If a person reads US newspapers, it is easy to get the impression that all of the world’s oil problems are over. But this is not really the case.

An Overlooked Part of the Problem: High Oil Prices

A major piece of the world’s oil problem is high price. Prices continue to be far above historic levels, now in 2013.

Figure 1. World oil price (Brent equivalent) in 2011$, based on BP 2013 Statistical Review of World Energy data.

High oil prices disrupt economies around the world because when oil prices rise, the wages of the vast majority of workers do not rise to compensate. Workers find that they need to adjust their spending patterns because the higher price of oil leads to higher prices for many things, including the cost of commuting, the cost of food, and the cost of buying goods that have been shipped long distance.

When workers adjust their spending patterns, discretionary spending is cut. This leads to patterns we associate with recession, or perhaps just slow growth. Unemployment rises, and there is less demand for new homes and cars.

Governments are also affected, because many of their costs, such as building roads, are higher. They also have to pay benefits to workers who can’t find jobs, or who can only find only low-paying jobs. Governments find it increasingly difficult to collect enough taxes because of the low wages of workers. Problems with rising deficits and the debt ceiling become the order of the day. Does any of this sound familiar?

One of our biggest issues today is that we don’t have a way of getting oil prices back down again, without a drop in oil extraction. The “easy to extract” oil (and thus the inexpensive-to-extract oil) was extracted first. There is still a huge amount of oil in the ground. The issue is that we can’t get it out, except at high prices—the same high prices that either (a) cause recession, or if governments can disguise the problem with deficit spending and low interest rates, (b) cause persistently low employment plus slow growth.

The Recent Rise in US Crude Oil Production

It is true that United States oil production is now higher than it has been in the recent past. The rise in production relates primarily to “tight oil”—the kind of oil production that is enabled by very extensive hydraulic fracturing (also called fracking). (Figure 2)

Figure 2. US crude oil production, divided into “tight oil”, oil from Alaska, and all other, based on EIA data.

We are often told that this rise in production is because of the invention of fracking. This is not really true; fracking has been used for decades, but not in the quantity it is used today. Oil production is up because oil prices continue to be high. High oil prices allow producers to use fracking in the quantity it is used today, on sites that without the technique would not be able to produce oil. Even with recent improvements in techniques, fracking remains expensive. Continued extraction of tight oil depends on oil prices remaining high.

There are other things besides high oil price that enable tight oil production. One of these things is plenty of credit, available at low interest rates. Tight oil by its nature requires considerable up front investment. Cash flow tends to be negative as production is ramped up. This means that there is a need for a lot of debt financing, so low rates are helpful. Ultra low interest rates, such as those provided by quantitative easing, also enable equity (stock) financing, because investors are so starved for reasonable returns that they will buy stocks of iffy companies, in the hope of capital gains.

Another thing that enables tight oil extraction in the United States is our law structure. In the United States, property laws permit landowners to share in the profits from oil drilling. In most other countries, profits are split between the company and the government, with nothing for local property owners. Because of the financial incentive, US property owners are often willing to put up with the hassles of hydraulic fracturing. This isn’t necessarily true elsewhere.

The United States also has other advantages that are not available in much of the world: lots of pipelines already in place, many drilling rigs available, a reasonable level of water supply, and population which is not terribly dense, so that fracking can often be done away from populated areas. The spread of technology for doing fracking around the world is far from a slam-dunk, because of the many obstacles to extraction elsewhere. These can at times be overcome with different techniques, but this adds another layer of costs, meaning oil prices need to be higher yet.

The amount by which tight oil production will continue to rise is open to a variety of interpretations. If oil prices drop because of recession, there may be very little additional production. If credit availability dries up, tight oil production may drop. If everything goes well, US production may rise. If miracles happen, tight oil production may even rise in many areas around the world.

As I have indicated previously, I am concerned about a financial discontinuity in the very near future–a few months to a year or two–a discontinuity that is ultimately related to high oil prices. This financial discontinuity could even be related to the current government shutdown, if it goes on for an extended period. If we are reaching a discontinuity, credit markets may be so disrupted and other changes may be so significant that past projections will be irrelevant.

A Second Overlooked Part of the Problem: Inadequate Rise in World Oil Production

The second major issue we are encountering now, besides high oil price, is an inadequate rise in world oil production. Many people are concerned about a possible unplanned decrease in world oil supply (so-called “peak oil”). While this may happen, worrying about this issue misses an important issue that comes earlier: for a growing world economy, we really need a reasonably large annual increase in oil supply.

Even if we include all kinds of liquids that aren’t quite oil, such as ethanol, natural gas liquids, and coal-to-liquid, the growth of oil supply has tapered off considerably in the last 50 years. (Figure 3).

Figure 3. Growth in world oil supply, with fitted trend lines, based on BP 2013 Statistical Review of World Energy.

If we fit trend lines to historical oil production, we see that the lines become progressively flatter. To make matters worse, the number of potential customers for this oil has been rising, thanks to globalization. The World Trade Organization was formed in 1995. Adding China to the World Trade Organization in December 2001 particularly ramped up demand for all types of energy products, including oil. As China’s use of oil products soared, it put huge pressure on world oil prices. The combination of flat production and rapidly rising demand led to rapidly rising oil prices between 2003 and 2008 (Figure 4, below.) Oil prices temporarily dropped during the Great Recession, but are now back up above $100 barrel.

Figure 4. World crude oil production and monthly average Brent spot oil price, both based on EIA data.

Whether or not recent oil production really is sufficient for a growing world economy is debatable. Certainly in terms of supply equaling demand, there was enough. But in terms of how this supply was divided, it has been very unequal (Figure 5).

Figure 5. Oil consumption based on BP’s 2013 Statistical Review of World Energy.

The big historical users of oil, that is the United States, the European Union, and Japan, have seen their use of oil drop, while oil use has continued to rise in the rest of the world. The countries that have seen a drop in oil consumption also tend to be the countries that experienced the greatest downturn during the Great Recession. These same countries are now struggling with slow economic growth and little gain in the number of high-paying jobs available.

There is good reason to expect that oil use and economic growth would be highly correlated. This expected correlation comes in two different directions—from the demand side and from the supply side. From the demand side, if businesses are growing, and if workers have jobs that allow them to buy an increasing amount of goods that use oil (such as cars or motorcycles, or new houses), the demand for oil products is likely to be growing as well.

Availability of oil is also important from the supply side—that is making and transporting goods. As mentioned previously, oil is required to transport goods, and it is used in many other places in the economy—such as in growing food, in the construction of buildings, and as a chemical feedstock. Of course, if oil is cheap, it is much better on the supply side than if it is expensive, because if it is expensive, the high price of oil tends to send the required selling price of goods upward, and (oops!) lead to fewer sales, cutbacks in production and recession.

How Financial Limits Tie in With Oil Reserves

There is a common belief that we have plenty if oil, because companies and governments report high oil reserves. For example, using BP’s 2013 Statistical Review of World Energy, the amount of oil that companies seem to think is extractable is (1668.9 billion barrels of oil reserves/ 31.5 billion barrels of oil produced in 2012) = 53 years worth of oil at the 2012 rate of production. If we look at oil resources that are supposedly available, which include oil that may be available with further exploration and development, the amount seems to be higher yet. So it doesn’t look like there could possibly be a problem.

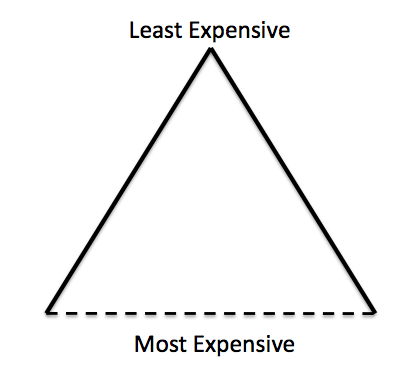

The reason why this belief is false is because the real cut-off is financial, and those making the estimates have no way of figuring out when the financial cut-off will occur. So they assume that we can extract oil that is very likely to stay in the ground indefinitely. One way of illustrating this problem is shown in Figure 6.

