Many people have the impression that recessions come from financial missteps, such as the US subprime loan fiasco. If energy is involved at all, the problem comes from high oil prices as supply becomes inadequate to meet demand.

The real situation is different. We already seem to be on the road toward a new crisis; this crisis is likely to be much worse than the Great Recession of 2008-2009. This time, a major problem is likely to be energy prices that are too low for producers. Last time, a major problem was oil prices that were too high for consumers. The problem is different, but it is in some ways symmetric.

Last time, the United States seemed to be the epicenter; this time, my analysis indicates China is likely to be the epicenter. Last time, the world economy was coming off a high growth period; this time, the world economy is already somewhat depressed, even before hitting headwinds. These differences, plus the strange physics-based way that the world economy is organized, explain why the outcome seems likely to be worse this time than in 2008-2009.

I recently explained what I see as happening in a presentation for actuaries: Recession Likely: Expect a Bend in Trend Lines. This post is based on this presentation, omitting the strictly insurance-related portions.

The big thing that the vast majority of people do not understand is how important energy is to the economy. Because of this issue, I started my presentation with this slide:

Slide 3

After an opportunity for discussion, I offered the explanation that the role of food for humans is very much parallel to the need for energy of various types for the world economy. Food provides people with the energy required if they are to have the ability to think, move and speak. Energy products of many kinds enable the activities that we associate with GDP. For example, energy consumption enables machinery to operate and goods to be transported.

Slide 4 – Larger image at this link.

Using data from Smil, as well as more recent BP data, we can estimate how fast energy consumption has been growing over a very long period–nearly 200 years. We can see that the highest energy consumption growth occurred in the 1961 to 1970 period; the second highest growth occurred in the 1951 to 1960 period. These are periods we associate with rapid GDP growth and prosperity.

On the next slide, I show the same data displayed in a different way.

Slide 5 – Larger image at this link.

On this slide, I make two changes in the way the data are displayed:

- The increases in energy consumption are split into two components: (a) energy used to support population growth and (b) all other, which I describe as energy used to support improvement in “living standards.”

- A different graphing approach is used.

Note that when population growth corresponds to the full amount of energy consumption growth (in other words, at times when there is no red area above the blue area), energy consumption per capita is flat. High growth in energy consumption per capita seems to correspond to rising living standards, as occurred in the 1950s and 1960s.

While I label the “all other” category as if it is simply changes in living standards, there are other components, as well. One breakdown might be the following:

- True improvement in living standards.

- Additional energy investments required to offset diminishing returns.

- Increasing use of energy for overhead items that don’t get back to individuals, such as energy used to fight pollution or to allow globalization.

- Efficiency improvements allowing available energy to be more productive.

Efficiency improvements (Item 4) will allow more energy to be available for improvement in living standards, while Items 2 and 3 in the above list act in the opposite direction. We do not know to what extent these items really offset each other. Thus, “All other” = “Improvement in Living Standards” is only a rough approximation.

Slide 6 – Larger image at this link.

We can see from Slide 6 that whenever there is no red area above the blue area (flat living standards or flat energy per capita), adverse events seem to happen.

For example, the US Civil War (1861-1865) came at a time of low energy consumption growth. The Great Depression of the 1930s came during another period of low energy consumption per capita growth. World War I came at the beginning of this period, and World War II came at the end. The collapse of the central government of the Soviet Union in 1991 ushered in a decade of low world energy consumption growth, in part because of the loss of the central currency of the Soviet Union.

The “China Coal” note at the end pertains to the way that China and its coal supply has helped pull the world economy forward since 2001. This benefit seems to be already declining.

Slide 7 – Larger image at this link.

Slide 7 shows China’s energy production by fuel. Coal production (in red) soared after China was added to the World Trade Organization in December 2001. Beginning about 2012, China’s coal production began to plateau. Depleting mines and low prices for coal have kept production flat. Imports can be used as substitutes, to some extent, but it is difficult to keep costs low enough and provide adequate total supply.

With the loss of growth in China’s coal production, its economy has had to cut back. Each year, we read about coal mine closures and miners needing to find new jobs. We know that China discontinued its paper and plastic recycling business as of January 1, 2018. China has also been cutting back on solar subsidies, leading to fewer jobs installing solar panels. All of these types of changes reduce the number of people who can afford to buy high-priced goods, such as new homes, vehicles and smart phones.

Slide 8 – Larger image at this link.

It is becoming increasingly clear that China is being forced to cut back on heavy industrialization because of its coal difficulties. Slide 8 shows automobile purchases for six large economies. China is by far the largest of these economies in terms of auto sales. China’s auto sales began to slide in 2018 and are sliding further in 2019 (about -11%).

If we look back at the time of the 2008-2009 recession, we see that auto sales of the US dropped precipitously. The United States was the country that led the world into recession. The inability of US citizens to buy cars was a sign that something was seriously wrong. Now we are seeing a similar pattern in China.

China has reported that its GDP growth rate has been slightly lower during 2019, but we really don’t know how much lower. The amounts it publishes are too “smooth” to be believed. The actual GDP growth rate is believed to be lower than the recently reported 6.0%, but no one knows by precisely how much.

Figure 8b – CNBC Chart of changes in auto sales by country, based on data through October 2019. (Not part of original presentation.) Source

Figure 8b gives a little more information about recent car sales by country. We can see from this chart that based on data through October 2019, world automobile sales are expected to fall by about the same percentage (3%) in 2019 as during the recession year of 2008. I find this disturbing.

We can also see the huge impact that China has had on keeping world private passenger auto sales rising. The world economy looked like it was headed into recession in January, 2016, when world oil prices were very low, but a spike in China’s automobile sales at that time helped keep total world automobile sales rising and allowed world oil prices to rise from their low point.

In the next sections, I provide some background regarding this story.

