The Peak Oil story got some things right. Back in 1998, Colin Campbell and Jean Laherrère wrote an article published in Scientific American called, “The End of Cheap Oil.” In it they said:

Our analysis of the discovery and production of oil fields around the world suggests that within the next decade, the supply of conventional oil will be unable to keep up with demand.

There is no single definition for conventional oil. According to one view, conventional oil is oil that can be extracted by conventional methods. Another holds it to be oil that can be extracted inexpensively. Other authors list specific types of oil that require specialized techniques, such as very heavy oil and oil from shale formations, that are considered unconventional.

Figure 1 shows the growth in unconventional oil supply for three parts of the world:

- Oil from shale formations in the US.

- Oil from the Oil Sands in Canada.

- Oil characterized as unconventional in China, in a recent academic paper of which I was a co-author. (Temporarily available for free here.)

Figure 1. Approximate unconventional oil production in the United States, Canada, and China. US amounts estimated from EIA data; Canadian amounts from CAPP. Oil prices are yearly average Brent oil prices in $2015, from BP 2016 Statistical Review of World Energy.

Oil prices in 1998, which is when the above quote was written, were very low, averaging $12.72 per barrel in money of the day–equivalent to $18.49 per barrel in 2015 dollars. From the view of the authors, even today’s oil prices in the low $40s per barrel would be quite high. Since the above chart shows only yearly average prices, it doesn’t really show how high prices rose in 2008, or how low they fell that same year. But even when oil prices fell very low in December 2008, they remained well above $18.49 per barrel.

Clearly, if oil prices briefly exceeded six times 1998 prices in 2008, and remained in the range of six times 1998 prices in the 2011 to 2013 period, companies had an incentive to use techniques that were much higher-cost than those used in the 1998 time-period. If we subtract from total crude oil production only the production of the three types of unconventional oil shown in Figure 1, we find that a bumpy plateau of conventional oil started in 2005. In fact, conventional oil production in 2005 is slightly higher than the later values.

Figure 2. World conventional crude oil production, if our definition of unconventional is defined as in Figure 1.

I would argue that far more crude oil production was enabled by high oil prices than I subtracted out in Figure 2. For example, Daqing Oil Field in China is a conventional oil field, but greater extraction has been enabled in recent years by polymer flooding and other advanced (and thus, high-cost) techniques. In the academic paper referenced earlier, we found that the amount of unconventional oil extracted in China in 2014 would be increased by about 55%, if we broadened the definition of unconventional oil to include oil made available by polymer flooding in Daqing, plus some other types of Chinese oil extraction that became more feasible because of higher prices.

Clearly, this same kind of shift to more expensive extraction methods has occurred around the world. For example, Brazil has been attempting to extract oil from below the salt layer of the ocean using advanced techniques. According to this article, Brazil’s “pre-salt” oil production was expected to exceed 600,000 barrels per day by the end of 2014. This oil should count, in some sense, as unconventional oil.

Massive investments in the Kashagan Oil Field in Kazakhstan were enabled by high oil prices. Some initial production began, but was discontinued, in September 2013. Production is expected to resume in October 2016.

There are clearly many smaller fields where higher extraction was made possible by high oil prices that allowed oil companies to utilize more advanced techniques. Deepwater drilling also became more feasible because of higher prices. Another example is Russia, which is reported to have heavy oil extraction that would not be commercially feasible if oil prices were below $40 to $45 per barrel. If we were to add up all of the extra oil production in many areas of the world that was enabled by higher prices, the total amount would no doubt be substantial. Subtracting this higher estimate of unconventional oil in Figure 2 (instead of the three-country total) would likely result in more of a “peak” in conventional oil production, starting about 2005.

Thus, if we think of conventional oil production as that which is possible at low oil prices, the forecast by Colin Campbell and Jean Laherrère was pretty much correct. Production of conventional oil did seem to peak about 2005 or shortly thereafter. We simply don’t have the data to estimate how much we could have extracted, if oil prices had remained low. Furthermore, oil prices did rise substantially, relative to 1998 prices, making Campbell’s and Laherrère’s forecast of higher prices correct.

I suppose that we could even say that if conventional oil were all that we had in 2005 and subsequent years, supply would have fallen far short of demand, based on Figure 2. This last statement is somewhat debatable, however, because there would have been other feedbacks, as well. It is possible that if total supply were very short, oil prices would have spiked to an even higher level than they really did. The resulting recession would likely have brought prices down, and temporarily brought demand back in line with supply. If prices had stayed low, there might have been a second round of shortages, with an even greater supply problem. This, too, might have been resolved by another price spike, quickly followed by another recession that brought world demand back down to the level of supply.

Of course, conventional crude oil isn’t the only type of liquid fuel that we use. When we add all of the pieces together, including substitutes, what we find is that since 1998, broadly defined oil production (“liquids”) has been rising quite rapidly.

Figure 3. World Liquids by Type. Unconventional oil is from Exhibit 1. Conventional oil is total crude oil from EIA, and other amounts are estimated from EIA International Petroleum Monthly amounts through October 2015. (EIA’s category “Other Liquids” is referred to as Biofuels in Figure 3, since this is its primary component. Other liquids also include coal and gas to liquids and other small categories.)

In fact, since 2005, Figure 4 shows that the single highest year of growth in oil production (broadly defined) was 2014, with 2.47 million barrels per day. (This is based on crude oil data from EIA Beta Report Table 11.b, plus values for other liquids from EIA’s International Energy Statistics. Annual amounts for 2015 were estimated based on data through October.)

Figure 4. Increase over prior year in total oil liquids production, based on EIA data. 2015 other liquids amounts estimated based on data through October 2015.

Figure 4 shows that the increase in oil supply in 2015 is almost as high as in 2014. The 2005 to 2015 period shown indicates a lot of “ups and downs.” The only two high years in a row are 2014 and 2015. This would seem to be at least part of our “oil glut” problem.

Exactly by how much oil production needs to increase to stay even with demand depends upon price–the higher the price, the smaller the quantity that buyers can afford. At a price of $100 per barrel, a reasonable guess might be that about 1 million barrels per day in consumption might be added. If categories other than crude oil are increasing by an average of 440,000 barrels per day, per year (based on data underlying Figure 4), then crude oil production only needs to increase by 560,000 barrels per day to provide an adequate supply of fuel on a total liquids basis.

If production of crude oil is actually increasing by more than 2.0 million barrels per day when only 560,000 barrels per day are needed at a price level of $100 per barrel, clearly something is badly out of balance. According to EIA data, the countries with the five largest increases in crude oil production in 2015 were (1) US 723,000 bpd, (2) Iraq 686,000 bpd, (3) Saudi Arabia 310,000 bpd, (4) Russia 146,000 bpd, and (5) UK 106,000 bpd. Thus, US and Iraq were the biggest contributors to the global glut in 2015.

What Is Going Wrong?

Not only did a lot of people hear the Peak Oil story, a great many responded at once. Governments added requirements for more efficient vehicles. This tended to lower the quantity of additional oil supply needed. At the same time, governments added mandates for the use of biofuels, also reducing the need for crude oil. Arguably, the US-led Iraq war, which began in 2003, was also about getting more crude oil.

Oil companies also rushed in and developed oil resources that might be profitable at a higher price. These new developments often take more than ten years to produce oil. Once companies have started the long path to development, they are unlikely to stop, no matter how low oil prices drop.

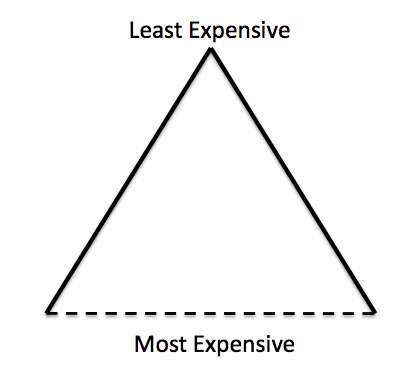

It is becoming apparent that if oil prices can be raised to a high enough level, a lot more oil is available. Figure 5 shows how I see this as happening. We start at the top of the triangle, where there is a relatively small quantity of inexpensive oil, and we gradually work toward the expensive oil at the bottom.