Figure 6. Resource triangle, with dotted line indicating uncertain financial cut-off.

Oil resources in the ground can be thought of as being somewhat like the triangle of resources shown. There is a lot of oil that is expensive to extract near the bottom of the triangle, but relatively little that is inexpensive to extract at the top. Oil companies start with the inexpensive to extract oil at the top of the triangle, and gradually work their way down through the triangle.

The least expensive oil is the oil that can be extracted with minimal problems. It is typically located near the surface, onshore, and can be extracted with the simplest equipment. Most of the easy, and thus cheap, to extract oil is now gone.

Now, if we want oil, we are being force to extract the more expensive oil, found lower in the triangle. Such oil may be deep under the sea, or near the North Pole, or may require hydraulic fracturing to extract. Sometimes the higher oil cost relates to indirect expense. For example, governments of oil exporters usually charge high taxes on exported oil. These taxes are used to keep their populations pacified with food subsidies and other benefits, such as desalinated water, so they do not revolt.

At the bottom of the triangle is an invisible financial limit, which I have shown as a dotted line. One way the limit “works” is by inducing recession in countries that obtain a very large percentage of their energy consumption from high-priced oil. Another way the financial limit works is by inducing financial collapse in oil companies. This happens when companies have huge up-front expense before they can recover their costs by selling oil they have extracted at high oil prices.

As an example of a company hitting such a financial limit, Brazil’s second largest oil company, OGX, is trying to extract oil offshore Brazil, including the presalt area (that is oil beneath a salt layer that is difficult to drill through). OGX recently missed a debt payment because of its inability to obtain sufficient financing to work its way around a long-term negative cash flow situation. It reports that most of the oil fields it has explored are not economically viable–the cost of extraction would be higher than the price available in the world oil market.

Because the financial limit is invisible, companies and government agencies have no way of excluding the too-expensive-to-extract oil from their estimates. A reasonable case can be made that at $100 barrel, oil price is already adversely affecting the economy. Without quantitative easing and deficit spending, the economy would be in recession from high oil prices now. Thus we are already hitting the financial limit, even though companies can see a huge amount of more oil that is theoretically available to extract. The only minor catches are that (a) consumers need to be able to afford to purchase the high-priced oil, and (b) oil companies need to be able to obtain ever-more cheap financing to extract it.

How Oil Limits Tie in with Energy Returned on Energy Invested (EROI)

Dr. Charles Hall and others have calculated Energy Return on Energy Invested (EROI) for various fuels (Hall and Klitgaard 2012). The basic premise is that the more energy is needed to extract a fuel, the less efficient it is for providing needing desired energy for society. Hall’s research has shown that over time, the EROI for each fuel extracted tends to decline. This is very similar to the rising cost of extraction over time I am showing in Figure 6. The main difference is that I include all relevant costs, including wage costs, taxes, financing costs, and distribution costs, rather than just energy costs associated with extraction.

I have talked about required oil prices already being too high, and thus causing recession. In many ways, this is parallel to saying that the EROI of oil is already too low, and is leading to recessionary problems.

Some people (for example, Garcia 2009, which seems to be used in used in Randers 2012) would like to use EROI comparisons to determine what might be a suitable substitute for oil. I do not consider this a suitable use for EROI for several reasons:

- Substitutability away from oil is very poor in the short-term, especially if we are up against a financial limit that will make substitution even more difficult in the future. The use of EROI in this manner assumes that substitution is really possible.

- EROI does not consider some important variables, including the timing of investment (and thus the need for long-term financing), and governments’ dependence on tax revenue from oil. Even in the US, governments obtain considerable revenue from oil extraction. According to Barry Rogers in the Oil & Gas Journal, in North Dakota, the total “government take” amounts to $33.29 on an average $80 barrel of tight oil.

- If substitution were to take place, huge transition costs would be incurred, such as early retirement of the current vehicle fleet, and higher capital costs (and thus more energy expenditure) related to the new vehicles. Simply considering EROI would miss these costs.

Conclusion

When we hit oil limits, we are really up against Liebig’s Law of the Minimum. Applied in this situation, this law would say that if a necessary fuel is missing, the economy will not operate properly. This law originally was used to describe a problem in raising agricultural crops. If a necessary nutrient (such as phosphorous) was not present, it didn’t matter whether excess amounts of other nutrients were added. The plants could not grow properly unless the missing nutrient was available.

With oil, the situation is pretty similar. The economy cannot operate as usual, without an adequate supply of cheap oil (or in EROI terms, high-EROI) oil. All of the talk about substitution for oil is irrelevant, if our problem is a financial problem we are hitting right now, or in the very near future.

In order to have prevented our financial problems, several years ago we would to have needed to put in place a substitute for oil with very little or no transition costs. Ideally, the substitute could have kept transportation costs very cheap—comparable to the cost before the run-up in oil prices starting about 2003. Ideally, the substitute would also have worked for other oil uses, such as for powering irrigation pumps, for powering agricultural equipment, and as a chemical feedstock for asphalt, for medicines, for herbicides and pesticides. To be truly an oil substitute, the new product would need to be available sufficiently cheaply that it could be taxed heavily, to make up for lost revenue from oil royalties and other taxes.

Now we are faced with what looks like an unsolvable problem. We need a cheap oil substitute, yesterday. The stories we heard saying, “Substitutes will work when the oil price rises high enough,” were a bunch of nonsense. The folks who came up with this idea didn’t realize what a negative impact high oil prices have on the economy. A high-priced substitute for oil is not at all helpful. Neither is one with huge transition costs.

Without a substitute, we need to figure out how to live in a very changed world, one facing financial collapse–a very difficult problem indeed.

Hi Gail.

First of all excuse me for my poor English because I’m not a native speaker. I’m Spaniard. I have read in different fonts that the money the FED creates via the mechanism euphemistically called “quantitative easing” never ends in the real economy: it never gets out from the banks accounts. In their opinion, quantitative easing is done in order to prevent banks bankruptcies and never gets out from the financial system, a monster bigger than the real economy.

If they are right, how oil companies can benefit from QE? I’m not living in the USA and I’m not an economist, so I’m not sure if the USA is living a moment of easy credit for consumers and companies.

Thank you for your time.

Quantitative Easing is part of a “package” that includes low short term interest rates and deficit spending as well.

One of the things quantitative easing does is keep long term interest rates artificially low. Investors looking for higher yield will then invest in a variety of kinds of things–speculative oil drilling, which will tend to help keep oil supply up; investors buying houses to rent out, which will help raise housing prices, so there isn’t so much of a problem with people having more debt than their house is worth; and perhaps even factories–but it is not at all clear that many factories are being built with the money. There are probably quite a few speculative bubbles in asset prices because of QE, in stock prices, farm prices, commercial real estate, and housing prices.

With the low interest rates, new homes and new cars are more affordable. This helps keep up “demand” for houses and cars, and thus employment in these industries. Other types of building is also affordable–for example, government building and commercial building.

Low interest rates also lead to a need for less high taxes, because the interest on the government’s own debt is lower. If the government doesn’t need to raise taxes, it leave the taxpayers with more dollars, that they can spend on other things (including gasoline and diesel for vehicles).

As you say, the Quantitative Easing also helps out the banks, by moving iffy debt out of the system.

QE also assists the US in continuing to issue large quantities of debt, because this way, the market does not get over-saturated with US debt.