Slide 9

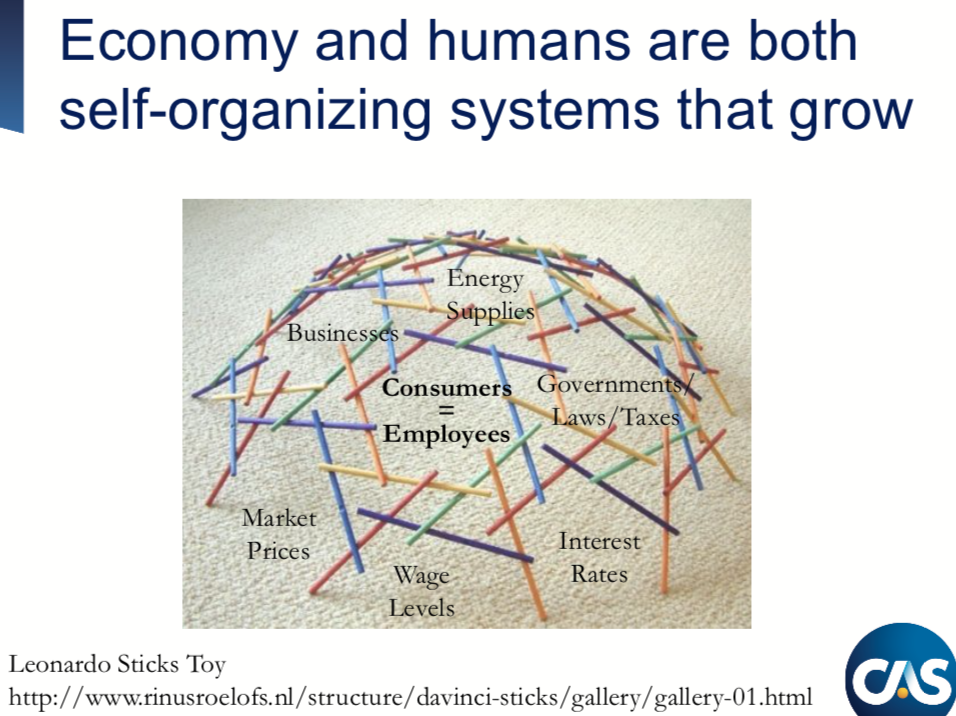

Slide 10 – Larger image at this link.

Slide 10 shows the way that I visualize the world economy self-organizing and growing. The economy grows by adding new “layers” of businesses, products, consumers and laws. Unneeded products, such as buggy whips, are dropped from the bottom. Unprofitable businesses close. In some sense, the economy is hollow because of these deletions. It cannot easily go backward because, for example, the support services for widespread use of transport using horses are lacking.

Energy is used to operate all aspects of the system. One part of the system is a self-organizing financial system that helps decide, through wage levels, who gets the benefit of the goods and services that are made. This financial system includes self-organizing interest rates and self-organizing commodity prices.

The most important connection within the economy is the one I show at the center as “Consumers = Employees.” Consumers are very dependent on their wages as employees. If the economy is to continue to operate, workers must receive high enough wages to purchase the goods and services the economy produces. Even the lower-paid workers need to be able to afford food, housing and transportation, or the economy will tend to collapse.

Slide 11

When we look back through the history on Slides 4, 5 and 6, we see that the growth of energy consumption is very important in how economies operate. The theories of Ilya Prigogine explain why this is the case; when adequate flows of energy are available, self-organizing systems are able to grow.

Few economists today include energy consumption in their models, however. Economic theory has grown over time in its own “ivory tower.” Like other academic subjects, it depends on early theories and the process of peer review. The views expressed must also be pleasing to those in power, who would like everyone to believe that politicians, rather than the laws of physics, are in charge.

Slide 12

There are many types of self-organizing systems that grow. They all, directly or indirectly, require energy. Plants and animals of all types are self-organizing systems that grow. Hurricanes grow using the energy that they get from warm water.

Governments grow from the tax revenue that they are able to collect; they use the revenue to buy energy products such as electricity to operate governmental offices, oil to build roads and operate police cars, and natural gas to heat buildings.

The Internet grows through the revenue collected to provide its services. The Internet uses revenue to buy computers (made with energy products) and electricity to operate those computers.

Slice 13

Nearly all 0f the energy we use is hidden. For example, modern food production is very much dependent on energy consumption. Agricultural machines are made using energy products. Soil amendments, including organic soil amendments, are transported using fossil fuel energy. Refrigeration is possible through the use of energy. Hybrid seeds are only possible through energy consumption. Planting seeds by digging with a stick would only use human energy, but such a process would be terribly inefficient.

Slide 14

Slide 15

Most of us can easily recognize today’s goods and services, such as those listed.

Slide 16

Promises of future goods and services act like promises of future energy supplies. This happens because creating goods and services that people can actually use requires energy supplies of the appropriate type.

When people get cash or a check, they expect to use it to buy goods and services. Creating these goods and services requires energy consumption. If there is no energy of the right type available, the goods and services won’t be available to fulfill the promises.

Slide 17 – Larger image at this link.

Promises of future goods and services tend to grow faster than actual goods and services because it is these promises that, in some sense, “pull the economy along.” For example, if a young person gets a loan, (s)he can often buy a new car. The fact that a new car is being purchased leads to more jobs in the supply line leading up to new car production. Or, if a business takes out a loan or sells shares of stock, it can use the proceeds to hire employees. It is these growing wages that keep the system operating.

As long as the economy is growing rapidly, the mismatch between growing debt and actual output doesn’t become apparent. As the economy slows, some workers find themselves working fewer hours. Some businesses become less profitable and lay off workers to try to restore profitability. The catch is, with fewer workers, the economy slows even more. It usually takes more debt, at lower interest rates, to get out of such an economic slowdown.

Slide 18

Slide 19

There is a lot of confusion about prices. “Demand” is what people, through their wages and debt, can afford. As economists tell us, price depends on supply and demand.

In the short term, prices tend to bounce around a lot. The short term buyers of oil are oil refineries. They need to keep their employees busy. If they see a shortage of oil, they may bid up the price of oil to allow their workers to continue to be employed.

Over the longer term, prices of all energy products tend to depend on consumers’ ability to afford finished products, like cars, homes and cell phones. Producing these objects and shipping them takes energy. They also use energy as they operate.

Slide 20 – Larger image at this link.

The various energy prices shown here are simply a few of the many, many energy prices that we see around the world. Strangely enough, prices of all energy products tend to fluctuate together, over the longer term. Prices depend on affordability of end products, such as cars, homes, computers, food and clothing. Our problem since about 2012 has been lack of affordability of end products.

The primary way of raising affordability is by increasing productivity. Increased productivity is made possible by increasingly leveraging human labor with devices that are built with energy and are operated using energy. For example, a worker with a ditch digging machine is much more productive than a ditch digger with only a shovel. An analyst is more productive with a computer and Internet access than with only pencil and paper.

With higher productivity, more goods are produced in total. As long as not too much of this productive output is skimmed off the top (by governments, or by business hierarchy, or to pay for the devices and their fuel), it is possible for each worker to afford more goods and services, raising total demand.

An alternative way of raising affordability is by adding more debt at ever-lower interest rates. This approach tends to make goods such as cars, homes, and factories appear more affordable because their monthly payments are lower. This added-debt approach only works as long as the economy is growing quickly enough. If the economy slows too much, the added debt leads to financial crashes of many types.

Slide 21

Slide 22

Many people think that they know the amount of oil that can be extracted based on the current technology and the assumption that prices will eventually rise high enough to extract all of the fossil fuels that seem to be available. For example, the International Energy Agency has prepared reports in which it shows expected oil availability if oil prices rise to $300 per barrel.