Figure 5. Resource triangle, with dotted line indicating uncertain financial cut-off.

The amount of oil (or for that matter, any other resource) isn’t a fixed amount. If the price can be made to rise to a very high level, the quantity that can be extracted will also tend to rise–in fact, by a rather large amount. The “catch” is that wages for the vast majority of workers don’t rise at the same time. As a result, goods made with high-priced oil soon become too expensive for workers to afford, and the economy falls into recession. The result is prices that fall below the cost of production. Thus, the limit on oil supply is not the amount of oil in the ground; instead, it is how high oil prices can rise, without causing serious recession.

While wages don’t rise with spiking oil prices, increasing debt can be used to hide the problem, at least temporarily. For example, cars and homes become less affordable with higher oil prices, since oil is used in making them. If governments can lower interest rates, monthly payments for new homes and cars can be lowered sufficiently that new car and home sales don’t fall too far. Eventually, this cover-up reaches limits. This happens when interest rates start turning negative, as they now are in some parts of the world.

Thus, by ramping up buying power with low interest rates and more debt, governments were able to get oil prices to stay above $100 per barrel for long enough for producers to start adding production that might be profitable at that price. Unfortunately, the amount of additional oil demand isn’t really very high at that price. So, instead of running out of oil, we ran into the reverse problem–too much oil relative to the amount that the world economy can afford when oil prices are $100+ per barrel.

The attempt by governments to fix the oil shortage problem didn’t really work. Instead, it led to the opposite mismatch from the one we were expecting. We got an oversupply problem–a problem of finding enough space for all our extra supply (Figure 6). Unless we have infinite storage, this pattern clearly cannot continue forever.

Figure 6. Weekly ending stocks of crude oil and petroleum products through July 29. Chart by EIA.

Eventually, this oversupply problem is likely to result in “mother nature” cutting off oil production in whatever way it sees fit–oil prices dropping to close to zero, bankruptcies of oil companies, or collapses of oil exporters. With lower oil supply, we can expect recession.

Misunderstanding the Real Problem

In the early 2000s, the story that Peak Oilers came up with (or perhaps the way it was interpreted in the press) was that the world was “running out” of conventional oil, and that this would lead to all kinds of problems. Oil prices would rise very high, and oil depletion would take place over a long period, as shown in a symmetric Hubbert Curve. As a result, at least small quantities of additional energy products with high “Energy Returned on Energy Invested” (EROI) were needed to supplement the energy products that would be produced based on the slowly depleting Hubbert Curve. Our oil supply problems were viewed as a unique situation, calling for new and unique solutions.

In my view, this story came about through over-reliance on models that likely were accurate for some purposes, but not for the purpose that they later were being used. One of these over-extended models was the supply and demand curve of economists.

Figure 7. From Wikipedia: The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

This model “works” when the goods being modeled are widgets, or some other type of goods that does not have a material impact on the economy as a whole. Substituting high-priced oil for low-priced oil tends to make the economies of oil importing countries contract. This effect indirectly reduces demand (and thus prices) for many products (not just oil), an impact not considered in the simplified Supply and Demand model shown in Figure 7. Also, the very long lead times of the oil industry are not reflected in Figure 7.

Two other models that were used beyond the limits for which they were originally designed were the Hubbert Curve and the 1972 Limits to Growth model. Both of these models are suitable for determining approximately when limits might be hit. Even though Peak Oilers have believed that these models can accurately determine the shape of the decline in oil supply and in other variables after reaching limits, there is no reason why this should be the case. I talk about this problem in my recent post, Overly Simple Energy-Economy Models Give Misleading Answers. Thus, for example, there is no reason to believe that 50% of oil will be extracted post-peak. This is only an artifact of an overly simple model. The actual down slope may be much steeper.

The Real Story of Resource Limits that We Are Reaching

Instead of the scenario envisioned by Peak Oilers, I think that it is likely that we will in the very near future hit a limit similar to the collapse scenarios that many early civilizations encountered when they hit resource limits. We don’t think about our situation as being similar to early economies, but we too are reaching a situation of decreasing resources per capita (especially energy resources). The resource we are most concerned about is oil, but there are other resources in short supply, including fresh water and some minerals.

Research by Joseph Tainter and by Peter Turchin indicates that some of the issues involved in previous resource-based collapses are the following:

Growing Complexity. Citizens who discovered they were reaching resource limits typically tried to work around this problem. For example, hunter-gatherers turned to agriculture when their population grew too large. Later, civilizations facing limits added irrigation to raise food output, or raised large armies so that they could attack neighboring countries. Making these changes required greater job specialization and more of a hierarchical system–two aspects of growing complexity.

This increased complexity used part of the resources that were in short supply, since people at the top of the hierarchy were paid more, and since building new capital goods (today’s example might be wind turbines and solar panels) takes resources that might be used elsewhere in the economy. Eventually, growing complexity reaches limits because costs rise faster than the benefits of growing complexity.

Growing Wage Disparity. With growing complexity, wage disparity became more of a problem.

Figure 8. People at the bottom of a hierarchy are most vulnerable.

I have described this problem as “Falling Return on Human Labor Invested.” Ultimately, this seems to be a major cause of collapse. Workers use machines and other tools, so this return on human labor has been leveraged by fossil fuels and other energy resources used by the system.

Spiking Resource Prices. Initially, when there is a shortage of food or fuel, prices are likely to spike. A major impediment to long-term high prices is the large number of people at the bottom of the hierarchy (Figure 8) who cannot afford high-priced goods. Thus, the belief that prices can permanently rise to high levels is probably false. Also, Revelation 18: 11-13 indicates that when ancient Babylon collapsed, the problem was a lack of demand and low prices. Merchants found no one to sell their cargos to; no one would even buy human slaves–an energy product.

Rising Debt. Debt was used to enable complexity and to hide the problems that people at the bottom of the resource triangle were having in purchasing goods. Ultimately, increased debt was not successful in solving the many problems the economies faced.

Ultimately, Failing Governments. Governments need resources for their purposes, whether hiring armies or making transfer payments to the elderly. The way governments get their share of resources is through the use of tax revenue. When people at the bottom of the hierarchy were cut out of receiving adequate resources (through low wages), the amounts they could afford to pay in taxes fell. Governments would sometimes collapse directly from lack of tax revenue; other times collapses occurred because governments could no longer afford large enough armies to defend their borders.

Ultimately, Falling Population. With low wages and governments requiring higher tax levels to fund their programs, people at the bottom of the hierarchy found it difficult to afford adequate nutrition. They became more susceptible to plagues. Loss of battles to neighboring countries could at times play a role as well.

Lessons We Should Be Learning

Even if we made it past peak conventional oil, there is likely a different, very real collapse ahead. This collapse will occur because the economy cannot really afford high-priced energy products. There are too many adverse feedbacks, including increasing wealth disparity and the likelihood of not enough revenue for governments.

We can’t count on long-term high prices. The idea that fossil-fuel prices will gradually rise, and because of this, we will be able to substitute high-priced renewables, seems very unlikely. In the United States, our infrastructure was mostly built on oil that cost less than $20 per barrel (in 2015 dollars). We know that with added debt and greater complexity, we were temporarily able to get oil to a high-price level, but now we are having a hard time getting the price level back up again. We really don’t know how high a price the economy can afford for oil for the long term. The top price may not be more than $50 per barrel; in fact, it may not be more than $20 per barrel.

We need to look for inexpensive replacements for both oil and electricity. Many substitutes are being made to produce electricity, since indirectly, electricity might act to replace some oil usage. There is considerable confusion as to how low these prices need to be. In my opinion, we can’t really raise electricity prices without pushing economies toward recession. Thus, we need to be comparing the cost of proposed replacements, including long distance transport costs and the cost of adjustments needed to match electric grid requirements, to wholesale electricity prices. In both the US and Europe (Figure 9), this is typically less than 5 cents per kWh. (In Figure 9, “Germany spot” is the wholesale electricity price in Germany–the single largest market.) At this price level, producers need to be profitable and to pay taxes to help support governments.