If the Federal Reserve were not doing all of these things, it seems like there is a good chance that interest rates would be much higher, taxes would need to be higher, and the US would be officially back in recession. In such a case, oil prices would likely drop too low, because of the lower demand for oil. If this were to happen, the output of oil would drop–perhaps not immediately, but there would be a drop in the drilling of new wells. Over time, this would lead to a drop of oil supply.

So I think you are right. The US is living on a moment of easy credit for consumers and customers.

Dear Gail and Others

One of my pet peeves is that analysts frequently fail to take into account behavior changes. They project trends which (predictably) hit brick walls, with the implicit assumption that human behavior won’t change as the wall approaches. The assumption about inflexible behavior may be a good assumption, or a poor assumption. But my complaint is that by ignorning the potential for changed behavior, the analyst mislabels the problem. The problem IS NOT the trend, the problem revolves around the human behavior change.

Let me give you an example. Lester Brown, in an interview with Chris Martenson (which is probably behind a paywall) projects that food production is peaking and thus dire consequences await an increasing human population. Lester is assuming that everything will continue on trend and the trend will hit a brick wall and that will be that.

Now I will show two examples of analysts who look at behavioral changes which can mitigate the projected disaster. First, look at Brian Kaller’s article:

http://www.resilience.org/stories/2013-10-14/nothing-needs-to-be-wasted

Brian asks the question, ‘Is it necessary to really waste 30 to 50 percent of the food we produce?’ And the answer, of course, is no.

As a second example, see Toby Hemenway’s essay:

http://www.patternliteracy.com/103-is-food-the-last-thing-to-worry-about

Toby points out the work of Howard Odum showing that the primary production of food is low on the complexity chain. Would a sane government (which must exist somewhere in the galaxy) sacrifice food production to save Wall Street? Toby also mentions the fact that gardens are grossly underutilized, that more productive (but more labor intensive) farm methods can be used, and other factors which are subject to human volition.

It MIGHT be true that a species with the very limited sapience identified by George Mobus will drive right into the brick wall at 90 miles per hour, but it is also possible that at least some people will avert the wall through changes in behavior. By failing to consider the potential for change, I think people like Lester Brown just foster an attitude of hopelessness. When we are hopeless, we shut down our problem solving apparatus. As stupid as the ‘equal time’ rule appears on TV news programs, I think that those programming interviews should make an effort to interview people who are doing something about the particular issue. It doesn’t have to be in the same program, but suppose Chris had ended with ‘and in the coming weeks we will be talking to people who are doing something about food supply’. I know that Chris and Adam Taggart are both personally doing something. You’d never get that from Lester’s comments.

Don Stewart

Another example…

It is common in the Peak Oil community to say that ‘food is oil’ or that ‘without genetically modified crops we would all starve’ with the background understanding that the high tech world of genetic engineering is fuel intensive.

Take a look at these graphs:

https://gallery.mailchimp.com/a57841e3f724f29382a368209/images/2013_08_corn_web.jpg

They’re small, and I don’t know how to enlarge them. So I will tell you what they say.

1. Genetically engineered corn has exploded since the year 2000.

2. Yields have not increased very much at all since 2000.

3. Most of the increase in corn production is due to more acreage planted in corn.

4. Corn prices have risen pretty dramatically.

5. We are diverting a large share of the corn crop to ethanol.

These graphs tell you a number of things, if you bother to connect the dots:

1. Genetically engineered corn shows no signs of solving an real problem except that it does make bales of money for Monsanto and Bayer.

2. If we want higher yields of corn, then we are likely going to have to use more labor intensive methods rather than more fuel intensive methods.

3. All those government officials who actually work for Monsanto should be tried for treason. Government efforts to prevent us from knowing when a product has ‘Monsanto content’ are certainly not government ‘of, by, and for the people’.

4. A loyal citizen wouldn’t buy a product with any ‘Monsanto content’.

5. Bill Clinton talked about the idiocy of corn ethanol in his talk at Omega. Government programs which require the production of corn ethanol are similar exercises in stupidity and/ or treason.

I submit that the great majority of Peak Oil pundits claim:

‘We are running out of oil and since food is nothing but oil, we will all starve’.

A more nuanced claim would be that:

‘Some of the most emergy inefficient processes revolve around stupid programs. IF we can look at graphs and draw sensible conclusions from them, and IF we can regain control of the government from the lobbyists, THEN maybe we don’t have to starve even as oil production declines.’

Don Stewart

Another good example of non-linear thinking rather than straight line projections:

http://www.resilience.org/stories/2013-10-14/an-interview-with-paul-hawken-we-choose-a-path-of-regeneration

Both Rob Hopkins and Paul Hawken were at Omega. The link is to Rob’s interview with Paul. You will see that Paul has a non-linear sense of the possibilities…both for good and for bad.

Don Stewart

George Mobus is one of the most perceptive observers around. Time spent reading him is always worth while. He’s more or less given up on Homo Sapiens, Current Model. But somehow one doesn’t despair having read him.

Mass food production via gardening could be a game-changer, I agree.

Change of behaviour requires Leadership, the thing we always hear about from the so-called global leaders and never get.

None of them tire of spouting the ‘recovery and growth is just around the corner’ lie, but not one takes a photo op with a spade in their hand…….

Hello Chris, I saw this article today too. “9 Depression-Era Frugal Habits You Need to Pick Up”

Which I will put up here for any interested, it was a main stream media article…

http://www.savvysugar.com/Great-Depression-Saving-Tips-32030865?utm_source=outbrain&utm_medium=cpc&utm_campaign=outbrain_cpc_savvy

Thanks Scott, this looks good. Frugal is good. I recently heard that Warren Buffett said he could live comfortably on $60 K per year. Happy for him…

Cheers, Chris

Hello Chris, this is from another main stream media site that I read today.

http://www.newsmax.com/Newsfront/debt-default-shutdown/2013/10/12/id/530731

Chris

Like the old chestnut: a rich man asks a poor man how much of his wages he spends on food and so on. ‘About all of it, sir.’ ‘Well, there you are, that’s your problem! I only spend about 5% on living costs, the rest I invest. Follow my example and you’ll get on better!’

Hello, I will put these links up for anyone interested… Here are a couple of things I was looking at and listening to today.

This first one is an interview of David Stockman about the coming financial crisis. A good interview outlining a big crisis coming that likely will be larger than 2008.

http://kingworldnews.com/kingworldnews/Broadcast/Entries/2013/10/5_David_A._Stockman.html

This one is an article about the honey bees and how Diesel may be to blame. It would be good to electrify our tractors and all vehicles if we only could.

http://www.newsmax.com/SciTech/Science-environment-pollution-chemicals/2013/10/05/id/529449

Scott

Thanks! I hadn’t seen the diesel and honey bee article. With the honey bees, the problem seems to be a bunch of factors working together.

Stockman has been saying something similar for a while now, but another good interview doesn’t hurt.

Edit: I listened to the Stockman interview. It was well worth listening to. He doesn’t understand the oil problems underlying our current problems, but he understands why the Fed is out of ammunition, in trying to fix financial market problems.

Dear Gail

I’ll just observe about the honeybees that they are an example of David Korowicz’s thesis about the collapse of complex system. A bee or a human or the global industrial system are all complex. The bee can endure one or two or three insults (such as pesticides or being trucked to distant locations) but at some point the bees defenses cannot cope with the insults and the colony collapses. Korowicz says something very similar about the global industrial and financial system.

And we have a very poor record trying to predict exactly when the insults will overwhelm the homeostatic systems.

Don Stewart

Agreed!

Dear Gail and Others

Here is a link to Joel Salatin talking about several things we have discussed in this particular post and also in other recent posts.

http://www.permaculturevoices.com/permaculture/permaculture-voices-podcast-015-joel-salatin-talks-to-the-next-generation-of-farmers/

I suggest you go to the 55:30 mark for a discussion of a one acre homestead. You will get advice about how to configure the house as well as things to grow. The house recommendations cover many of the same features as an Earthship, but without the use of dry soil as an insulator or the generation of your own electricity or the use of gravity for the water system. He is assuming you already have a house, you just want to make it more efficient. Listen for about 4 minutes.