The catch is that even if oil prices can bounce high, it is not clear that they can stay very high. The current price of oil is only in the $55 to $65 per barrel range. A price of $300 per barrel will allow oil extraction using very advanced technology. We don’t have any evidence that oil prices can stay this high because demand comes primarily from wages. Prices cannot stay high without adequate support from wage levels.

Of course, the issue is not just oil prices staying sufficiently high. Natural gas, coal, uranium and electricity prices all have difficulty rising high enough and staying high enough. Commodity prices such as copper and steel have the same issue.

Slide 23

There are many people who say, “Of course, oil prices will rise. Oil is a necessity.” They forget that it is really a two way tug of war between producers getting a high enough price to be profitable and consumers getting a low enough price to be affordable. There will be a winner and a loser.

People also forget that most commodity use is hidden. We see the fuel we buy for our personal vehicles, but there are a huge quantity of oil products required for shipping goods, paving roads, growing food, and for many other uses that we are not aware of. While we might be able to pay a little more to fill our gasoline tank, most of us would not be able to simultaneously pay more for food, transported goods of all kinds and road maintenance.

Slide 24 – Larger image at this link.

Economists often assume that if energy prices rise, wages will rise, as well. If we look at the data historically, however, it doesn’t work that way at all. What happens is the opposite: average wages tend to rise as long as oil prices stay low. Once oil prices spike, average wages tend to flatten out.

The amounts shown on Slide 24 are average wages, computed by taking the total inflation-adjusted wages for the population in total and dividing by population. When oil prices spike, recession soon sets in. The reason why average wages fall is partly because more people become unemployed. Other workers find it necessary to accept lower-paying jobs.

Slide 25 – Larger image at this link.

Many people focus on the run-up in oil prices to July 2008. An equally important point is the fact that the world economy has not been able to maintain these high prices since July 2008. The general price trend has been downward. The cuts by OPEC have not had a material impact.

Slide 26

Citizens of the United States, Europe, and Japan are used to thinking of high energy prices as being a problem because they are from countries that require substantial imported energy to maintain their GDP. For example, Greece will sell fewer trips on its tour boats, if oil prices are high. This will have an adverse impact on employment and the ability to repay debt with interest.

If a country is an oil exporting country, low oil prices are an even worse problem. This happens because oil exporting countries tend to earn a large share of their revenue from taxes on the sale of oil. These taxes can be much higher if oil is selling for, say, $120 per barrel than if it is selling for $60 per barrel. These tax dollars are used to provide subsidies to offset the high cost of imported food. They are also used to build industry and infrastructure to provide employment to the population.

If oil prices are too low, oil exporting countries will tend to cut back on oil production. In fact, this has been happening for OPEC for the entire year of 2019.

Similar problems occur if commodity prices of any kind (coal, natural gas, uranium, steel, copper, etc.) stay too low for an extended period. Producers go bankrupt, or they stop production, or they pay their employees so poorly that the employees go on strike. Sometimes, they may even start rioting. Many of the riots around the world today are related to low commodity prices.

Slide 27

Slide 28 – Larger image at this link.

The world experienced spiking oil prices in the period leading up to mid-2008. These high prices caused a recession and much lower prices followed. The chart on Slide 28 gives a somewhat exaggerated view of what goes wrong with high oil prices.

If the price of oil suddenly spikes to two or three times its previous price, both the price of food and gasoline are likely to increase. This change tends to lead to a big shift in a family’s budget. Debt payments, such as for a home and car, are pretty much fixed, so the big increase in food and gasoline prices must be taken out of the budget earmarked for everything else. This leads to cutbacks in discretionary spending such as vacations, restaurant meals, and charitable contributions.

In a short time, there are layoffs in discretionary sectors. Those who are laid off are more prone to defaults on loan payments. The problem soon escalates to a recession, with high unemployment and low oil prices.

Slide 29

Strangely enough, central banks push back against high oil prices as well. They know that high oil prices lead to high food prices. Citizens of energy-importing countries will be unhappy with elected officials if oil and food prices rise. Thus, central banks tend to raise short-term interest rates, as soon as they become concerned about high oil and food prices.

The recession that follows will quickly bring food and energy prices back down. If food and energy prices fall, the low prices will be the problem of the energy producers. Oil exporters will find their tax revenue too low, but the high-price problem of oil importers will be gone.

Figure 29b- Slide from a different presentation, showing the trend in interest rates. Larger image at this link.

You will recall that the rapid energy consumption growth periods were 1961 to 1970 and 1951 to 1960. During these periods, the economy was growing almost too quickly. The Federal Reserve was able to keep raising interest rates, as a way of holding down economic growth. It was not until 1981 that the pattern changed from raising interest rates to falling interest rates.

Since 1981, the US Federal Reserve and other central banks have been reducing interest rates. Lowering interest rates and rising debt levels, as mentioned previously, makes goods appear more affordable because of lower monthly payments. The concern now is that interest rates are about as low as they can go. Central banks no longer have room to offset recessionary tendencies (because of slow growth in energy consumption) by lowering short-term interest rates.

Slide 30

Most people never consider the possibility of low energy prices leading to collapse. It looks to me like this is the danger facing us today. Let’s start by looking back at what happened in 1991.

Slide 31 – Larger image at this link.

When the central government of the Soviet Union collapsed in 1991, the individual republics making up the Soviet Union were left on their own to find new currencies and new trading partners. Satellite countries of the Soviet Union were affected as well. Slide 31 shows that the consumption of many types of resources dropped for many years for the whole area. The low point was not reached until 1998.

Slide 32 -Larger image at this link.

If we look back to see what had happened previously, the Soviet Union was an oil producer and exporter. When oil prices were high in the 1973 to 1980 period, the Soviet Union prospered. But then low prices came along, at least partly because the US Federal Reserve raised interest rates to almost 20% in the 1980-1981 period. (See Figure 29b.)

The long-term low oil prices, in some sense, indicated that the world economy was producing too much oil; some inefficient area(s) of production needed to leave. The Soviet Union may have been singled out by the self-organizing economy because it used energy products in a less efficient manner than other economies. Its adverse outcome may also have reflected the fact that its cost of production was higher, leaving less of the sale price for reinvestment and taxes.

Slide 33

The Soviet Union is an example of what can happen if oil prices stay too low for several years. The central government of such an economy can collapse.

Slide 34

When commodity prices are too low, the economies of countries exporting those commodities are stressed. This is why we see so many uprisings in commodity-producing countries right now. Iraq with its oil has been having protests. Chile, with its copper and lithium exports, has been seeing protests. South Africa with its exports of coal, precious metals and gems has been having riots. With some escalation, any of these low-price situations could lead to an overturned government.