Figure 9. Residential Electricity Prices in Europe, together with Germany spot wholesale price, from http://pfbach.dk/firma_pfb/references/pfb_towards_50_pct_wind_in_denmark_2016_03_30.pdf

Replacements for oil need to be profitable and be able to pay taxes, at currently available price levels–low $40s per barrel, or less.

We need to be careful in aiming for high-tech solutions, because of the complexity they add to the system. High-tech solutions look wonderful, but they are very difficult to evaluate. How much do they really add in costs, when everything is included? How much do they add in debt? How much do they add (or subtract) in tax revenue? What are their indirect effects, such as the need for more education for workers?

We need to be alert to the possibility that solar PV and most wind energy may be energy sinks, rather than true energy sources. The two hallmarks of providing true net energy to society are (1) being able to provide energy cheaply, and (2) being able to provide tax revenue to support the government. When actually integrated into the electric grid, electricity generated by wind or by solar generally requires subsidies–the opposite of providing tax revenue. Total costs tend to be high because of many unforeseen issues, including improper siting, long-distance transport costs, and costs associated with mitigating intermittency.

Unless EROI studies are specially tailored (such as this one and this one), they are likely to overstate the benefit of intermittent renewables to the system. This problem is related to the issues discussed in my recent post, Overly Simple Energy-Economy Models Give Misleading Answers. My experience is that researchers tend to overlook the special studies that point out problems. Instead, they rely on the results of meta-analyses of estimates using very narrow boundaries, thus perpetuating the myth that solar PV and wind can somehow save our current economy.

Too much debt, and too low a return on debt, are likely to be part of the limit we will be reaching. Investment in complexity requires debt, because complexity requires capital goods such as wind turbines, solar panels, computers and the internet. The return on this additional debt is likely to drop lower and lower, as complex solutions are added that have less and less true value to society.

We need to remember that as far as the economy is concerned, it is total consumption of energy resources that is important, not just oil. Wages reflect the leveraging impact of all energy sources, not just oil. If energy consumption per capita is rising, more and better machines can help raise output per capita, making workers more productive. If energy consumption per capita is falling, the world economy is likely moving in the direction of contraction. In fact, we may be headed in the direction of early economies that eventually collapsed.

When we look at the data, we see that world energy consumption per capita appears to have peaked about 2013. In fact, the big drop in oil and other commodity prices began in 2014, not long after energy consumption per capita hit a peak.

Figure 10. World energy consumption per capita, based on BP Statistical Review of World Energy 2105 data. Year 2015 estimate and notes by G. Tverberg.

The world seems to have hit peak coal, because of low coal prices. In fact, falling coal consumption seems to be the cause of falling world energy consumption per capita. Whether or not most people regard coal highly, coal is pretty much essential to the world economy. A recent decrease in coal consumption is what is pulling world energy consumption per capita down. We do not have any other cheap fuel to make up the shortfall, suggesting that our current downturn in energy consumption (shown in Figure 10) may be permanent.

Figure 11. World and China appear to be reaching peak coal.

We should not be surprised if the financial problems that the world is now encountering will eventually resolve badly. This seems to be how the Peak Oil story will finally play out. Without rising energy per capita, the world economy tends to shrink. Without economic growth, it becomes very difficult to repay debt with interest. Wealth disparity becomes more and more of a problem, and it becomes increasingly difficult for governments to collect enough revenue to support their needs. Our problems begin to look more and more like those of earlier economies that hit resource limits, and eventually collapsed.

{kind=link}

{kind=link}

Pingback: Gail Tverberg: How Peak Oil was misunderstood – Ecologise

Yoshua, I too wonder why the economy is not “burning”, growing at a fast rate, expanding, providing jobs for young people. I offer two factors.

1) Everything else is getting expensive. Food, housing, medical, education

2) The owner are looking forward and do see what we see and conclude there is no good reason to expand.

Indeed,

1) Human productivity on average is going down as even highly-educated and well paid humans now are facing strong competition from sophisticated computers and algorithms.

2) No more wealth can be obtained by a larger population and work force. With the current technological sophistication, people are increasingly becoming a liability. A burden on the system. Humanoid entropy generator automatons for the owners.

The growth numbers we are being fed are lies…. whatever growth is happening is simply shifting the pieces around …

Evidence: Global GDP is increasing — but corporate earnings are decreasing for the second year now…

The jobs reports are of course total fabrications.

I am sorry I have not yet finished up a new post. I hope to be able to finish it up today, and put it up tomorrow. We are beyond the 20 day limit for comments on my previous post. That is why new comments won’t work any more.

I will need to go to an out-of-state funeral this week, but I don’t know the date yet. My husband’s 43 year old nephew died–the funeral cannot be held until after an autopsy to try to figure out the cause of death.

Tim Groves, I am enjoying your posts.

I agree it is too late there will be no human solution to global warming.

The time scales are long so let’s all just remain calm.

Some news from a friend in Ittervoort, in the Netherlands.

“We had some very rough weather last night. 2 houses in the neighborhood burned down because of lightning. A large tree ended up on a car injuring 3 and a roof was blown off a building. The lightning struck in our house too which caused short circuit in a part of the house, at that time all equipment had already been unplugged so no real damage was done. The chance that our house is being struck by lightning is higher because of the solar panels on our roof which cause static electricity (which attracts lightning). Both houses that burned down also had solar panels.”

Solar panels – Catch 22. 🙁

World oil exports seems to have reached a plateau in 2005 at about 50 mbpd or half of world production (no imports from other worlds so far).

http://i574.photobucket.com/albums/ss189/Darwinian1/World%20Oil%20Exports_zpsghm7ufud.jpg

“No imports from other worlds so far” –LOL!

take your time gail it must be hard work churning out one article after another

It is on intermittent electricity–wind and solar PV. There are a whole lot of pieces to pull together.

” The raw reality ” (La cruda realidad) is a new Spanish documentary on the depletion and limits. Though it is of scanty interest for the habitual readers of FW, it gives us the opportunity to listen to Gail in three short but interesting interventions, where she is very elegant.

The interventions are in:

1:09:30

1:13:57

1:19:25

In the third intervention, the sum of his words, the background music, the gesticulation with his hands, gives a result of distress but also beauty … in my opinion.

Most of the persons is not in disposition to understand the relevancy and significance of his words. This is something that to me causes a great affliction.

Very nice to hear Gail. Reading between the lines, there is this enormous behemoth of an economy, with millions (or billions or trillions) of interdependent parts. For some reason, nobody figured out that these millions of parts could be calibrated so that they didn’t all flake out at once. I guess it was every man for himself, and the devil take the hindermost, and that has not turned out well.

I think that my sections were probably recorded when I spoke in Barbastro, Spain back in 2014.

1888 posts! Looks like wordpress fixed the large number of posts bug. Wonder what happens when we get to 2000?

I think it goes to 2001. I am trying to write a new post–takes time to research and write.

See, Fast Eddie, step up to the plate and post a short article here. After all it should be cake for you after all the teaching Gail gave you!. Believe you wanted to explore the BAU Lite topic and how its a non starter. Come on now, time for you to grow…..

Sure Gail wouldn’t mind looking it over first and edit.

https://m.youtube.com/watch?v=2cjRGee5ipM

No, you’re not one of those people,

We’ve already got the makings of a book from CTG on this … and still you cannot get it.

Would you like me to rewrite what he’s posted — making it compatible with the comprehension level of a 6 yr old?

Sure Fast Eddie, that would be OK with all of us because we realize the IQ level you display here.

You were the one, BTW, to suggest to Gail to write such an article for us all. What you need to do is divert some of that nonsensical comment space/time you devote here and channel it to some meaningful contribution. Having poor Gail shoulder all the hard work because of your addictive compulsive behavior to get attention is childlike. Come on, be a grown up and take a stab at some meaningful intelligent activity. My take is you are only able to play romper room fun and games tag. LOL

No turkey for you Vince! Besides, FE is kind of funny in a relentless sort of way.