Then skip to the 1:09:00 point where he talks about his distaste for farmer’s markets and expresses his opinion that distribution is the inefficient, weak link in the local food system, and the farmer’s market is the most inefficient link of all. He talks about the alternatives. He also drops the comment that Amazon Fresh may put Wal-Mart out of the food business. (My opinion is that the kitchen garden is the real answer to fresh produce, and he recommends a kitchen garden in his first answer.)

The next question relates to his summation of his life experiences. He says that we mostly have no idea how productive land can be if we approach it with care and imagination and husbanding its inherent capacity for fertility. Treating a farm as something to which you add inputs is a fundamental error (Liebig’s Law is a Distraction?).

The last two questions and answers total about 15 minutes. Of course, Joel is always informative, even when describing which pair of pants he chose to wear today…so feel free to listen to the whole thing.

Don Stewart

The Economist urges “Let decaying British towns die”:

http://www.economist.com/news/leaders/21587790-city-sicker

And I always thought the Economist represented the cornucopian view that there’s enough for everybody.

Quote:

“Hasn’t America tried more-or-less letting cities grow and shrink naturally, and isn’t the result Detroit? Yes, but this is to focus on one side of the ledger. America has some shockingly ruined cities, but it also has shockingly successful, fast-growing ones, like Houston and Raleigh. And Detroit was brought down partly by the weight of pensions owed to its police and other public-sector workers. In British towns, pensions are either much better funded or are paid by the national treasury.”

Is that so? Yet still the UK government has debt over a trillion pounds sterling.

I haven’t looked at European figures, but I cannot imagine that the governments will possibly be able to pay the pensions promised (or alternatively, that the money provided by the pensions will be worth very much, when it actually comes to buying goods and services).

We are beginning to see a situation with a shrinking “economic pie” instead of a growing one, in the US, Europe, and Japan. Everything looked great, as long as the model showed growth forever, and citizens getting a reasonable percentage of a growing economy. But if the economy is flat or declining, it is very hard to make the numbers work out right.

I suspect households in Japan have high ownership of Japanese government bonds because households are trying to fund their own retirements. I am afraid Japanese households will run into the same difficulty as everyone else.

Can anyone tell me how much of GDP is deficit spending and quantitative easing? And how much oil the US. consumes versus how much oil it produces. The numbers seem way off!

With respect to oil production vs oil consumption oil consumption. The US in 2012 produced 6.5 million barrels a day of crude oil. The US’s net imports was 7.4 million barrels a day. (The US actually imported 8.5 million barrels a day of crude, and exported enough products to bring the net imports down to 7.4 million barrels a day.)

The US consumed 18.5 million barrels a day of oil products in 2012. The difference between the 18.5 million consumed and the (6.5 million bpd of US crude) plus (7.4 million bpd) is 4.6 million bpd of “other stuff” the US produces, that isn’t really oil, but is included in the total to hide the problems with crude oil. It includes ethanol, plus “natural gas liquids” (propane, butane, and ethane), plus “refinery expansion” that takes place when the US processes crude oil (including imported crude oil).

So one way of looking at the amounts would be to say that the US imported 7.4 million barrels a day out of 18.5 million barrels of consumption or 40% of the total. If you don’t give the US credit for all of the other stuff, the US imported 7.4 million barrels a day, out of (7.4 + 6.5 =) 13.9 million barrels of oil per day, or 53% of the total.

With respect to the question about how much of GDP is deficit spending and quantitative easing? Quantitative easing does not directly go into the GDP calculation, so the answer in one sense for QE is $0. In another sense, both the deficit spending and quantitative easing (to keep interest rates low) were necessary to keep the economy from imploding, so a fairly large percentage of GDP is a result of these programs.

In total the amount of US debt is over $16 trillion. The national debt increased from $14.8 trillion at 9/30/2011 to $16.1 trillion at 9/30/2012, an increase of $1.3 trillion. This compares to US GDP of $15.7 trillion for 2012, or about 8%. I don’t think it is very helpful to compare this deficit to GDP, because we don’t pay taxes on GDP–taxes are on a much smaller base, predominantly wages. Wages amounted to $6.9 trillion dollars. If the shortfall were to be collected as a tax on wages, it would need to amount to something like 19% of wages. (Social Security taxes were raised by 2% of wages, so part of the shortfall has already been made up.)

Dear Gail and Others

There is so much disagreement about houses that I feel a brief exploration of the topic is in order. The first stop recommend is this video with Paul Wheaton talking earlier this year in San Diego. Click on the video. Go to the 10:45 minute point and then the 21 minute point and then to the 29 minute point for brief discussions of Annualized Thermal Inertia, really cheap houses, and solar drying of food. Then click on the second link for an explanation of what is going on in terms of using earth as a thermal inertia storage medium. For the sensitive, I will warn you now that Paul sometimes uses strong language…I don’t think these short clips are too bad.

http://www.permies.com/forums/f-88/podcast

http://www.richsoil.com/wofati.jsp

The Earthships also use thermal inertia, but incorporate some other ideas as well.

An early Arctic explorer spent a winter on Greenland in a sort of tube. By the end of the winter, his breath had frozen around him so that he could barely get out of the tube. At the other end of the spectrum, Adam and Eve wandered around Eden and most likely never built a house. In effect, the garden was their house. So humans can survive in all sorts of places called ‘home’. Parisians are noted for sleeping in little cubbyholes and living in cafes. Citizen Kane built Xanadu, with countless rooms and so many treasures they could not be catalogued. California in the 1950s invented the notion of ‘bringing the outside inside’, and built patios that melted seamlessly into drawing rooms. I once ate dinner in a California winery where it was hard to tell what was on the inside and what was on the outside. Many Mediterranean cultures used houses as a place to hide the women from prying eyes. In San Francisco, women use their house as a place to decorate themselves in preparation for their forays into the cafes. Today, many people have home offices. I once saw a house in New Jersey which was built as a weekend corporate getaway for the company bigwigs in Manhattan–not a practical thing in it and very expensive. In short, there are a wide variety of different practical definitions of ‘home’ or ‘house’.

It is obvious that the requirements one asks of a house depend on how one plans to use it. Paul Wheaton thinks and acts like a homesteader. Most of the day will be spent out and about doing the work that needs to be done. The purpose of the house is, first, shelter and then practicality (including things like computers) and then comfort at the end of the day. If we think about the 1950s suburban house and then we think about how David Holmgren proposes to repurpose it for the Age of Energy Descent, we find quite different purposes and consequently different activities taking place and physical modifications.

Earthships, which came along 30 or so years ago, were typically built on cheap land in the arid West by people who didn’t have the psychological need for close neighbors (and maybe had the opposite) and who wanted to be more self-reliant. The land was cheap because it didn’t have utilities. If you have ever tried to get utilities extended to a remote homesite, you know what an expensive proposition that is. So the houses were designed to be off-grid. And if you are going to be living in that glorious landscape, it seems a crime to live in a tube such as sheltered our Greenland explorer. The Earthships cleverly integrated the thermal mass of earth, the insulating power of used tires packed with dry dirt (dry dirt is important in the two links above), a clever water cycle, full use of gravity, and the greenhouse effect of a wall of glass. Somewhat reminiscent of the Biosphere effort in Arizona.

One of the threads which unites all these houses is the desire for energy efficiency. There is little or no external energy used for heating and cooling. Unless you live on an island with trade winds, that means insulation with earth. What you will choose to build depends on your land, your neighbors reactions, your own proclivities, how you plan to use your house, and your budget. All these guys avoid mortgages.