Slide 35

Slide 36

In Slide 36, I give an example of two different kinds of ingredients in a cake:

- Ones that are substitutable: the flavoring, which can be vanilla, almond, or something else

- Ones that are not substitutable: the flour, which is the energy product

With too small a quantity of flour, all we can do is make a smaller cake. Perhaps we can substitute a different energy product, but electricity most certainly will not do! Some bacteria eat electricity, but humans do not. Substitutability is limited, even within energy products/carriers.

Economists make models focusing on the special case when a material is not essential for the economy. This gives a misleading impression. If they had looked back at what happened when energy supplies were low relative to population growth, as we saw on Slide 6, they could make much better models.

Slide 37

We seem to be sitting on the edge of some form of collapse for at least parts of the world economy, right now.

Without enough energy consumption growth, top-level organizations, such as the European Union, the United Nations and the World Trade Organization, are especially at risk of collapse.

Slide 38

Slide 39

One of our big problems today is excessive wage disparity. High-wage workers rarely have trouble being able to afford homes, cars, vacations, and air conditioning. It is non-elite workers, the ones who have not been able to find high-paying jobs, who have an affordability problem.

The wage disparity problem is an outgrowth of how the physics of the economy works. If there are not enough goods and services to go around, the physics of the economy effectively “freezes out” some of the workers. Under this arrangement, there will be some survivors even if there is not quite enough for everyone. In some sense, the “best adapted” are able to survive. If the inadequate supply of finished goods and services were spread around evenly, there might be no survivors at all.

Slide 41

The thing that is key is that workers need to be able to afford finished goods and services produced by the economy. If too large a share of wages goes to high paid workers, or to owners of robots, there is not enough left over for the “regular” employees.

Slide 42

Many workers have seen their jobs disappear as their employers moved production to another country where wages were lower. Or, jobs can remain, but the wages will fall from the low-wage competition.

Slide 43

US income disparity seems to be as great as it was in about 1930, at the time of the Great Depression.

Slide 44

Slide 45 -Larger image at this link.

If we look at historical world energy consumption by fuel, we observe that it has been rising the vast majority of the time. The little dip that we see about 2008-2009 occurred at the time of the Great Recession. It doesn’t take much of a cutback in energy consumption to cause a major problem.

Back at Slide 20, I remarked,

The primary way of raising affordability is by increasing productivity. Increased productivity is made possible by increasingly leveraging human labor with devices that are built with energy and are operated using energy.

The world economy requires growing energy supply, of suitable kinds, to operate. If the quantity of energy available is reduced, productivity is likely to nosedive. This is true even if the reduction is intentional and seems to be for a good cause, such as reducing CO2 emissions.

We seem to be heading for a contraction in energy supplies now because of continued low energy prices. Fossil fuels are, in some sense, leaving us, whether we like it or not. World coal production has been flat to falling since 2012. IPCC scenarios assume a very different pattern: Fossil fuel use, especially coal, will grow indefinitely, presumably because of high prices and improved technology.

Many people are hoping that wind, solar, and hydroelectric will someday replace fossil fuels. I consider this highly unlikely because all three are made using fossil fuels. Furthermore, these “renewables” in total represented only 10% of world energy supply in 2018. The 10% is divided as follows: wind, 2%; solar, 1% and hydroelectric 7%.

Slide 46 – Larger image at this link.

There clearly is a correlation between GDP growth and energy consumption growth. China with its growing coal use was pulling the world economy along, especially in the 2002 to 2012 period. Recently, it has lost much of this ability.

In my opinion, Trump’s tariffs are not the cause of our current trade problems. Tariffs seem to be enacted whenever growth in energy consumption per capita is very low. Tariffs were enacted both immediately before the US Civil War and at the time of the Great Depression. The problem is that jobs that pay well indirectly require significant energy consumption. When growth in energy consumption per capita is low, it becomes impossible to find enough jobs that pay well for everyone. Tariffs are used in an attempt to keep jobs that pay well at home.

Slide 47

We don’t know quite what will happen. The closest analogy is the Great Depression of the 1930s. More financial problems seem likely. In fact, they could escalate quite quickly. More strikes, such as those currently going on in France, seem likely. The situation is likely to play out a little differently in various countries.

The physics of the situation seems to try to keep some parts of the system operating, if at all possible. But, as mentioned at Slide 10, the self-organizing system deletes parts of the economy that are no longer needed. We no longer have an economy that can operate with horse and buggy, for example. We can’t just “go backwards” to an economy of an earlier era.

Slide 48

We are already seeing changes in this direction. Hong Kong’s protests are in the news practically daily. Germany is experiencing job layoffs. We know that in an interconnected world, a recession that starts in one large country is likely to eventually affect much of the rest of the world.

Now we are in a waiting period, waiting to see what happens next. Major changes seem likely over the next five years, but they could happen much sooner.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Do I send a TREND here?

(Bloomberg) — The world’s youngest prime minister needs to act quickly to tackle one of Europe’s fastest-aging populations.

https://news.yahoo.com/finland-pm-urged-address-risks-080000076.html

Finland’s central bank said on Tuesday that the burden on public finances, as more people head for retirement, is unsustainable and requires a political response. The warning comes just days after 34-year-old Prime Minister Sanna Marin took office.

The so-called sustainability gap — which measures the difference between spending and income — has widened to 4.7% relative to gross domestic product, from about 3% a year ago, the Bank of Finland said in a report on Tuesday. The biggest contributors to the increase are cooling growth, higher government borrowing and political stalling over health and welfare reform.

According to the European Commission, the sustainability gap poses a significant risk to the long-term health of public finances when it exceeds 6%, while a reading of under 2% denotes low risk.

“One factor currently weighing on the long-term outlook for the public finances is the fact that the baby-boom generation has reached retirement age,” the central bank said. “This has increased public pension expenditure, and over the next few years it will also lead to a more rapid increase in expenditure on health care and long-term care of the elderly.

OK BOOMER…keep feeling until you drop…..and no unlimited health care for you!

There will be a lot of countries in this position, I am afraid.

“…thousands rallied at the weekend in [Thailand’s] biggest demonstration since a 2014 coup… Saturday’s peaceful rally was a reminder of the tension that is building again rapidly between the establishment and those seeking change.”

https://www.bangkokpost.com/thailand/politics/1817299/from-tweet-to-street-new-thai-generation-joins-protest

“…the [Thai] central bank is happy. But there are clear signs of production market struggles as the sector keeps producing fewer goods and services. Manufacturers aren’t happy.

“All three markets — financial, product and labour — are interconnected to form the economic cycle. When one market breaks down, the whole economy collapses.”

https://www.bangkokpost.com/opinion/opinion/1808969/the-vicious-economic-cycle-has-begun

“Domestic car sales contracted for a sixth straight month in November, slumping 16.2% from a year earlier to 79,299 vehicles, hit by stricter lending by banks, the Federation of Thai Industries said on Wednesday. In October, sales were down 11.3% from a year earlier.”

https://www.bangkokpost.com/business/1818879/slump-in-domestic-car-sales

I didn’t realize that Thailand was doing poorly as well. Stricter lending by banks creates a problem.