@Sungr

FE lives in “Hobbit-Land”… and we don’t know how he looks like or what he really is… Hobbit? Elf? Ork? Human? Wizard? You never know….. he may even be a kind of Sauron or another evil force which wants to suc*k the spirit of live out of sheeple 😉

Unfortunately, the American Public probably has the comprehension level of not much more than a six year old. It is hard to rewrite all of these things down to the level required.

FE, you seem to have a strong understanding of the financial world. That world seems to me to be super strange now. Can you give us your take? Thanks.

Gail, getting back to the subject matter of your post, I think it is interesting that since around 2005, world conventional crude oil production has basically been flat, hovering just above 70 million bpd. Some producing nations are experiencing production declines these days, but Iraq has the potential to expand production and Iran has just been allowed back into the game. So I wonder what are the prospects for being able to maintain this 70 Mbpd+ conventional oil production volume over the medium-term?

Oil production volume depends on price as well as on demand. I’m not sure precisely how these three things relate to each other, although higher prices tend to suppress demand and producers attempt to match production to demand, obviously. Also, as you state, if the price rises, a lot more oil becomes available. Conventional oil tends to be cheaper to produce than unconventional oil, and so all other things being equal, the the current lower oil prices should favor more conventional and and less unconventional oil production. If rising demand drives prices higher slowly over a period of years, unconventional oil production becomes more affordable and so can be ramped up to meet demand. Put price crashes can wreck the best laid plans and send producers hurling toward bankruptcy.

Oil prices rose steeply from the time of the 2003 Iraq invasion until 2011, with a short downturn in 2008, while world liquids production rose almost continuously until 2015 despite mostly rising prices—thanks in no small part to mushrooming debt. The oil industry loved that. Exon Mobil’s profitability in the first decade of this century made it the envy of the corporate world.

But the party is now over. We have reached a point where the demand for oil is faltering and even steep price reductions have not done much to lift it. Could it be that too many years of high oil prices have damaged the rest of the economy so much that individuals and companies are no longer capable economically or psychologically of taking advantage of the benefits brought by today’s lower prices? Can we expect a modest economic recovery over the coming year or two as a result of lower oil prices, or should we expect things to get worse? Of course, reading the conclusion of your post, I know the answer to that.

Here is my answer. You aren’t going to like it.

Modern civilization has passed the point of the truth or reality principle. We have entered into media driven obfuscation and fantasy. Now, anything can just be made up or pulled out of a hat and presented to people. Nobody cares anymore, honest journalism and accounting has long ago disappeared.

This is when reality will become important again…when the top people are close to starvation. If you are paying attention, you will realize we are nowhere near that point.

The rest of us have only one role: accept the lies, work, and die. That’s it. That’s your purpose.

dolph, agree with minor change. When the top people can not feed the army then reality matters again.

” Now, anything can just be made up or pulled out of a hat and presented to people”

Humans have always preferred adventure stories or religion over the sometimes laborious process of separating facts from fantasy. On Sunday, how many folks are sitting in church pews vs how many are digging into Economist articles or evaluating climate studies?

However, this also creates job opportunities for priests, politicians, and many other categories of human predator. It also creates job opportunities for economic speculators who are wily enough to separate the REAL story from the illusions of the mass of true believers.

It depends a whole lot on how we define conventional oil, whether it has been flat since 2005. In fact, I expect that high prices and a fear of shortages were even a consideration in the Iraq war, and getting the Iraq oil into production. After all, George Bush (and also his Vice President, Dick Cheney) is known for saying, “The American way of life is not up for negotiation.”

Lower prices seem to be cutting out some American unconventional oil and some Chinese unconventional oil. Big projects which had been ongoing for several years are still going on, however, so some new oil will be coming online, to help offset decline in conventional oil. Thus, we are seeing enough new production right now that our oversupply problem continues to get worse, rather than better.

I am expecting now that companies will do as much as their creditors let them do, in terms of new drilling and new projects. There has to be a crack in the financial system, for a major cutback in production. Of course, this crack may not be far away, with all of the problems we have with European banks, Japanese debt, Chinese debt, etc.

Current prices are still high, relative to $20 per barrel oil that the infrastructure of the country was built on. Prices are low, but not low enough to encourage greater consumption. Of course, if prices get this low, no oil company can really make money on the situation, and production will drop quickly.

I don’t think we can expect a modest economic recovery at this point. I continue to be surprised at how long the economy can hold on. I won’t complain, of course. Exactly what goes wrong where, when, is not something I know. It could be derivatives, or something else. It is sort of like walking on thin ice, wondering if we are not going to sink in at some point.

From The Economist:

‘Grim employment prospects for young people around the world”

http://www.economist.com/blogs/graphicdetail/2016/08/daily-chart-23

“Unemployment among 15-24 year olds has risen to 13.1% in 2016 and is close to its historic peak of 2013. The rate is highest in Arab countries, at 30.6%…”

“In 2015, 25% of young workers in OECD countries were in temporary jobs and 26% were employed part-time…”

And from MarketWatch:

“Net investment at slowest pace since Great Depression.”

http://www.marketwatch.com/story/americas-investment-in-its-own-future-is-in-a-depression-2016-08-26

“… the median family’s annual inflation-adjusted income is still down more than $3,000.”

“Most troubling, there’s still very little investment in the buildings and equipment… that we ought to be putting into place today as the foundation for our prosperity tomorrow.”

“Since the recession, investments have fallen sharply, and they haven’t gotten back up again. It seems as if everyone is still scarred… by the collapse of asset bubbles in 2000 and 2006.”

“Net investment by government has also collapsed since the Great Recession…”

Well, except for government bailout, er, “investment” in the banking sector…

Seems like “prosperity” and “tomorrow” should be mutually exclusive words, given our present situation.

Anyone see a trend, and find a common thread in the financial/economic news these days?

Cheers

Here is the only trend that I see in anything:

-our world is corrupt and irredeemable top to bottom; everybody is lying about everything, all the time

As such, I find most analysis to be a waste of time. We are all Romans now.

You are making my morning. “our world is corrupt and irredeemable top to bottom; everybody is lying about everything, all the time” Yup.

The cheery philosopher, Kant:

‘Out of the crooked timber of Humanity, you will never make anything straight!’

Thanks for the links. Both of these issues are concerning. When not enough jobs are being added, it is young people who get left out.

Regarding net investment, I have not seen numbers on this basis–just on the gross investment basis, where they don’t look so terrible. Adding intermittent renewables puts us on a treadmill of investment being about equal to depreciation, but we still need to pay interest on what we have borrowed. We end up in an increasing amount of debt. We certainly have not been adding new road, or new schools. Just turning existing roads into gravel, to save money.

From yet another MSM source, this time Bloomberg:

http://www.bloomberg.com/news/articles/2016-08-26/gross-says-yellen-s-economy-may-never-walk-normally-again?

“[Yellen] is opening the door to creating even greater asset bubbles…This is not capitalism. This is providing…a wheelchair for an ailing economy. It may never walk normally again if monetary policy continues in this direction.”

– Bill Gross, Janus Capital Group

“Rivelle warned that central bank intervention to keep rates low and prop up asset prices may worsen the impact of an inevitable end to the current credit cycle…

“Every cycle in human history has ultimately come to an end…Credit-enhanced cycles come to worse ends than the normal kind.”

– Tad Rivelle, TCW Group

Also from Bloomberg:

“World’s Biggest Pension Fund Loses $52 Billion in Stock Rout”

http://www.bloomberg.com/news/articles/2016-08-26/world-s-biggest-pension-fund-loses-52-

billion-as-stocks-slump

Cheers.

Of course, it is energy consumption that has allowed the credit bubbles to form. Once energy gets expense to extract, we end up with all kinds of problems. We shouldn’t b surprised if a bubble breaks.

Japan and its pension fund are another problem. I believe that the government has been using the pension fund for its own purposes, trying to keep everything from collapsing. Can’t really work long-term.