Finally, a great deal of energy in the home goes to the manipulation of food: refrigerators, stoves for canning, glasses for canning, etc. Solar drying cuts out a lot of that external energy requirement. (Fermentation cuts out the processing energy, but requires either glass or earthenware storage which does require energy to make).

Don Stewart

Dear Gail and Others

Two more pictures of unconventional houses in Paul’s talk. At 58:30 he shows a picture of a tiny house. At 1:01 he shows a picture of an insulated shipping container which has been turned into a house.

Note Paul’s discussion of the plain front on the shipping container. The inside and back are nicely fixed up to be friendly to humans. The front is plain so that the owners are not drawing the attention of people driving by. This is probably illegal (as is the tiny house). Having a house which doesn’t draw attention helps if you are doing something illegal.

Why are these illegal? Because humans are inherently drawn to dividing ‘us’ from ‘them’. In the Robber’s Cave experiments in Oklahoma in the 1950s, boys were selected who were as uniformly white and middle class as the scholars could manage. When taken to the camp, the boys nevertheless quickly divided into two groups and the scholars had to cut the experiment short to avoid violence.

If you have a shipping container in your back yard to store all the surplus stuff you have, you are one of ‘us’. Possibly up to your eyeballs in debt, but ‘comfortable’. People who refuse to go into debt and live instead in shipping containers are definitely ‘them’. A shipping container in the yard storing stuff does not have a negative impact on property values (except in very ritzy zip codes), while very few people want anyone living next to them who is so ‘other’ that they live in a shipping container.

Don Stewart

Don

Great stuff.

You missed out: home as a place to watch TV and absorb propaganda……

Gail Tverberg, My friend and fellow economist the late John Attarian

and the quarterly journal The Social Contract have thought about and

published on many of the issues of concern to you and many who

comment on your postings. In the spring of 2003, John served as the

editor for a special issue of The Social Contract on “Ecological

economics: highlighting the work of Herman Daly.” John also

published a number of articles in The Social Contract and elsewhere

outlining his concerns over issues such as peak oil and the end of

cheap oil, population sustainability and immigration, the sustainability

of our entitlement systems and government debt, and the like. One

of the best pieces that John did was his article on “Economism”

which one can read from the following link:

http://www.thesocialcontract.com/artman2/publish/tsc1504/article_1326.shtml

In 2002 John published an article in The Social Contract on the end

of cheap oil. Prior to his untimely demise at 48 in late 2004, John

and I discussed a lot the oil situation and we both concluded, as

John set out in two short article he published that year, that we were

likely to hit peak oil before the end of the next administration which

turned out to be Bush’s second. We both expected an oil shock

which occurred in 2007 and 2008 and was surely a catalyst in

engendering “the great recession” as the Canadian economist Jeff

Rubin has pointed out.

There should have been a serious discussion of this issue in the

2004 election, but there wasn’t. After the oil shock, it should have

been discussed in the 2008 election, but again wasn’t. And it

clearly wasn’t in the 2012 substanceless election.

Over the years I have argued with John, with people connected with

The Social Contract and with others that pamphleteering on these

issues isn’t enough. What is needed to get these issues seriously

discussed to start coming up with some solutions and action is to

open up our political processed to third parties willing to discuss

them and the hard choices we face. But this is not possible

without voting reform since, as you can see from the following link

on Duverger’s law, it is our system of plurality voting which engenders

and sustains our rigid, and increasingly dysfunctional, two party

system. In reading the link:

http://janda.org/c24/Readings/Duverger/Duverger.htm

people need to be aware that when Duverger (a Frenchman) speaks

of a majority he actually means a plurality in most cases.

I am not as pessimistic as some about our ability to tackle our

problems if we can get a serious discussion of them in the

public forum. A necessary, though not sufficient, condition for

this is voting reform. On this score, I would invite you and your

readers to take a look at Chapter 1 and Appendix 7 of the

electronic book on my website http://www.nationalrenewal.org.

Given the announced retirement of Senator Saxby Chambless

and our Michigan Senator Carl Levin, I would like to try to

organize an effort to solicit their support for initiating in the

Senate a voting reform act to open up our political processes

to third parties and independent candidates. I hope that you

and your readers might take a look at my website and that

you might consider in one of your postings looking at the

issues I have tried to raise there.

John Howard Wilhelm, Ph.D.,

Economics

Ann Arbor, Michigan

Tel. 734/477-9942

Thanks for the information and the links. I read the article, “Economism and the National Prospect” by John Attarian. He does a good job of describing the situation. It is almost a national religion at this point. Of course, the fact that we live in a world with limits means that at some point, (likely not far away), it becomes clear that the national religion is a false one–everything falls apart.

Dear Gail and Others

Some of you have claimed that Earthships are ‘for rich people’. Here is one desgined for Haiti:

http://earthship.com/Designs/simple-survival

Now, this uses industrial trash such as used tires and cans and bottles and it uses new industrial products such as cisterns and solar panels and rebar and insulation. If you are ONLY interested in solutions which would work in the total absence of an industrial system and completely without reused trash, this isn’t for you. On the other hand, if you are interested in living well in the system as it exists today, but without going into debt, and being far more independent of the vagaries of the economy, then take a look.

http://earthship.com/Designs/simple-survival

Also, if you want to find out more about black water and gray water and how they are treated, just use the appropriate words and you will turn up a wealth of information. The graywater from the living area in the back of the house, for example, flows by gravity through PVC pipes to the garden beds up in the greenhouse part of the dwelling. They use panty hose as a grease trap.

Don Stewart

Dear Ms Tverberg,

You might be interested to learn that Shell CEO Peter Voser is now sharing your view on the limits of shale:

http://www.ft.com/cms/s/0/e964a8a6-2c38-11e3-8b20-00144feab7de.html#ixzz2h72mIF5H

“Mr Voser also said rhetoric about the US shale revolution being exported to other countries was “hyped”, and that the rest of the world was in an early “exploration phase” which could yield “negative surprises”.

Yes, I saw that article. Thank you. It is good that oil company executives are speaking out.

I wonder if there is an upper limit of the percentage of GDP that a country can spend on energy before it precipitates economic contraction? I suppose part of the answer depends on whether the energy dollars spent get recycled into the economy effectively, or removed from it.

Here is my list of adjustments that this country can make to downsize its energy/resource demand-

1. Ration public money spent on medicare for the elderly to what would be considered today as severe in degree. Medicare payments would be reserved for those expenditures that have the lowest cost to benefit ratio (yes- rationing).

2. Downsize the military at about 3 %/yr until we are down about 50% from today. It would still be massive.

3. Drop meat consumption by half/capita, and drop all farmland biofuel subsidies.

4. Carbon tax (at an equivalent of 25 cent/gallon, with the proceeds to used for efficiency and innovation credits).

5. Lastly- we need a campaign to popularize euthanasia and hospice. it shouldn’t be hard to sign out.

Of course, in the big analysis, these measures are just buying a bit of time.

Thanks for your writings Gail.

“I wonder if there is an upper limit of the percentage of GDP that a country can spend on energy before it precipitates economic contraction?”

It’s 5% for oil. Details are here:

22/7/2013

US oil demand peak was in 2007

http://crudeoilpeak.info/us-oil-demand-peak-was-in-2007

There can be a difference in calculation if you use retail prices or cost of a barrel of oil–you sometimes see a different figure for that reason.

Good reference, Matt. However, do you ever wonder why the Europeans could survive better on more expensive fuel, or the Japanese and Chinese. Why is the USA paradigm the only one we track? Europe and Japan don’t produce any gasoline, and China but a fraction of their demand, despite that their wage rates are much lower.