“The biggest television broadcaster in Hong Kong is cutting staff as the city plunges into recession and its political crisis continues with “no sign of abating,” the company’s CEO told workers this week.”

https://edition.cnn.com/2019/12/17/media/tvb-layoff-hong-kong-protests/index.html

“Hong Kong‘s economy ends the year wounded, with the chances for stabilization in 2020 hanging on whether future protests are peaceful or lapse back into violence.”

https://www.bloomberg.com/news/articles/2019-12-16/hong-kong-s-economy-limps-into-2020-with-fate-tied-to-protests

“A Bank of England committee for financial policy underlined global risks linked to Hong Kong’s political tensions which led to about $5 billion in capital outflows from investment funds. The figure amounts to around 1.25 percent of Hong Kong’s GDP, the BoE said.”

https://www.finews.asia/finance/30510-boe-5-billion-in-protest-linked-fund-outflows-from-hong-kong

“Protests in Uzbekistan are a rare event given the country’s authoritarian history… [but] small public protests are emerging.

“The majority of public protests so far have been tied to temperature drops. As the temperature dropped, so did the patience of people unable to satisfy their basic needs for electricity and natural gas…

“In 2019, Uzbekistan’s energy and natural gas systems yet again were put to the test as winter set in. The protests reveal that the government is unable to deliver basic utility services or handle normal complaints to satisfaction. Taking to the streets is a last resort.”

https://thediplomat.com/2019/12/what-recent-protests-in-uzbekistan-really-tell-us/

“At least 304 people were killed and thousands more injured during anti-government protests across Iran last month, according to Amnesty International…

“Nationwide protests broke in dozens of cities across Iran last month after the government suddenly hiked the price of fuel overnight.”

https://www.independent.co.uk/news/world/middle-east/iran-protests-death-toll-arrest-government-crackdown-amnesty-a9249351.html

“The United States is urging Iraq to take steps to help prevent bases where U.S. troops are stationed from being shelled amid the country’s mass anti-government protests…

“Last week, Secretary of Defense, Mark Esper warned that attacks by Iran-backed groups on bases hosting U.S. forces in Iraq were pushing all sides closer to an uncontrollable escalation.”

https://www.theepochtimes.com/us-official-urges-iraq-to-stop-attacks-on-bases-housing-us-forces_3175794.html

“Young Shia Muslim men clashed with police in Lebanon’s capital overnight, after a video emerged that purportedly insults religious figures they revere… the third consecutive night of violence in Beirut.”

https://www.bbc.co.uk/news/world-middle-east-50821272

“As the Middle East ushers in 2020, experts say a new kind of uprising is unfolding. While the 2011 Arab Spring uprisings… were directed at long-ruling autocrats, the current economically driven uprisings are directed at an entire class of politicians and a system they say is broken and has failed to provide a decent life.”

https://abcnews.go.com/International/wireStory/protesters-arab-worlds-newest-uprisings-face-long-haul-67770038

It seems to me that the party most able to take such steps is the US itself. Remove the bases, and their chance of being shelled becomes zero.

I associate protests with hot weather. Going outside when it is cold out, to protest lack of natural gas, indicates a real problem. Uzbekistan produces more natural gas than it consumes. Theoretically, it should not have a problem.

The RACE is ON…faster, faster

Mexico Boosts Minimum Wage by Seven Times Rate of Inflation

Eric Martin

BloombergDecember 16, 2019, 8:51 PM EST

https://news.yahoo.com/mexico-boosts-minimum-wage-seven-015107166.html

(Bloomberg) — Mexico will raise its minimum wage by 20% as President Andres Manuel Lopez Obrador doubles down on redistribution policies even at the risk of spurring inflation and limiting the room for interest rate cuts.

The minimum wage will rise to 123.22 pesos ($6.50) a day next year, Labor Minister Luisa Alcalde announced at an event in Mexico City. While that’s less than the most aggressive pay hike proposal of 29% discussed by the head of the nation’s minimum wage commission, known as Conasami, it’s seven times the current rate of inflation, which slowed to 2.85% in late November.

Minimum wage increases have accelerated under Lopez Obrador, a leftist who has promised to boost income and well-being for the nation’s poorest who had lost purchasing power due to stagnant salaries amid inflation. The 20% raise announced Monday follows a 16% hike during his first year in power, at the time the biggest jump in two decades.

“This is going to help the economy of course because it strengthens the internal market,” Lopez Obrador said at an event at the National Palace in the nation’s capital, thanking union leaders and business representatives. “If there’s more revenue, it helps reactivate the economy, there are more sales for merchants.

What could possibly go WRONG!?

Sigh. Another forgotten truth of classical monetary theory, as explained by Adam Smith and Samuel Smiles: you cannot make poor people richer by giving them money. You give them education, vocational training, opportunity, and the moral courage to put their hand to the plough instead of holding it out.

Take it to the Streets…Occupy Wall Street the French Way….that should help your pension/retirement plans….

https://finance.yahoo.com/news/no-school-no-trains-no-083731774.html

PARIS (AP) — Teachers, doctors, Eiffel Tower employees and workers across the French labor force walked off the job Tuesday to resist a higher retirement age and to preserve a welfare system they fear their business-friendly president wants to dismantle.

Lighting red flares and marching beneath a blanket of multi-colored union flags, thousands of angry workers snaked through French cities from Brittany on the Atlantic to the Pyrenees in the south to oppose President Emmanuel Macron’s overhaul of the French pension system.

Commuters and tourists faced a 13th straight day of traffic headaches as train drivers kept up their protest of changes to a system that allows them and other workers under special pension regimes to retire as early as their 50s.

But I PAID into it and it was PROMISED to me….I’m entitled and DEMAND MY MONEY!

Across the French capital, union leaders demanded that Macron drop the retirement reform.

“They should open their eyes,” Philippe Martinez, the head of hard-left union CGT, said at the head of the Paris march.

Nationwide, the number of striking workers Tuesday was up from a similar cross-sector walkout last week., adding pressure to Macron, The president was already on the back foot after the key architect of his pension overhaul resigned Monday over alleged conflicts of interest.

So far, his government is sticking to plans to raise the retirement age to 64, though it made concessions last week by delaying the roll-out of the change and opened the door for new negotiations.

Government spokeswoman Sibeth Ndiaye said on BFM television: “The reform remains.…We will not withdraw it.”

Several European countries have raised the retirement age or cut pensions in recent years to keep up with lengthening life expectancy and slowing economic growth. Macron argues that France needs to do the same.

Well, the answer is NEGATIVE interest rates to spur Economic Growth…..sarcasm…Gail already debunked that solution for us! Thank you

PS This ain’t gonna end well…..