OPEC’s crude oil production is 33 mbpd and their exports are 25 mbpd or 75 percent of the production.

http://peakoilbarrel.com/opec-crude-oil-production-charts/

http://fuelfix.com/blog/2016/08/16/market-currents-opec-oil-exports-at-25-million-barrels-per-day/

Not much have actually changed in OPEC in two decades if one only looks at crude oil production and exports.

http://www.theoildrum.com/files/09_OPEC_NET_EXPORTS_2009.PNG

With all of the ups and downs, total OPEC production continues higher. Inventories are more of a mystery, but it is clear to me that US inventories keep rising.

Yes, there has been a rising trend in production, consumption and exports with rising oil prices.

FE wrote:

“What I am wondering is …. what impact does this have on tourism?

Of course my website strifetravel.com is prospering …. we have never had such awesome offers for so many destinations…”

“Strife Travel”?? Yawn, bor-ing, been there done that…

You need to book a trip with “Extinction Tourism”, now that’s the ticket, a once in a lifetime experience!! But hurry, before it’s gone, cuz remember, supplies are limited…

https://www.theguardian.com/world/2016/aug/20/inuit-arctic-ecosystem-extinction-tourism-crystal-serenity

Cheers.

If you enjoyed that, you may also like Last Chance to See, an above-average 1992 potboiler by Douglas Adams and Mark Carwardine, went around the world in search of endangered species.

From the Amazon reviews:

Douglas Adams’ sense of humour is so strong, it could inject a bucketful of laughs into an obituary. Needless to say I wasn’t surprised when this book, his elegy for endangered species, turned out to have a welcome balance between laughter and melancholy.

Adams is joined by zoologist Mark Carwardine, as they use their last chance to see a variety of animals on the brink of extinction, such as the Komodo Dragon, the White Rhinos of Zaire, New Zealand kakapos, and Yangtze river dolphins. Adams, amateur wildlife lover, is wise enough to know the purpose of his journey: to shine some of the glare from his celebrity as a “science-fiction comedy novelist” on the issue of global extinction. He does wisely not to downplay the plight of these animals in the favour of commerciality, but manages to produce an entertaining work nonetheless. Carwardine, and the other people we encounter, sometimes come off as little more than characters in a Douglas Adams novel. I am hesitant to believe that everyone he encounters has the same dry, deadpanned British sense of humour. Nonetheless, the characters’ eccentricities further shed light on the kinds of people who are willing to undertake the monumental task of saving these beautiful beasts. It is not work for the dispassionate.

“The great thing about being the only species that makes a distinction between right and wrong,” he notes at one point, “is that we can make up the rules for ourselves as we go along.” Which brings up the second theme he hopes to illustrate here. Humans are dumb. No, that’s too simple. Humans are egotistical, selfish, wasteful, materialistic, impudent, and dumb. The single, overwhelming reason why most of these animals must fight for their survival is the sheer audacity humans have in moving into their natural habitat, and upsetting the balance of nature. Adams has no time for individual moments of human idiocy, best exemplified by his wonderful line skewering young Yemeni men who insist on wearing rhino tusk costume jewelry: “How do you persuade [them] that a rhino horn dagger is not a symbol of your manhood but a signal of the fact that you need such a symbol?” His exasperation is evident in this and other such pearls of prose.

I admit that I read this book more for Adams himself than for the subject matter. It is a credit to the author that by the end, I felt some sense of emotional investment in the animals, without the bitter feelings that usually emanate whenever I am subject to an overt tug at my heartstrings. Adams walks that fine line quite well.

And (yawn again) here’s why supplies are limited:

http://www.scientificamerican.com/article/how-the-ipcc-underestimated-climate-change/

Cheers.

And yet peer-reviewed grown-up research indicates that climate sensitivity to atmospheric CO2 has been over-estimated.

http://science.sciencemag.org/content/early/2011/11/22/science.1203513

And they’ve overestimated Antarctic melting.

http://climatechangedispatch.com/ipcc-author-antarctica-s-abrupt-glacial-melting-greatly-overestimated/

Yawn!! Groves’s Law: “Just as with proverbs, you can usually find plenty on the Web that contradicts anything else on the Web.”

The IPCC is a UN quango, not a scientific body, and certainly not an authority on anything. They have to take political considerations into account when making their projections, and they employ an army of cooks (called authors) that tend to spoil the broth, and as a result they repeatedly underestimate this, overestimate that, and make a total pig’s breakfast of the other.

Groves’s Law: “Just as with proverbs, you can usually find plenty on the Web that contradicts anything else on the Web.”

I agree. Hard to sort things out.

I don’t place very high reliance in Scientific American articles, after they wrote a few years about how we could transition to 100% renewables in some short time frame. They want to sell magazines.

Gail,

If you… “don’t place high reliance on Scientific American articles…They want to sell magazines”…

…then why did you quote from a Scientific American article in your first paragraph?:

“The Peak Oil story got some things right. Back in 1998, Colin Campbell and Jean Laherrère wrote an article published in Scientific American called, “The End of Cheap Oil.” In it they said:

Our analysis of the discovery and production of oil fields around the world suggests that within the next decade, the supply of conventional oil will be unable to keep up with demand.”

Good grief.

Cheers.

Gail wrote:

“…after they [Scientific American] wrote a few years about how we could transition…”

Is this 2009 article the one you’re referring to?

“A Plan to Power 100 Percent of the Planet with Renewables”

http://www.scientificamerican.com/article/a-path-to-sustainable-energy-by-2030/

If so, Scientific American did not “write” it.

Mark Jacobson and Mark Delucchi “wrote” it.

In fact, in a 2013 interview with Jacobson,

http://www.scientificamerican.com/article/how-to-power-the-world/

Mark Fischetti, senior editor at Scientific American, opens with this question:

“At first glance, your proposals to convert society wholesale to renewable energy, and relatively soon, sound wild. What kinds of reactions do you get?”

So Scientific American thinks the idea sounds “wild”.

Fischetti then asks about “obstacles”, “criticisms”, “challenges”, and “other concerns”.

He ends the interview with this:

“Given the radical nature of your proposals…”

And then questions the authors motivation:

“If you’re not an advocate [of Renewable Energy] what is your motivation? You’ve done this exercise three times now.”

So:

Scientific American prints a controversial energy plan, that it did not write, and does not endorse, written by an author who is later interviewed by Scientific American’s senior editor who thinks the idea sounds “wild”, and the proposal “radical”, then challenges the author on obstacles, criticisms and other concerns, and ends by questioning the author’s motivation.

It’s fair to say that Scientific American was highly skeptical about the whole plan, and by printing it, “sparked a debate” that completely, and deservedly, debunked it.

And… Scientific American wanted to sell magazines 18 years ago when the article you quoted approvingly of was printed, and it wanted to sell magazines when the article you disapproved of was printed.

We all have our preferences on the publications we “place high reliance on” and those we don’t. That’s our personal choice based on our personal reasons.

But it’s important to represent the position of those publications, and the authorship of their articles, clearly and honestly.

Scientific American did not write the 2009 article, as you claimed.

This fact materially changes your post. And thus changes, indeed obviates, mine.

If the 2009 article is not the one you referred to, then would appreciate a copy or an address for the correct one.

Thanks.

Cheers.

If so, Scientific American did not “write” it.

Mark Jacobson and Mark Delucchi “wrote” it.

The SA doesn’t “write” anything. Unless they have started to employ AI programs for the task, human beings ”write’ or ‘author’ everything that appears in SA. And I assume they gave up on employing clerks with quills to create the magazine pages quite a while ago.

The SA “printed” it. The SA “published” it. That’s what’s important. And in so doing they publicized, announced, reported, posted, communicated, imparted, broadcasted, transmitted, issued, put out, distributed, spread, promulgated, propagandized, disseminated, circulated, aired, blazoned, heralded, proclaimed it to the public—in association with their brand name.

Unless the SA printed and published it without an accompanying note stating that the decision to publish in no way amounted to an endorsement of the authors’ opinions or claims and that the magazine had reservations about such, then publication can be reasonably assumed to indicate the magazine’s approval of the article.