I would argue that the Europeans are not surviving better on more expensive fuel. Their economies are collapsing. The taxes on oil were to try to keep those economies from collapsing sooner–get people to use smaller cars and ride the trains or bicycles to use less oil. The taxes on oil have helped redistribute oil to China and India.

That’s quite right about Europe. Americans might look at the prices and say: How on earth can they manage?! But cities are configured differently and distances generally so much smaller.

When I worked in central London, I was able to walk 15 minutes to one office, and then 15 minutes in the opposite direction to another from a conveniently located apartment, but otherwise the metro rail and bus services work pretty well: even from the suburbs of London one can get to town in say 12 minutes by train and have a rail station some 10 to 20 minutes walk away.

But high fuel costs are certainly having an impact on businesses that have to use a lot, and this is driving down discretionary income also. The European Union are starting to get worried about high energy costs and the adverse impact on industry (a bit too late!).

I generally agree with you.

I think on Medicare, we have to have some recognition built in that at advanced ages, it doesn’t make as much sense to do very much. Intensive care, and for that matter brain surgery, doesn’t make sense on 85 years olds. There are simple palliative things that should be available to all (pain relief, for example). And caffeine is a great stimulant–works well for many elderly.

People used to die at home. My husband’s aunt died at our home, while living with us, a few years back. She was being served by hospice. I hired a young woman to come in and stay with her in her declining days, while I was at work.

Hello Gail, it looks like we may have to change our diet as the future goes on and the good fish get more scarce. You may not believe this but when I was a teenager in the early 1970’s you could still buy Abalone in cans like Tuna. Now it looks like Jelly fish will be on the menu, I hope they are eatable, not sure though….

http://www.nbcnews.com/science/jellyfish-are-coming-experts-tangle-exploding-population-8C11352067

The overfishing problem and the jellyfish in the wake of other fish problem is pretty severe. I noticed that a few days ago, there was an article about jellyfish paralyzing the water intake at a nuclear reactor in Sweden.

humankind is a species unique in its ability to grant itself ‘human rights’

looked at dispassionately, human rights is in direct conflict with the laws of nature, because nature makes laws, we do not.

but human rights are with us, if only in the short term, because we have the means to sustain them.

unfortunately very few people realise that our ‘human rights’ are supported by energy input of fossil fuels, and that before hydrocarbon burning added itself our lifestyle, the concept of human rights didn’t exist.

To refer to your ‘list of essentials ‘ there, they contravene everybody’s human rights, to live life as we wish. —A dead end I agree, but one we shall continue with until we get to that dead end.

Your list can be filed under Wish politics, and Wish economics

Saw this today the first time… my be interesting.

Regarding Oil-Limits if found some time ago the LFTR technology quite intriguing. Now there is an other but similar concept, that seems removes some deficiencies of the Liquid Fluoride Thorium Reactor: the Dual Fluid Reactor (http://dual-fluid-reactor.org/video).

Still is a fluid based Thorium breeder reactor – so “explosion” potential is extremely minimized and all the other advantages as less Plutonium, simple and available fuel, simple exchange and remove-ability of fuel.

Still some game-extension-options available 😉

Thanks, very interesting on the Thorium reactors. I think we will be able to make plenty of electricity, but we still do not have a good enough battery. We can make hydrogen with it to store the energy, but that is difficult to deal with. We can make lots of electricity it seems but to make it portable is the problem still.

Even if we can make unlimited electricity it still does not solve our overpopulation problem and resource scarcity.

But that was hopeful news for clean power.

Scott

For those following the current stalemate in Congress, Chris Hedges reports on the ideology of a republican leaders such as Ted Cruz who are bent on derailing Obama Care. The parallels that he draws between the Christian Right and the fascists are compelling. He also rails against the liberals in the Democratic Party who he believes have enabled the corporate take over of government and have their own way failed the poor and dispossessed. I don’t see any way out of this impasse unless a large external event such as a stock market tumble forcing a compromise. http://m.truthdig.com/report/item/the_radical_christian_right_and_the_war_on_government_20131006

Behind this all the fact that there is no way that we can pay for current programs, much less pay for Obama Care as well. We are at a point where citizens (with stagnating wages) cannot afford the government we have put in place.

Dear Ms. Tverberg,

You might like this recent interview with Peter Voser, CEO of Shell, who admits that investments by the company in US shale have not paid off, and that shale in other countries is in for “negative surprises”.

http://www.ft.com/cms/s/0/e964a8a6-2c38-11e3-8b20-00144feab7de.html#axzz2h1hw3IHV

Interesting! Thanks for the link.

Gail, over at zero hedge was this paragraph: “Recognizing that the economy is still weak, the Fed at its latest meeting yet again declined to begin tapering. When the Fed is finally forced to cut back, interest rates will rise, Wall Street will call for relief, and the economy will slump. This may be delayed with additional printing for a couple of months, but the adjustment will occur and it will be severe, probably much worse than in 2008. However, this time there are no arrows left in the government’s quiver to spend or print its way out of trouble.”

“No arrows left in the govt. quiver” caught my eye, because that’s what I keep coming back to is the question of what happens after QE and huge borrowing are no longer on the table? Since 08 some form of QE has been the go to strategy to keep defaulting paper at bay, but without it, uh, well… My thinking on this is the Fed will QE right up until it is forced to stop by one market force or another and the govt. will borrow 700b-1trillion a year until congress stops it.

The govt. shutdown has been in the works for a long time now as the R’s want to reduce deficits, so we may be seeing pressure to taper QE and reduce deficits taking hold both in this 4th qtr. I’m very interested to see how all this plays out and it’s fiscal consequences for the economy. We may be on that edge of discontinuity you mention.

I think we are thinking along the same lines.

In addition, there is no real way the budget can be balanced. The Federal Government is on a “cash” basis, rather than an accrual basis. This means that even if Social Security does have some funds theoretically built up, those funds have in fact already been spent, and replaced with non-marketable government debt. Thus, as the baby boomers retire, the entire cost of their Social Security and Medicare benefits must be paid for on a pay-as-as you go basis. This is happening at a time when young people are having a hard time getting decent jobs, and are also being saddled with student loans.

Yes, indeed. My oldest son is working in China because he could not find a job in the US. My middle son is working in the US but would not be able to get to work if we had not bought him a car that he could never afford given his income. My youngest I have no idea what to tell him to do he just finished high school.

Dear Gail and Others

Relative to the Omega Institute conference. If you are interested in trying to foster changed behavior, there are two speakers that I highly recommend.

First, I would watch Bob Berkebile on Sunday morning. Bob is an architect. Whether you agree with his ‘living buildings’ designs or not, I think you will be impressed by the way he gets in touch with his clients. He goes into the tornado stricken town of Greensburg, KS, and asks them questions no one has ever asked them before. Then he designs a green solution which includes their concerns. I think you will particularly notice the key role played by local schools in his solutions. Notice that the school officials have no sense that they play a larger role.

Second, watch Bill Clinton’s keynote address. Clinton talks about the President of Brazil and how she is doing things right…much like Bob Berkebile is doing things right. He contrasts her approach with that of Assad, Jr. in Syria.

What else does Clinton have to say?

1. Complaining about things is disempowering.

2. Every day offers opportunities

3. Distinguish between Headlines and Trendlines.

4. A key concern is sustainable farming. We have many rich countries who cannot feed themselves who are buying up land, farming it unsustainably, and pushing out small farmers. This is disastrous.

5. A rational health care program for the US requires thinking, and you almost never see that in DC. It’s like walking and chewing gum at the same time. We are paying an extra trillion dollars each year to be sicker and live shorter lives.

6. We are all interdependent. Divorce is not an option. The Israelis and the Palestinians don’t realize it, but they are interdependent.

7. The four main obstacles to achieving the world we want:

a. Gross inequality

b. World is too unstable…people are scared

c. Unsustainable production of energy and other resources

d. Consciousness is not what it needs to be if we are to develop solutions which will work. We have to let our eyes overrule our ideologies.

