond interest rates would exceed $2 trillion globally. Losses on corporate and other securities would add to the damage. Holders may be forced to raise capital or liquidate, compounding the pressure on rates. For banks, such losses could constrain their capacity to supply credit.

Third, higher interest rates will drive investors to switch from stocks and other risky assets to bonds. Lower stock prices may affect the collateral value securing financings. The debt-funded share buybacks and acquisitions that have propped up equity prices will slow down.

Fourth, higher rates will divert cash to servicing debt. This will dampen economic activity, as companies reduce their investments in the real economy and households, burdened by record levels of borrowing in several countries, cut back on their purchases.

Finally, and perhaps most importantly, higher rates will restrict the ability of governments to deploy fiscal stimulus to extend and solidify the recovery. The U.S. is headed for trillion-dollar annual budget deficits from 2020, driven by tax cuts and higher public spending. Higher rates and rising deficits will sharply increase the amount needed for debt service as a percentage of expenditure. According to the Congressional Budget Office, net interest payments would rise to 3.1 percent of GDP in 2028, up from 1.6 percent in 2018. The problem will be compounded if growth slows because of higher rates, as well as other factors such as trade disputes and geopolitical stresses.

The idea that higher interest rates don’t matter because they will simply reallocate cash between borrowers and lenders is misleading. It assumes that the easy money of the past decade was spent productively and is generating the earnings required to service the borrowing. In fact, to a substantial degree, borrowings simply financed consumption and leveraged purchases of existing assets rather than new investment. At higher interest rates, many borrowers won’t be able to service the debt they’ve incurred. The Fed and others had better be prepared for a return to “normal” that’s anything but.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners. To contact the author of this story: Satyajit Das at sdassydney@gmail.com

https://www.bloomberg.com/view/articles/2018-04-12/u-s-federal-reserve-rate-hikes-could-trigger-a-debt-bomb

” The yield on the 10-year U.S. Treasury note has risen from 2.4 percent to 2.8 percent in 2018 alone.”

true, but a bit misleading…

this year, the rate went up to about 2.95% before being hit with a “whack-a-mole” tactic which knocked it down into the 2.7s…

the rate is now 2.84…

because of all the problems that might arise (as the article says), this rate won’t be allowed to go much higher…

the Fed will have to be losing its grip on controlling the economy for it to go over 3%…

hey, maybe by June 1st…

Right. It is short term interest rates that are up, no 10-year Treasuries. They affect mortgage rates, and are more set by the market.

I hadn’t thought about calling higher rates a “Debt Bomb,” but it sounds like a pretty good description of the situation to me.

False flags are real – US has a long history of lying to start wars

https://www.rt.com/op-ed/424298-false-flag-syria-attack/

This is from RT (a Russian publication). How certain are we that they would be telling the truth?

https://cdni.rt.com/files/2018.04/article/5ad4c36ddda4c812778b4586.jpg

I have never read ‘Alice in Wonderland’, but maybe now is the time.

The ‘Truthmakers’ seem to need to be running faster and faster just to stand still. Or is there a better fantasy novel (Not “Game Of Thrones”) that I should make my bedtime reading to prepare for each new day?

“If you want a guarantee, buy a toaster” – “The Rookie” – 1990

You may be asking the wrong question. When news breaks in a situation close to war, the protagonists quickly learn never to leave a news vacuum. Think of it as a news trajectory, with two diametrically opposed views, converging, possibly very slowly.

Of immediate concern to me is the monopoly of power. If a vote had to be taken before punitve kinetic action was authorised, questions about “intelligence” would be asked, and evidence may have to be produced. Afterwards, lies are much more difficult.

I’m adding this from a non-Russian publisher, for perspective, it’s a year old;

https://www.welt.de/politik/ausland/article165905578/Trump-s-Red-Line.html

Economic Consequences Of Peak Oil For The Major Multinational Oil And Gas Companies (Amate 2018)

https://www.scribd.com/document/376611398/Economic-Consequences-Of-Peak-Oil-For-The-Major-Multinational-Oil-And-Gas-Companies-Amate-2018

Abstract:

So companies need to “relax their investments” during periods of low prices. This makes supplies drop further. This is really what causes peak oil (and peak other things). Steve Kopits was writing about the issue of too low return in invested capital in the 2013 timeframe, back before oil prices drop.

If return on investment is truly too low, this will continue to be a problem, whether a company makes the investment now or 10 years from now. What the economy needs is cheap to produce oil. If it is not cheap to produce now, it will not be cheap-to-produce later. It is low cost per barrel or Btu that really matters.