Moreover, articles of which the SA’s owners disapprove of or have reservations about do not get published in that magazine without a note clarifying the situation. The magazine does not lend its prestige to articles of which it disapproves.

Furthermore, the expression “ABC wrote X” is a perfectly acceptable equivalent way of saying “X was written in ABC”. The construction is commonly used to that end within the journalism industry. Arguably, anybody who wasn’t a pedantic troll out trying to cause trouble would interpret it as meaning precisely that.

Back in 1998, the Scientific American didn’t seem so focused on selling magazines. The thing that really got me upset was the article I wrote about at The Oil Drum, http://www.theoildrum.com/node/5939 back in 2009. It was about Scientific American’s so-called “Path to Sustainability.” I understand that the Scientific American has changed over the years. https://en.wikipedia.org/wiki/Scientific_American

Young Hawkeye makes yet another elementary mistake in logic.

Gail says she doesn’t place very high reliance on SA articles after they wrote a few years ago…. And the Hawk-eyed one asks in an accusing tone why she quoted from an article they published 18 years ago.

Duh!

SA was a great read up until about 1990. It was well worth buying for the Stephen Jay Gould columns alone. But like so many magazines it gradually declined in quality until it became irrelevant. As one former subscriber remarked, “They gave up being about science a long time ago. Thinner and thinner all the time, they have to fill the pages with CAGW crud and junk now. It’s been like seeing an old friend get dementia. Sad.”

In late november Laherrère wrote on the price, it’s in french but graphs are in english (pages 24 to 35, and 44):

http://aspofrance.viabloga.com/files/JL_Nice2015long.pdf

Some of his conclusions:

Since 2003, oil price is highly inverse to dollar value

Before 2003, M2 stock growth dragged dollar value; since 2003 dollar value drags M2 growth

In 2003, US oil costs and total debt hiked

The graphs are in English, so those are easy to read. Jean Laherrère is 85 years old, but he keeps working on this issue.

The mortality of all of us is 100%. If you didn’t think this was the case, you were fooled by the good times.

Collapse just brings this into sharper focus.

Most people are focused on something much smaller than the global situation. The world they perceive as “real” is the world of their local community or region. If they watch the TV, this may extend to their nation. The larger world where a lot of the food, fuel and other products they consume comes from is well over the horizon and therefore out of sight out of mind. Doubtless, they assume, the powers that be have everything in hand.

This is true of most people even if they are intellectually aware that the world they live on is a ball with a large but finite surface area and copious but finite amounts of natural resources. Emotionally, most of us are rooted in my home, my town, or my local province. My parents, for instance, were Londoners, and London was their world. Dad never travelled further than Brighton on the south coast and Mum only ever took two overseas trips in her latter years. I had an uncle who was a merchant seaman who sailed the world for many years. But even he remained a Londoner and what he experienced of the wider world consisted mainly of lots of ocean views, touristic scenes and sailors nights on the town. He didn’t look down on the whole thing and see the planet and our place on it in a holistic fashion like an engineer sees a factory or a systems analyst sees a computer operating system.

Thus, for most people, a form of secular providence reigns supreme in their subliminal belief systems. The idea that their society could collapse would never occur to them until, as in Venezuela, Ukraine, Syria and Yemen today, they are staring collapse in the face.

I know this from talking to many kinds people and also because I too am like most people in most respects.

Right, and in the face of collapse, people will hunker down which means their perception and world will get even smaller.

Another thing I find interesting about people: they will lie, and they can understand if other people are lying to them in small matters…but they don’t believe politicians or business people lie! They actually do believe the government is honest, the corporations are honest, the accounting is real, they are protecting our interests, etc!

It would never occur to an American, for example, that virtually every single person of big influence in America is lying to them. Rather, they will attack the person who tells them that. Witness how strongly you guys react against me, and you are fellow doomers.

I see the same thing. I take a psychological view of the effect. People have an internal model of the world. For each of us that internal model IS the world. When you tell someone a significant part of their world is not true they take it as a personal attack. They need to defend “the world”, at least their model of the world. A person to person lie on a local fact does not pose that same level of threat. It is not that people think the president can not lie they believe “the office of the president” can not lie because that meme has been embedded in them by society, tv, and the government school system.

Their are few people with the ability to do abstract thinking that challenges core emotional beliefs. At 58 I have learned I will not be changing peoples core beliefs. But I do enjoy the company of others who can see.

Dolph,

Agreed!

Witness how strongly you guys react against me, and you are fellow doomers.

At least they don’t call you a “denier” when you disagree with their dogma!

Ed,

When you tell someone a significant part of their world is not true they take it as a personal attack.

It’s a very common human trait. My mother got quite upset when as a teenager I told her that there was nothing truthful in the horoscope magazines she used to read. After a bit, she admitted astrology was probably bunk, but insisted it was a source of comfort to her and I shouldn’t try to take it away from her. I right little Rationalist Red Guard I used to be. 🙂

And this from yet another MSM source that is having a difficult time ignoring reality:

“QE Infinity: Are we heading into the unknown?”

http://www.cnbc.com/2016/08/26/qe-infinity-are-we-heading-into-the-unknown.html

“….Markets are currently riding on the wave of uncertainty and speculation over whether the world’s central banks will continue to pump in more and more cash into the economy…”

Well, markets are currently riding on a bubble in the bond market – a market which is three times larger -Trillions and Trillions larger – than all global stock markets combined.

Given that scale, if the pop of a dot com bubble (2000), or the pop of a housing bubble (2008) can cause deep recession, then what would a pop in the global bond bubble look like?

Maybe this is a scenario where the four horsemen awaken once again, perhaps for the last time, and begin to saddle up?

“….The problem is rising debt and monetary easing comes with many collateral effects…”

So beautifully understated. Oh, you mean like collapse of the global economy and the end of industrial civilization?

We are, no doubt, living in one of the most riveting times in human history.

Two quotes immediately come to mind:

“If something can’t go on forever, it won’t.”

– Herb Stein (CCE under Nixon and Ford)

“You can avoid reality, but you can’t avoid the consequences of reality.”

Ayn Rand (we all know who she is)

There’s another saying, “A group of people are only as healthy as the things it talks about…”

That’s good news for OFW readers: we might have a better measure of health than most, at least in awareness – and at least while the grid still works.

Cheers

Two lemmas ( mine — Interguru’s Lemmas )

1) They go on a lot longer than you think they can.

2) They stop suddenly without warning. Even those who see it coming have no idea when.

I am becoming ever more aware of the last part of your lemma, “Even those who see it coming have no idea when.”

2.1) They degrade with plenty of warning. Everybody will be suffering through the grueling process.

good stuff!

How’s this for a place to see off the end of the world… west coast of NZ…. spending a night in a nearby beach shack…. maybe I should haul my 20ft container and park it here 🙂

http://www.planitnz.com/assets/Uploads/West-Coast-Beach.jpg

Best idea of yours yet, Fast Eddie. Yes, haul it all there and wait and STAY there till the end! After all, avoiding to you its just a few months way….hehe

I like Eddys attitude. I will also start eating every christmas turkey like it is my last.

Those containers like to rust around the base of the steel corrugations. Pretty soon there will be salt water fountains at floor level.

For anyone interested in the role of geopolitics in the collapse of BAU and the unraveling of empire:

http://www.counterpunch.org/2016/08/25/the-broken-chessboard-brzezinski-gives-up-on-empire/

Read this book review by Mike Whitney in Counter Punch – and, if you have time, read the book. Would be interested in any thoughts our OFW friends here might have.

My take, in reading between the lines, is that it confirms the growing sense of impotence and desperation – and a whiff of fear when reality can no longer be easily ignored – in the imperial halls of power.

Or is this just a warmed over, updated version of pragmatic realpolitik?

Cheers.

Interesting article. From what I know, Iranian youth rather like America. More so, it seems, than any others in their region.

Military might and realpolitik aren’t always the best policy. The reset that Brzez envisages seems to require far more soft power and diplomacy than at any time. A very quick calibration to soft power and diplomacy might take traditional adversaries off guard. Speed is good. There’s still plenty of room to maneuver–working with religious organizations or non profits on the ground, etc.