He spoke some more about Health Care. In Rwanda, the Clinton Foundation is involved in their effort to develop and implement, by 2020, a health care system which Rwanda can afford with zero foreign aid. We have to learn to pay attention to how other people do it…just like a football coach looks at films of the other team. And we have to confine our debates to the realm of reality.

He recalls a conference he attended in Brazil where all the players in a contentious issue were sitting at a table discussing the issues ‘as if they had half good sense’…which you never see in DC.

Don Stewart

Thanks! Most of those ideas sound good.

Clinton’s point 7: as it has always been and ever shall until the last human animals take their last breath – fear, struggle, insecurity, fights for dominance, inequality (ineradicable), irrational hatreds.

These can destroy the most promising societies and relations. We are an animal that cannot be sure that the next member of its species to come along will not enslave, torture, murder or abuse it, or just plain lie (Clinton was good at that was he not?)

Mostly it doesn’t happen, of course – when it does there is no real society: in war -and even more in civil war – it happens a lot. The Old Testament refers to mothers eating their own children and families murdering one another at times of stress and starvation.

Take a look at any office and its politics….. Look at family quarrels…. All of it irrational and wasteful. In practical terms, inevitable.

Everything good beautiful and sane is destroyed eventually, maybe to re-emerge somewhere else.

It’s the old curse. Someone asked the sage Rumi in the 13th century to prove he had a perception of the Divine and special powers to help mankind and improve its lot, so – in the middle of winter – he produced a perfect-looking apple, which was delicious. The third bite produced a nasty worm. Spitting it out, the eater said: ‘How can a Heavenly Apple have a worm in it?! ‘ Rumi replied that everything that enters the Earth is corrupted, and it’s foolish to expect anything else.

Not that we are excused from struggling, of course!

Dear Xabier and Others

There was a lot of content in several of the presentations about ‘changing consciousness’…but it wasn’t about drumming or chanting or praying. It was mainly about giving people experiences through the built environment and also giving instant feedback.

I believe it was Clinton who talked about the importance of using the advances in communications to give rapid feedback to people to assist learning. This is a huge topic, and I won’t go into it here. Suffice to say that the information revolution opens up lots of opportunities.

In terms of ‘experiences change consciousness’, it all started with Jeremy Rifkin who talked about how the changes humans have experienced from early gatherer/ hunter days to today’s abundance of data on demand have changed the way we think. (The counter argument is that our hormonal systems haven’t changed appreciably…just the data they are operating on.) Then we saw a succession of architects who show us pictures of the built environment which not only achieve ecological goals but also change the way we perceive events.

For example, if you are sitting at your dining table in an Earth Ship that you yourself made out of earth and junk and you go over to the banana tree growing in your solar greenhouse and pick a banana watered by the graywater from your own house which came from water catchment on your roof, and you sit down and eat the banana and save the peel for composting and look out at the blackwater nourished plants outside and the animals they have attracted, and you are cool in the summer and warm in the winter because of all the thermal mass surrounding the house, is your consciousness different than that of someone buying a million dollar apartment on Park Avenue in NYC?

Does the Yoga class which meets in the sewage treatment plant at Omega amid lush greenery have a different consciousness than a yoga class meeting in a typical high school basketball gym?

David Orr gives the concluding talk about how Oberlin College built their new building specifically to give the students a daily experience which will foster a new consciousness. What does it mean when students can go skinny dipping in one of the pools outside while a meeting is in session in the building?

What does it mean when school buildings are recognized as essential community assets, as opposed to a way to teach kids to pass multiple choice tests with high efficiency? If kids at schools are regularly exposed to adults who are there on serious, adult business, does it make any difference?

What does Majora Carter mean when she says that ‘my neighborhood needs to become the kind of neighborhood where people go to parks’. What does it mean when Mayor Bloomberg talks about the proliferation of parks in his regime, and comes to Majora’s park to pose with his shovel?

To put all this together, I can’t refer you to a 5 minute segment of any single talk. It’s woven through practically all the talks.

Don Stewart

Somehow, I have a very difficult time seeing these new buildings with lots of glass and solar panels being affordable by more than a tiny percentage of the population. Suppose the economy goes down hill. More people will lose their jobs. The information revolution is likely to come to a swift halt, as the huge energy inputs required to keep up Internet is no longer available. Perhaps electricity is not available at all, or only very intermittently.

Most of the folks with the fancy new homes will owe mortgages to banks on them. As the economy goes downhill, their inability to pay these mortgages will become one of the drains on the economy. Banks fail.

Other members of the economy are jealous of the fancy homes. They are without jobs and hungry. They throw stones through the windows of the fancy new homes. New windows are not available for replacement. Oops!

The money that was spent on the fancy new homes could instead have been spent on simple tools for all–shovels and wheelbarrows, and instruction in simple skills that do not depend on our whole modern energy network. How to get along without solar panels and things that can’t last indefinitely.

But somehow, people have latched onto the belief that we can somehow hold on to what we have with more and more fancy stuff for at least a few, made because we still have some energy. And they have stopped thinking about the fact that each of these expenditures requires trade-offs for other expenditures that could be made, and the necessary debt leads to other limits down the line.

Gail

Regarding the ‘fancy and expensive’ houses. I can only recommend that you listen to Michael Reynolds talk about the economic independence that living in an Earth Ship brings. The residents typically have no debt, no utility bills, and they are growing a lot of food. The place is beautiful because of all the plants.

Reynolds repaired the ancient Mercedes that he drives (on grease) with salvaged auto door panels. The houses are built with walls of plastic bottles and metal cans from dumps. If the production of trash stops, then someday Michael will have to look for different materials. But it’s a sane and sensible way to live today. If the solar panels fail and nobody is making them anymore, then he will live without electricity. Or maybe the wind turbine will still function. He notes that some have worked for 30 years with zero maintenance. He doesn’t need a lot of electricity.

As for the sewage. I am sure that Omega spent more than is required simply because they are in an upscale neighborhood. Albert Bates, in a distinctively downscale neighborhood, accomplishes the same biological transformation of waste into nutrients with much simpler facilities. I doubt that the neighbors in Dutchess county would appreciate Albert’s outdoor pissoir.

You can find lots of material on the obstacles local governments have placed on Michael’s houses. But things may be changing. He has a current project in midtown Manhattan which has not yet been vetoed by the City.

You look at it and say that ‘this won’t survive the kind of collapse I foresee’. Albert would tell you ‘I thought the same thing in the 1970s’. What all the speakers see around them is gross ecological ignorance and abuse which is destroying the ability of the the planet to support the abundance of biological life that it might support, and the architecturally inclined are trying to design in such ways that the biological processes which are at work are transparent. David Orr said ‘we learn when we see and experience’.

As for the rampaging mobs, I recommend Michael’s words about ‘tomato independence’.

I won’t try to convince you that making a built environment designed to have a positive impact on human consciousness is a good idea. Some will be intrigued and will investigate.

Don Stewart

Gail

Just one more thought for you. This all began with a derisive comment about the sewage treatment building at the Omega Institute being a tourist destination.

Now let me ask you this question. Suppose the person who made the derisive comment actually observed the transformation of their own waste into biological nutrients every day…by the design of the built space. Every day they would observe a miracle.

Do you think they would have made the derisive comment? Would they vote for dumping sewage into the Chattahoochee? Would they assume that gigantic sewage plants with complex designs are a good expenditure of the taxpayer’s money?

Don Stewart

i’m not quite sure what the options are. I may have missed something–I don’t read the comments together with what preceded them, so sometimes forget what the original context was.

In the long term, the only options we have are simple ones that we can make with local materials, and that local people can afford. Thus, both big and small sewage plants are probably out, unless the small plant truly can be made with local materials by local people. In the long run, the best option is probably less dense population, so that sewage is not such a problems.