“But I PAID into it and it was PROMISED to me….I’m entitled and DEMAND MY MONEY!”

Dear stupid persons of French persuasion. Dear me, your government lied to you, made promises that it knew it could not keep, and is now giving you the shaft. Cry me a river.

“Put not your trust in princes” (Ps cxlvi:3) Or, if you prefer the version that at one time you heard read in your churches, when you still had churches: “Nolite confidere in principibus, in filiis hominum, in quibus non est salus.”

These government pension plans are all pay as you go plans, I am afraid. That is the only way the system can work. It can’t work with very many retirees relative to workers.

From last June:

Saskatoon senior amassed $20K in doomsday prep food before her death

There’s so much of it,’ says the executor of Iris Sparrow’s estate.

Her stash included eggs, rice, beans, lentil burgers, pasta, cheesy broccoli, strawberries, vanilla pudding — all in vacuum-sealed bags in boxes and plastic pails. Some packages have hundreds of servings.

Iris Sparrow died two days shy of her 80th birthday. RIP

https://pressfrom.info/upload/images/real/2019/06/14/saskatoon-senior-amassed-20k-in-doomsday-prep-food-before-her-death__355768_.jpg?content=1

https://pressfrom.info/ca/news/canada/-143623-saskatoon-senior-amassed-20k-in-doomsday-prep-food-before-her-death.html

Donate it to the Fast Eddy Rescue League of Gardeners and wanna be Farmers!

https://m.youtube.com/watch?v=-Jn32OCQ7ns

“An economist has warned that India’s slowdown is now directly affecting households in a big way, with 40,000 to 50,000 persons having forced to surrender their commercial vehicles till now due to non-payment of dues.

““The situation is very grim. Our data says that the number is around 40,000 to 50,000 across the country,” said SP Singh, senior fellow at Indian Foundation of Transport Research and Training.”

https://www.indiatvnews.com/business/news-people-surrendering-vehicles-economic-slowdown-commercial-india-571879

“India’s economy, it seems, has entered the stagflation phase with the key macro-economic data showing dwindling manufacturing activity as the subdued demand conditions contracted the October factory output by 3.8 per cent.

“The worsening trend has also been spotted in the Consumer Price Index (CPI) as an increase in food prices lifted the November retail inflation to 5.54 per cent from 4.62 per cent in October.”

https://www.gulftoday.ae/business/2019/12/16/rising-inflation-falling-growth—point-to-stagflation-in-india

I wonder to what extent that cut back in recycling has adversely affected India’s economy.

In the years immediately after the 2008 price spike, recycling seemed to be very important in the Indian economy. Many poor people made a living by picking up used plastic bottles and aluminum cans, and bringing them in for recycling.

When the US started to send more materials to India, it was at first helpful, I expect. But then the amount of recycling overwhelmed the system. Oil prices dropped in 2014, making recycling non-economic. The many people who make their living in the recycling industry were hurt, first through the lower prices paid for recycled materials and second when the recycling had to be discontinued, because it was not economic at current oil prices.

“A massive protest has broken out in India’s capital Delhi – as anger at a citizenship law spreads across the country.”

https://www.bbc.co.uk/news/world-asia-india-50818192

I wonder if part of the problem (besides religious differences) is simply that there are not enough good jobs to go around. Offering citizenship to some new people, whoever they are, cuts back on job opportunities.

Ouch! Fewer commercial vehicles are likely to be a big problem.

“Conventional monetary policy stimulation works through lower policy interest rates, which help boost demand by lowering the cost of borrowing. Given today’s low policy rates, if a recession were to occur in the near term and G4 central banks were to lower rates by their average recessionary cuts since 1960, policy rates would become deeply negative.”

https://www.top1000funds.com/2019/12/central-banks-limited-in-next-downturn/

“It’s becoming increasingly apparent that the negative interest rates introduced in several countries in the wake of the global financial crisis are trashing bank profitability. Less obvious, though perhaps more crucial for society as a whole, are their debilitating impact on pension plans.”

https://www.washingtonpost.com/business/negative-interest-ratesare-destroying-our-pensions/2019/12/17/a59e06e0-209b-11ea-b034-de7dc2b5199b_story.html

“Struggling to revive profits as low yields persist, a handful of troubled Japanese regional banks are wading deeper into riskier credits such as near-junk rated overseas bonds, according to a Bloomberg survey.”

https://www.bloomberg.com/news/articles/2019-12-16/stricken-local-banks-in-japan-turn-to-riskier-credit-to-survive

Maybe they can help out US energy companies!

Lol, good point! Perhaps there should be an OFW consultancy service matchmaking increasingly reckless lenders with increasingly desperate borrowers.

Right! Pension plans were hoping for big positive returns. Assumptions by actuaries are proving to be very much incorrect.

Interesting that a comparison is being made to the 1930s:

Another comment is

In the US, debt of many kinds has not been growing as rapidly as GDP. I am fairly certain that this is true in Europe as well. It seems to me that this lack of debt growth becomes too big a problem for the government to make up for with additional printed money.

https://gailtheactuary.files.wordpress.com/2019/12/domestic-finanacial-sectors-as-ratio-to-gdp-shown-beside-three-other-graphs-amounts.png

In the US, the big debt areas that have been lagging behind since 2008-2009 are (1) Financial sector debt and (2) Mortgage debt.

Household debt is closely related to mortgage debt. It also includes student loans and credit card debt, among other things. Only a short time series is available.

This article shows that there has been a spike in rejections of auto loans:

https://www.marketwatch.com/story/more-borrowers-are-getting-rejected-for-auto-loans-2019-12-16

It doesn’t look like the change has affected US motor vehicle loans outstanding yet, however. This chart is through September 30, 2019. The amounts seem to be the same as household automobile loans, so I don’t think that they include commercial auto loans.

https://gailtheactuary.files.wordpress.com/2019/12/us-motor-vehicle-loans-outstanding-through-sept-30-2019.png

The actual press release, if interested.

https://www.newyorkfed.org/newsevents/news/research/2019/20191216

About the same length as the market watch article.

A good point, Henry, except for that word “conventional”. Classical monetary theory says that you improve the economy by raising interest rates, which encourages more thrift, providing more capital for investment, and then helps direct that investment into the more profitable enterprises, the ones able to repay their borrowing out of profit generated.

Modern monetary theory, by contrast, leads to the creation of zombie organisations that eat debt until it is all consumed in negative return ventures.

Manufacturing recession is already here in the Eurozone.

Manufacturing in the Eurozone has now fallen to euro crisis levels. But there’s no crisis.

The ECB is already doing ZIRP and QE.

Can the central banks deal with a slowdown…and for how long?

https://pbs.twimg.com/media/EL5ccroXkAAETMa?format=png&name=900×900

45.9 not good.