It costs little, and probably is most practical to gear American grants to planning departments (which can be paid not to get in the way, at least) as well as other organizations that can promote small-group community planning. Each group tries to acquire a measure of self-sufficiency through small upgrading of water conservation and food production–like roof water catchment and soil building workshops, etc.. Small, coherent, universally distributed expenditures. Since they are the most concerned with the nurture of their families, women might be most receptive to such a plan.

But military might would be quietly reserved in the background. Walk softly but carry a big stick.

Book review? It’s a review of a ~3K word article

China is pushing the limits on urbanizatio:. Welcome to the “City Cluster”.

By any measure, Shanghai is one of the world’s biggest cities. It’s home to more than 24 million people. Its subway system is the longest ever built, extending to its rural limits. Crowds are so thick that burly “shovers” get paid to help pack the trains. Now the local government is saying enough is enough: Documents released this week reveal that Shanghai intends to admit a mere 800,000 new residents over the next 24 years, on its way to becoming an “excellent global city.”

A population cap on one of China’s most dynamic locales may seem impractical. But the government is actually thinking bigger: The plan envisions Shanghai as the high-end hub at the center of a massive “city cluster” comprising 30 urban areas — with a staggering total population of 50 million.

That might sound preposterous. But the Yangtze Delta Cluster, as it’s known, is one of at least 19 such projects in the works. The idea is to use an extensive hub-and-spoke rail system, much of it high-speed, to better integrate China’s burgeoning urban areas. The big three clusters — located along the Pearl River, the Yangtze River and the Beijing-Tianjin corridor — will each have 50 million people or more.

The effect could be transformative. For one thing, it will create the world’s biggest labor markets, and further urbanize a country that’s still more than 40 percent rural. It should boost economic growth and efficiency. And it could help solve a growing dilemma: Many of China’s biggest cities have simply reached their geographic and demographic limits.

https://www.bloomberg.com/view/articles/2016-08-25/how-big-can-china-s-cities-get

How much “stuff” would need to be imported into such a huge city cluster? How would road transport really work? This sounds like science fiction, but I suppose planners think this way.

LOL!

All I see is concentrated dieoff…

http://davecoop.net/senecagraph.gif

http://davecoop.net/seneca.htm

Above, are my latest guesses about the world oil-production situation.

Here’s an acronym for what drives a lot of this: MROMI, for “money return on money invested” — my guess is, MROMI considerations (not EROEI, or some such thing) are largely what drive oil-extraction companies (including such as ARAMCO).

With broad simplification, I think oil-extraction costs fall into two categories:

(A) the costs of keeping the existing wells/oilfields producing, &

(B) the costs of replacing those wells/oilfields, when they deplete

Though economic collapse may occur in different places at different times (EG, compare this “Silicon Valley”, where I am, where the water is pumped around, & mostly pumped in from afar, with electricity, with much of the world, where young folks carry the day’s water home), as someone (I think it was FE) wrote on OFW, “when the oil goes, the food goes”.

That’s part of why I think that the (A) costs will continue to get paid, if not the (B) costs.

Thanks! I agree that MROMI is a whole lot more important than EROEI.

One thing that confuses matters is that M includes growing debt, or lack of growing debt. Once banks cut off financing to oil companies, it seems like the game is over. Or worse yet, if banks fail, and it is not possible to pay employees of any kind of company, oil or otherwise.

Dave, you don’t really use your mromi concept to draw your graphs, don’t you? Rather an extrapolation of past production?

The team of scientists also used historical aerial photo analysis, soil and methane sampling, to quantify the strength of the “permafrost carbon feedback.”

Although the amount of gases being released from permafrost at the moment is “pretty small,” it’s thought that over the next 90 years, the levels of gas could be from 100 to 900 times greater than present measurements.

https://www.rt.com/viral/357224-permafrost-carbon-climate-change/

Pretty pretty … pretty … pretty … small

Other sources would have us believe the frozen muck will be melted by the end of summer…

Again — if AGW is the real deal — it ranks way down my list of concerns…. IBGYBG – I be gone you be gone in 90 years…….. actually everybody be gone….long before that

You maybe need to google a few sources. Cherry picking just amplifies your bias. Any googler can make themselves look like they are informed, maybe even seem intelligent. I don’t expect this post will pass inspection though.

Keep in mind Eddie that the attitude of “I don’t care, it won’t be here while I’m still alive” is a big part of what got us into the middle of this climate change and extinction mess in the first place. What I don’t understand is the ones who have kids. Apparently they don’t care about them either.

Tango Oscar, I accept that you are genuinely concerned about catastrophic climate change. But the big question is, what do you suggest we can do to prevent it?

As a denier, I feel no responsibility to do anything apart from to keep calm and carry on. But you, an alarmist, shouting “Fire” in our common global crowded cinema—a cinema apparently without exits—must feel some responsibility to do more than alerting other people to our impending doom. So what’s your plan for dousing the flames? What would you have the rest of us do?

“But the big question is, what do you suggest we can do to prevent it?”

I’ll give it a shot. The Earth receives about 1200 watts per square meter from the Sun, and has a current surplus of about 0.6 watts per square meter. That’s about 0.02% more energy coming in then going out. So all we need is a bit of dust, gas, particles, whatever in high atmosphere, preferably some kind that reflects visible light but not infrared, to just block out 0.02% of the sunlight.

Easy just place 400 satellites in orbit each 10 miles by 10 miles to block 0.02% of incoming sunlight. Aluminized Kevlar at 0.1mm thick (this is to get a back of the envelope number thicker than needed but accounting for other system components) weights 1.5g/cc or 0.015g/sqcm or 150g/sqm or 1.5E8g/sqkm or 1.5E5kg/sqkm. Gives 256*1.5E5 = 38E6 kg per satellite. At $4000/kg to medium earth orbit that is about 160 billion dollar per satellite or 64 trillion dollars for the whole constellation. Doable as a twenty year global project. Global warming problem solved.

I think you forgot to include this (sarc) 🙂

Won’t aluminized mylar bounce infrared back to Earth equal to the amount of sunlight it deflects? Like, a space / survival blanket works by reflecting your own body heat back to you, so …

I think just using balloons with variable displacement would work better, to lift loads up into the stratosphere and release the dust or whatever and then come back down to take the next load. Or partially deflate the balloons at max altitude and just let them fall back down slowly.

Maybe tactical nuclear war —- Nuclear Winter Lite?

Or perhaps we could spray 30 sunblock into the atmosphere on a daily basis?

https://www.rt.com/news/357230-belgium-chimay-sports-blast/

And the hits keep coming! Relentless… fear fear FEAR!!!!

What I am wondering is …. what impact does this have on tourism?

Of course my website http://www.strifetravel.com is prospering …. we have never had such awesome offers for so many destinations…

My other business of front-running the stock markets because I live in the future is also doing quite well… we make money every single day.

“because I live in the future”

Never mind the stock market. Tell us who wins the game of thrones. Then we can let this collapsing thing have its run.

Keep in mind I am only a few hours ahead… so my power to predict is quite limited…

“Tell us who wins the game of thrones.”

I think it is pretty obvious, winter wins and all the contenders die. Unless we get a cheesy ending where everyone unites to stop global cooling.

Yes, I am hoping for the silver wig, the dwarf and the bastard wins the throne halfway through the last episode. Then the snow zombies comes south, kills everyone. Then eternal winter.

Unusually normal summer in 2016 in Central Europe after the years of escalating temperatures: the climatologist Pavel Fasko says that we have returned 30 – 40 years back (article in Slovak)

http://kosice.korzar.sme.sk/c/20253739/v-kosiciach-a-presove-uz-mesiac-nebolo-ani-len-30-stupnov.html?ref=trz

Is it possible that the peaking coal consumption has its impact?

https://gailtheactuary.files.wordpress.com/2015/06/world-energy-consumption-by-part-of-world-2014.png

Well, we will see…

An article that starts out nicely, then peters out.

http://www.aljazeera.com/indepth/opinion/2016/08/economic-system-21st-century-160819134542550.html

Towards a new economic system for the 21st century

The new economic system should be based on localised forms of industry, finance and participatory democracy.