In the short term, there is a problem with sewage. Then whatever is cheap per person and can be maintained by local people, without electricity use,”works”.

Don

I’m with you on many points.

Radical change in architecture, education, community resilience is urgently needed: but that’s not where our civilization is heading. We are reinforcing our mistakes and misunderstandings.

On the whole, one feels like a passenger strapped in while a delusional drunk is in charge of the bus…….

Xabier

The conclusion of the session was a panel. Someone posed the question ‘what keeps you from jumping off the bridge?’. Mostly, I think, they concluded that it was the work itself. David Orr, who is a political scientist, said ‘we will win because we are right’. Whether you have that much faith in truth and justice will determine how you line up on the issue of ‘why don’t you just jump off the bridge?’.

On a slightly different tangent. I have started reading The Social Conquest of Earth by E.O. Wilson. It’s been on my shelf for a while. Bill Clinton contributed this blurb:

‘I just finished The Social Conquest of Earth, a fabulous book’.

On page 44: ‘The cohesion forced by the concentration of groups to protected sites was more than just a step through the evolutionary maze. It was, as I will elaborate later, the event that launched the final drive to modern Homo Sapiens.’

Now, a little background. Wilson shows that biological diversity increased greatly as the social insects proliferated. The insects evolved slowly and the other plants and animals evolved along with them. Many plants are now absolutely dependent on the social insects. So the introduction to Earth of the social insects multiplied Life.

Social Humans, and especially their invention of agriculture, have been a disaster for Life. Page 16: ‘Wherever humans saturated wildlands, biodiversity was returned to the paucity of its earliest period half a billion years previously.’

So, taking Bill Clinton at his word, he understands that the campfire which nourished humans and made us what we are is no longer adequate. Arguably, even the campfire has fallen apart under the spell of Ayn Rand and the Neoliberal Economists. But restoring the campfire consciousness would not be adequate to avoid disaster given the capacity of modern humans to destroy Life. Therefore, as difficult or impossible as it may seem, we have little choice but to try to find and nourish a new consciousness. That, or hoard some resources for one last, solitary party.

Or, perhaps, adopt the Permaculture (or any other variant of biological agriculture) ethics and intervene to maximize biological life on the land you have an influence on. It is conceivable that humans could increase Life, as the social insects did, but the odds are pretty long.

Don Stewart

Don, Omega is located on one side of Long Pond lake. There are about 300 persons living around the lake full time. Omega brings in 500 folks a week for drumming and tennis for lawyers and what not. They used to collect the feces of these 500 people in large underground tanks. They would then to sucked into tank trucks and trucked the 90 miles to the transfer station in Albany, New York. What happened after that I do not know. That is the same place my septic tank non-digestible waste is trucked to.

They switched to their on-site sewage treatment for the other unsustainable influx of 500 people. I do not know how much heavy metal load we are now getting into our aquifer from the continuous buildup of un-processable components like mercury in the feces. How long will it be sustainable?

As an aside there is a 435KV extra high voltage transmission line to one side of Omega and a 230KV high voltage transmission line to the other side of Omega. The 230KV is to be upgraded to 435 extra high as part of the New York State Energy Super Highway. The superhighway will bring stranded nuclear and coal power from upstate New York through my backyard to New York City. The upstate generators are running at reduced rates due to the death of the old upstate cities. This will allow full throttle use of the nukes with full throttle nuclear waste production and full throttle coal burning with full throttle air pollution including more mercury.

Another aside it is interesting to see how many folks from Manhattan are buying and building up mini farms 100 miles north of New York City as insurance. Beautiful new barns are being built that are architecturally superb, new tractors are bought, servants are hired to do the work etc….

edpell

There was discussion about the utilities using eminent domain to take the Omega property. I get the impression that they are trying to fight it by getting the neighbors involved.

As for the toxic metals. Biological waste treatment can sequester metals. Janine Benyus touched on this during her talk. Geoff Lawton, when he was doing his Greening The Desert work in Jordan, found that if he made swales and planted plants, they sequestered salt from this heavily salted earth. I don’t think he really understood why, at the time. Janine Benyus now seems to understand it, to some extent. Biology works miracles.

Don Stewart

edpell

To your point about new tractors and barns. Darren Doherty is a Regenerative Agriculture consultant in Australia. He has been spending some time in the US recently. He says that lots of people in Australia have made money in the housing boom and decided to buy country land. Then, some of them give him a call to figure out what they should be doing with the land.

He says that when he pulls into their driveway, he gets a good idea how long they will last. If they have a shiny new tractor and a barn stuffed with new, but useless, stuff, they won’t make it very long.

Of course, if you have enough money, and continue to make money in the city or through financial means, then the farm just becomes a sink, albeit a pleasant one. If you ever get to Asheville, NC, go to see the Biltmore Estate. New York City money built this medieval estate in the early 20th century. They imported stone masons from Italy, etc. They aspired to be self-sufficient, with artisans of various kinds working in blacksmith shops and bakeries and things. But I am sure it just lost money. But there was plenty more coming in all the time.

Don Stewart

all creatures discharge waste

we are therefore faced with a problem:

We leave it where it is and walk away from it

We remove it to somewhere else

We pay somebody else to move it and hopefully find a use for it

Speaking in a collective sense, I fear that we will expect the latter to go on happening precisely because it ‘always has’, forgetting that universal sewage disposal is a luxury of a minority and is energy intensive.

Bloggers on here know that, but I’m afraid that if you bring up the subject in polite conversation (risky) among most people, the solution is that the ubiquitous ‘they’ will figure out a solution to the energy problem

While some may be able to cope with the problems, most will not, and there is much more to this than recycling for beneficial use. Without the necessary energy input, we will be faced with the disease that accumulated body waste creates within any community, I covered this in my article ‘Survive’ which shows just what is costs to keep a crowded community healthy. http://www.endofmore.com/?p=763

And we ARE crowded.

Earthships no doubt function very well. I can only suggest building them in the fetid heart of Lagos or Mumbai

Dear End of More

The original Earth Ships used composting toilets. Now they use flush toilets but the waste never leaves the property. It is processed biologically and is released outside, as you can see from his pictures.

You could, of course, still use composting toilets. In the New Mexico high desert, where he developed these, graywater is entirely too valuable to waste.

I have no idea what he will do with the wastewater in Manhattan. I do know that NYC has some building codes which are designed to reduce stormwater runoff. Some new big buildings near the Battery have used innovative ways to reduce the storm flooding. So I suppose NYC may be more amenable to innovative ways to deal with water than some other cities.

Don Stewart

Dear Gail and Others

Thanks to some rather slurring comments, I found out about the Omega Institute’s symposium ‘Where Do We Go From Here’. You can find it at:

http://www.eomega.org/workshops/conferences/where-we-go-from-here

Find the place where it invites you to participate in the Live Streaming and click. It’s free. The sessions today are supposed to play starting today and lasting for a few days. The sessions tomorrow can be viewed live or as they replay them. Bill Clinton’s address on Friday evening will play at least at 2pm tomorrow, Sunday.

To determine whether you are interested in watching, here are my comments from today. First, I believe Gail assumes that our financial economy requires exponential growth, and that lacking exponential growth, the financial economy will collapse and take the real economy with it. This would be in line with Hubbert’s observation in the 1980s about what happened in 1929 in the US economy: we either failed to disconnect the physical economy from the financial debacle on Wall Street, or else we refused to do so. I don’t see any of the speakers making that assumption. I would say that they are all assuming that the real economy can change more or less graciously even if financial values collapse. They all seem to assume that Apple and Google and Twitter can have high values even if the traditional bricks and mortar economy is sick. Your opinion on that subject may be the most important determinant of whether you want to watch.