“The manufacturing slowdown since the summer of 2018 has become a slump, the labour market shows first tentative bruises and, even worse, disruption in one of Germany’s key industries, automotives, do not bode well for the imminent future.

“In fact, there is a risk that the German economy is almost seamlessly moving from a golden decade into a lost decade.”

https://think.ing.com/articles/germany-entering-the-lost-decade/

“The euro zone’s second-biggest economy will slow next year to 1.1% from an estimated 1.3% this year, the Bank of France said in its quarterly economic outlook…

“Although the French economy has proven more resilient in the current slowdown than countries like export-dependent Germany and Italy, it too is feeling the pinch from a down-shift in global growth..”

https://uk.reuters.com/article/uk-france-economy-cenbank/french-central-bank-trims-outlook-on-global-slowdown-idUKKBN1YK17A

“The UK private-sector economy is shrinking at the fastest pace since July 2016, with manufacturing output tumbling and services activity recording consecutive monthly falls for the first time since 2009 amid Brexit uncertainty, a key reading shows.”

https://www.heraldscotland.com/business_hq/18105941.grim-reading-reveals-state-uk-economy/

Your chart is worrying! Germany, as Europe’s center of manufacturing, seems to be most affected. Automobile manufacture is especially important, I expect.

Gail, you may be right, but the car makers evidently don’t think so. For years, they have not even tried to make cars cheaper, more affordable, more in keeping with Henry Ford’s vision. Instead, they have continually made them more expensive, and not with useful features, but for added frills such as power windows, air bags, FM radios and cassette decks, … all of which can be built in at a heavy markup. And they are now reaping the consequences of their greed and folly.

(Oh, sorry, air bags are not a frill, they are an addition lethal to smaller women and invalids, as well as being propelled by poisonous chemicals)

And have saved plenty of lives. Let’s not forget that. The problem isn’t technology per se, but the decadence which it enables. Cars have been too cheap for too long.

If you ask for the price – then you can not afford it.

I respectfully disagree. Airbags save the lives of riders who do not use seatbelts. For those who do, they put lives at risk. In other words, they differentially preserve the stupid, and kill the intelligent. Enough said: you can guess my view of this situation.

I don’t care about viewpoints. I care about the actual statistics of life saving active and passive safety devices in modern cars.

There is little doubt that they do indeed save lives and serious injuries. Do some googling around and put aside the “ok d00mer” narrative for a moment.

“Chinese corporate debt is the “biggest threat” to the global economy, warned a Moody’s Analytics economist, who described such risks as a “very significant fault line.”

“That followed similar comments by Fitch Ratings last week, which said that private companies in China have defaulted on their debts at a record pace this year.”

https://www.cnbc.com/2019/12/17/chinas-corporate-debt-is-biggest-threat-to-global-economy-moodys.html

“Six privately owned companies in one of China’s wealthiest provinces have defaulted on their debt or come perilously close in the last three months.

“With 68.1 billion yuan ($9.7 billion) in outstanding debt among those six companies alone, the distress in Shandong has rattled even seasoned investors.”

https://www.caixinglobal.com/2019-12-17/defaults-in-one-of-chinas-richest-provinces-spook-investors-101495040.html

I looked up Shandong. It is China’s second most populous province. It is south of Beijing north of Shanghai, along the coast. The debt defaults in a rich province are concerning.

I would agree that China’s debt problem is a top threat to the global economy. It doesn’t matter with a deleveraging plan is one that is initiated to help the system. In fact, it is very detrimental to economic growth.

President of Pakistan is one of the world’s more dangerous occupations along with Prime Minister of India.

Now comes news that the knives are out for the country’s former President Pervez Musharraf, who I personally thought, in my naivety, was one of the more decent holders of the title.

According to a bulletin from the Telegraph:

Pakistan’s anti-terrorism court sentenced on Tuesday former military ruler Pervez Musharraf to death on charges of high treason and subverting the constitution, a senior government official said.

“Pervez Musharraf has been found guilty of Article 6 for violation of the constitution of Pakistan,” government law officer Salman Nadeem said.

Musharraf has been on trial for high treason for imposing a state of emergency in 2007.

Musharraf, who seized power in a 1999 coup and later ruled as president, has been living outside of Pakistan. He was not immediately available for comment.

On second thought, the record shows Prime Minister of Pakistan to be a far more dangerous job than President.

How propaganda works

I would like to return to the recent video in the campaign for the parliamentary elections 2020 in Slovakia, as there is an interesting clash of the two white males:

https://www.youtube.com/watch?v=owDQLb-TpCM

There are two dominant white males as party leaders presented in the video:

1. Robert Fico:

https://upload.wikimedia.org/wikipedia/commons/thumb/7/7c/Fico_Juncker_%28cropped%29.jpg/230px-Fico_Juncker_%28cropped%29.jpg

He is presented as an adult who comes to the kindergarten where children (representing the leaders of the competing parties) are doing mischiefs and quarrelling.

2. Boris Kollar:

https://static.markiza.sk/media/a501/image/file/21/0209/iajp.boris_kollar.jpg

He is a famous celebrity, a bussinesmen known as a polygamist, having multiple children with multiple women. The video represents him with his characteristic blue eyeglasses as a girl!!!

Boris Kollar made one of his women a party member and a member of the parliament thanks to the previous election results.

Polygamy is a male dominancy destroying element. The highest god is always single. The new perspective leader of the SMER SD party (which was solely dominated by Robert Fico until recently) is Peter Pellegrini, a single man, without publicly known relationships with women.

https://upload.wikimedia.org/wikipedia/commons/thumb/6/64/Peter_Pellegrini_-_2015.jpg/230px-Peter_Pellegrini_-_2015.jpg

Shall we meet again….???

The latest UN climate conference by the numbers: $100 million, 27,000 attendees, 1 prominent Swedish teenager, and 0 tangible outcomes

awoodward@businessinsider.com (Aylin Woodward,Morgan McFall-Johnsen)

Business InsiderDecember 16, 2019, 8:35 PM EST

The 25th iteration of the United Nations’ biggest annual conference on climate change, COP25, came to an end on Sunday in Madrid, Spain.

But despite a year of increased climate cognizance worldwide — led in part by Swedish activist Greta Thunberg — the 13 days of negotiations yielded few tangible outcomes.

“I am disappointed with the results of COP25,” António Guterres, UN secretary general, tweeted as talks closed. “The international community lost an important opportunity to show increased ambition on mitigation, adaptation, and finance to tackle the climate crisis. But we must not give up, and I will not give up

By no means, don’t give up….BAU says thank you so much!

Greta is Alia from dune! “meet my gom jabber grandfather”

top of the OFW home page:

Blog Stats

10,001,334 hits

that’s kinda cool…

here’s hoping for 10 million more… 🙂

I had noticed earlier that the site was close, but not that the site had actually exceeded that 10 million hits. Thanks for pointing this out.