I didn’t get past the headline because I started to hear this song playing in my head… don’t you hate when that happens!!! It really can drive one around the bend…

“An article that starts out nicely, then peters out.”

Why? Because it’s completely delusional, the writer ends up in a cul-de-sac of illogical thinking, and deep down knows it. Airy fairy talk about “consciousness shifts” and “young people taking up the vanguard of revolutionary struggle”, or “new ways to restart production and consumption by other means “new economy” are laughable, for all the reasons we’ve spoken about ad nauseum, on this blog.

It must be difficult to maintain a line of thought as a journalist who is ordered to write something based on an edict issued from the Ministry of Truth … when you know what you are writing is total nonsense…..

You of course spew something out — a series of disjointed thoughts — bordering on gibberish…. hoping the editor will accept it….. because you need to eat….

An article filled with the audacity of hope. It put me in mind of this catchy little ditty.

https://youtu.be/FjtEYt6l2Cs

Ha ha ha ha …. and what would a Hoper Party be without this classic (and organic granola…)

Imagine no possessions. The way things are going, quite soon we might not need to imagine that. But in the meantime, let’s calm ourselves with the mantra,” Nothing’s gonna change my world!”

Imagine there are no people… they’ve mostly starved and died…. and the rest succumbed to radiation poisoning…. it’s easy if you try…..

If that version isn’t working:

https://youtu.be/XcsflKHiKlo

He took on the Bernie New Deal approach, which was intriguing. But didn’t explain why it couldn’t work (which would have been helpful for millions of those “new young revolutionaries”). Then he abandoned the discussion entirely thereafter.

That was four minutes of my life I will not get back.

Hey, how come my comments are always awaiting moderation nowadays?

Could you be using any words that are on the naughty list?

Or could you be putting too many page breaks or links in the comments?

I don’t know what words are on the list or what the limits are, but shorter posts seem to have less trouble getting posted immediately.

Like “nazi”, “gun” or “Hillary Clinton”? 😀

If you use “conspiracy theory” and “Fast Eddy” in the same sentence you get moderated.

Lol!

The things you see when you haven’t got a gun…

Climate Change Is Making This Portable Air Conditioner a Must-Have Summer Accessory

https://i.kinja-img.com/gawker-media/image/upload/s–ag_ccKev–/c_fit,fl_progressive,q_80,w_470/scnspmha4kvdnpzcsolu.jpg

Sunglasses, swimsuits, tank tops, and sandals are the usual accessories you think of when you’re getting ready for summer. But with climate change pushing summer temps higher and higher ever year, it’s probably not a bad idea to add the Zero Breeze portable battery-powered air conditioner to that list.

Wow! Another way to justify using more energy resources now!

Why not use a coal powerplant to power a wind turbine with refrigerated blades. And voila A nice and cool breeze on lull days.

Am I fiendishly clever or what? 😉

https://wattsupwiththat.files.wordpress.com/2016/01/de-icing-wind-turbine.jpg

Give that man a cigar!

https://3.bp.blogspot.com/-0w4UU92om-0/V5nFQ1rmtrI/AAAAAAAC-AM/Ddxx9FsG5aY3EgAtGorEvDcRMiPC3CjnACLcB/s1600/won%2527t%2Byou%2Bbe%2Bmy%2Bhumidor.jpg

Radiant Technologies TM has the answer!

A spent fuel rod in every turbine blade would kill the de-icing problem stone dead.

As an added advantage, it would make the blades glow in the dark allowing owls and low-flying airplanes to avoid hitting the things.

http://www.bloomberg.com/news/articles/2014-07-11/dubai-to-build-the-first-air-conditioned-mini-city

http://www.bloomberg.com/news/articles/2016-01-10/dubai-real-estate-reality-check-felt-by-20-billion-developer

I suppose this is as good a way as any of raising debt levels, and demand for fossil fuels. I expect it will end in debt default problems.

IRRC, there was an earlier Dubai project that had a problem with debt a few years ago, but recently got out–the island project in the form of a big tree.

If I had any doubts left, I’m now certain: we deserve what we have coming.

“Assuming by BAU you mean 3 – and this is where Laetititia’s observations come in – transition to a post-consumerist economy, based on the smaller energy surplus that renewables can provide, may be feasible.”

https://surplusenergyeconomics.wordpress.com/2016/08/13/76-the-point-of-no-returns/?replytocom=2337#respond

This is what happens when you write a book and want people to guy it….

” The link between population and energy availability is incontrovertible, and is discussed in my book…

Adjusting the economy downwards could be traumatic – adjusting population downwards would surely be brutal.” – drtimmorgan

That should help book sales in DelusiSTAN.

And it makes sense to focus on that population — because if the book were written to appeal to RealitySTAN residents …. it might sell a dozen copies.

Norman – do you reckon that is accurate?

(Jackson Hole Wy) Conferees at the Jackson Hole Economic Symposium were startled when a middle-aged man forced his way past security and barged into the main conference hall shouting “You’re doomed. All of you! BAU will end and you will be dead. Dead.”

Symposium security guards quickly overcame the slightly built intruder and ejected him bodily out of the hall and into the street where he was taken into custody by Wyoming State Police. Calls to the FBI revealed the man to be a possibly deranged New Zealand citizen who has claimed to have a gift of prophecy in predicting the end of the world. State Police spokesmen said that FBI inquiries indicated that “Fast Eddy” apparently posed no security threat and is mainly interested in publicity. Troopers escorted the man to the town limits and warned him to stay out of town or else.

The man was last seen weaving around outside a local cowboy bar and annoying passerby with shouts of “Hey I’m Fast Eddy. C’mere and let me tell you a story about the end of the world” but getting few takers.

Fed Chief Janet Yellen was not present during the incident and presented her keynote address at 1:00pm as scheduled and without interruption.

I’m typing this from a cell in Jackson Hole….

Tiffany & Co revenue fell 5.9 percent to $931.6 million, missing analysts’ $933.9 million estimate. Comparable-store sales fell 9 percent, excluding the effects of currency fluctuations. Analysts projected a 7.1 percent drop, according to the average of estimates compiled by Consensus Metrix.

The same-store sales disappointments were centered in the Americas and Japan.

In the Americas, they dropped 9 percent. Analysts estimated a 7.8 percent decline.

In Asia-Pacific, they slipped 9 percent. Analysts estimated a 11.4 percent drop.

In Europe, they fell 13 percent. Analysts estimated a 13.6 percent decline.

In Japan, they were down 3 percent. Analysts estimated a 1.8 percent gain.

http://www.bloomberg.com/news/articles/2016-08-25/tiffany-sales-miss-estimates-as-global-uncertainty-hurts-demand

The and other corps are cutting expenses to the bone …. how do we not have mega layoffs?

Update: police say that upon questioning, Fast Eddy would only repeat over and over, “there will be no Christmas turkey for you.”

I didn’t do nuthin wrong!

FE– any sighting of Oil Slick Dick Cheney?

It is part of that Jackson elite, who like a non stirred stew, has had the scum rise to the top.

(That’s why both stews and society needs to be stirred frequently)

HT- Abbey

The world has become a giant cargo cult. The people are gathered in the parks, praying for black helicopters (or any other color) fly over and drop money on them like mana from heaven or the rain that falls after a long drought. If we listen hard enough, we may hear the whining of the choppers in the distance as they approach us loaded with pallets of nice, fresh, crisp greenbacks, euros and yens. Once they’re dropped, all we have to do is go out and spend them and salvation is at hand.

On August 25, 2016 at 3:10 Fast Eddy was able to – from his cell – create and market $1 billion in negative interest bonds. Those bonds pay him 1% per year, and so with his first interest check he was able to bribe the judge, and get released.

Knowing that the end is nigh and having a few bucks in his pocket is a well known sign that FE is going to PARTAAAIA, and he has not been seen since … though he still is posting on OFW.

And from Bloomberg:

“Mobius says helicopter money will be Japan’s next big experiment”