Why Trillion-Dollar Deficits Matter

http://www.thefiscaltimes.com/2018/04/12/Why-Trillion-Dollar-Deficits-Matter

US consumer finances hit by higher fuel prices -Financial Times

American households expected to spend on average $400 more this year on petrol

Ed Crooks in New York 8 HOURS AGO Print this page1 Tim Rogus, a retired publisher in suburban Chicago, has noticed fuel prices at the petrol station creeping up towards $3 a gallon, as oil has rebounded to four-year highs this month, but he is philosophical about it. “Our prices were nearly $4 at one point,” he says. “Life has to go on somehow.”

His attitude sums up the expected impact on US consumers of rising oil prices: not a disaster, but another burden to bear, with rural areas and middle-income households hit the hardest.

Americans are expected to spend an average of $400 per household more on fuel this year than in 2016, as the rebound in crude prices is reflected in the cost of petrol at the pump. By contrast, middle-income US households will on average gain $930 each from the tax cut bill passed at the end of last year, according to the Urban-Brookings Tax Policy Center.

The average price of petrol in the US was about $2.75 a gallon last week, according to the government’s Energy Information Administration, up $1 from its low point of about $1.75 in February 2016.

The “driving season”, the peak of petrol consumption in the US, is April to September, and the EIA expects prices this summer to be at their highest for four years, up 10 per cent from 2017.

Oil has been pushed higher by the success of Opec’s strategy of restricting output, and international risks including Saudi Arabia’s war with Houthi rebels in Yemen, and tension between the US and Russia over Syria.

A decade ago, before the shale oil boom, prices at these levels would have loomed large for US policymakers. The surge in US production, which has cut net imports sharply, has calmed those fears.

“Ten years ago, White House economists looking at gross domestic product and job creation would be quite concerned if oil prices rose significantly,” says Jason Bordoff, a former official in the Obama administration who leads the Center on Global Energy Policy at Columbia University. “It’s a different world now.”

When oil prices fell sharply after the summer of 2014, the net stimulus to the US economy was “effectively zero”, wrote economists Christiane Baumeister and Lutz Kilian in a Brookings paper in 2016. The boost to consumers from cheaper fuel was cancelled out by a slump in investment in the oil industry. As oil prices rebound, the overall impact on US growth is similarly likely to be very small, Mr Kilian says.

But while growth may not be much different overall, its composition will be affected, with an investment boom in the oil industry offset by a drag on consumer spending.

Cheaper oil handed a windfall to middle-income households, more than half of which was spent, according to research from the JPMorgan Chase Institute. Now, some of that boost is being withdrawn.

The impact varies widely across different types of consumers. Rural households spent about 16 per cent more on petrol on average than urban households in 2016. Fuel accounted for 4 per cent of total household spending for middle-income Americans, but only 2.6 per cent for the highest earning fifth.

There are already signs that higher fuel costs may be starting to have an effect. US retail sales excluding fuel, food and cars have been roughly flat since November, data from the commerce department showed on Monday.

In effect, the boom in the hotspots of the oil industry such as west Texas, where truck drivers are being hired for $100,000 per year, is being paid for by consumers.

One effect not yet seen from higher fuel prices is a drop-off in demand. Petrol consumption is likely to be slightly higher this summer than it was last year, the EIA has forecast.

“People aren’t going to start cancelling trips with gasoline at $2.75, and probably not at $2.95,” says Tom Kloza, head of research at Oil Price Information Service.

“If the economy keeps chugging along, you’ll have to see more than 25 cents more on the price before you see a significant demand response.”

Additional reporting by Patti Waldmeir in Chicago

https://www.ft.com/content/59019f1a-41cf-11e8-803a-295c97e6fd0b

Changes can be subtle and occur at the margin. Subprime auto loan holders may have a higher default rate, for example. China may export more petroleum products like diesel, if they cannot use them at the higher price.

Watched this on the plane https://en.wikipedia.org/wiki/Hard_Sun

In a nutshell… the government knows an extinction event is imminent — a leaked file gets into the hands of a cop who attempts to expose what is happening — she hands it to the press — it gets air time – then a massive campaign is launched to discredit the whole thing as a conspiracy theory…

UK intelligence is directly involved in trying to stop the story from getting out because – as they put it — the world would unravel if the masses became aware….

Lots of the themes that are discussed on FW are raised in this series — it’s almost as if the writers were following FW when they put this together

Definitely worth watching