Another statistic that I see is the number of approved comments. This recently exceeded 200,000.

The optimism of doom and gloom is spreading wide and far. How I laugh at the optimists deluding themselves with hopes and dreams of a green and sustainable tomorrow.

https://i.pinimg.com/originals/4c/a8/65/4ca865afaaf9674fb62b07997ae36ef8.jpg

King COAL

https://finance.yahoo.com/news/coal-endures-worlds-favorite-fuel-000050141.html

Coal Endures as World’s Favorite Fuel for Electricity Generation

Will Mathis

BloombergDecember 16, 2019, 7:00 PM EST

Coal Endures as World’s Favorite Fuel for Electricity Generation

(Bloomberg) — Coal consumption is set to rise in the coming years as growing demand for electricity in developing countries outpaces a shift to cleaner sources of electricity in industrialized nations.

While use of the most polluting fossil fuel had a historic dip in 2019, the International Energy Agency anticipates steady increases in the next five years. That means the world will face a significant challenge in meeting pledges to reduce greenhouse gas emissions that cause global warming.

“There are few signs of change,” the agency wrote in its annual coal report released in Paris on Tuesday. “Despite all the policy changes and announcements, our forecast is very similar to those we have made over the past few years.”

While this year is on track for biggest decline ever for coal power, that’s mostly due to high growth in hydroelectricity and relatively low electricity demand in India and China, said Carlos Fernandez Alvarez, senior energy analyst at the Paris-based IEA.

Despite the drop, global coal consumption is likely to rise over the coming years, driven by demand in India, China and Southeast Asia. Power generation from coal rose almost 2% in 2018 to reach an all-time high, remaining the world’s largest source of electricity.

Well. Let’s have another Climate Conference….Sally Field can fly in…

https://m.youtube.com/watch?v=rbwwk_k5-dw

After her arrest..Sally Field arrested during Jane Fonda’s weekly climate change protest

BY SOPHIE LEWIS

DECEMBER 14, 2019 / 10:49 AM / CBS NEWS

Maybe and maybe not. There are too many countries that seem to be past peak coal. It is very hard to keep prices high enough to make extraction profitable.

“China’s small rural banks are scrambling to raise new capital as they struggle to contain a rapidly rising number of overdue loans… 29 rural banks this year have applied to the China Securities Regulatory Commission (CSRC) to raise capital by selling new shares…”

https://www.scmp.com/economy/china-economy/article/3042252/chinas-rural-banks-struggling-under-pressure-overdue-loans

“China injected liquidity into the financial system by offering medium-term loans to banks, in the government’s latest effort to support economic growth…

“The People’s Bank of China (PBOC) added 300 billion yuan ($43 billion) through the medium-term lending facility, with 286 billion yuan being used to roll over loans coming due on Monday.”

https://www.caixinglobal.com/2019-12-16/china-injects-2-billion-into-banking-system-as-loans-mature-101494533.html

“China’s central bank warned property speculators that “homes are for living in” as the regulator pledged to properly regulate the real estate market…

“The central bank also said it will further expand an opening up of the financial sector, replenish the capital of small and medium-sized banks and improve their ability to offer credit. It pledged to properly handle risky issues in the financial industry to avoid major risks in 2020.”

https://economictimes.indiatimes.com/markets/stocks/news/china-central-bank-warns-property-speculators/articleshow/72725839.cms

It doesn’t matter how well-intentioned regulators are. Cutting back on the growth of debt tends to make the economy grow less rapidly. The jobs building unneeded homes are (unfortunately) an important part of China’s economy. These folks need to find employment elsewhere. Otherwise, they need to cut way back on their spending. This is part of what makes commodity prices fall.

Yes! Keep the system going.

I still don’t see how deflation happens….. I mean I do in some countries….the ones that can’t and won’t print money. But in the U.S when they promise everything to the voters? You will see bi partisan spending at the next recession and massive printing of U.S dollars….so how will that cause deflation? Deflation of the Dollar? All countries will be in the same boat and where are they going to put their money?

The problem is the debt defaults. People can’t afford the houses they live in and the cars they drive. Businesses cannot afford to pay the workers they have hired. There are lots of layoffs. Governments can print more currency, but this doesn’t provide more underlying goods and services. As with Venezuela or Zimbabwe, the extra currency is likely simply to push the value of the currency down on the world market. It can, in theory, buy more goods in the local market, but the shelves of stores will still be empty, so the currency has virtually no buying power. In a sense, this is inflation.

When it comes to the raw materials needed to make the goods and services, these will increasingly suffer from customers being unable to buy the end products made from them, as the real cost of extraction rises. Thus, the prices of raw materials will tend to deflate. This is where the deflation comes in. It will continue to be non-economic to produce them, so production will slow and stop. The world market will not provide the goods for the currency to buy. It is the inability to combine the resources from countries around the world that brings the process to a halt. The world was using resources from around the world at the time of Jesus’ birth–think of the Wise Men bearing gold, frankincense, and myrrh. Long before that, Greece, Italy and Egypt were importing tin to make bronze. The fact that printed money is local makes it inadequate to solve the problem.

What needs to change is the relationship between wages of common workers and the true cost of extraction of resources, including the higher cost required as a result of depletion. Once the cost of extraction is too high relative to these wages, there is a major problem.

Big auto mfg push coming in China according to reliable sources. The stimulus will be of epic proportions.

“The Ministry of Industry and Information Technology’s draft proposal said China should seek to ensure one in four of all vehicles sold in 2025 were either hybrids or fully-electric vehicles.”

https://today.rtl.lu/news/science-and-environment/a/1440066.html

«The measures are partly to ensure the country meets its air pollution targets, and to reduce Beijing’s dependence on imported oil«

The measure could perhaps also stimulate their own coalproduction, as i presume the EV run on electricity from coal-fired power plants? Or am i wrong?

Sven, regarding your question about whether the EVs are to run on electricity from coal-fired plants: Yes, a major purpose of EVs is to switch demand from oil to coal, and thus hopefully raise the price of coal. Another major purpose is to move pollution outside of major cities. A third purpose is to have a salable product for the world export market.

This is just wishful thinking:

China doesn’t have the money to subsidize electric automobiles sales now. This is one (of several) reasons way electric automobile sales are falling. Expecting China to have the money in the future to subsidize electric automobile sales is simply wishful thinking. It is sort of like wishing for water to run uphill. Unless electric automobiles are truly less expensive for the buyer, it is impossible to increase sales.

The point is not to provide vehicles for the people. They already got the basic transportation needs mostly covered by electric scooters and public transport.

It is stimulus for the economy. After building the n’th airport and concrete ghetto stops working – then it’s time to sink some money into building up the high-tech auto supply chain becoming a player there as well. The vehicles you might ask, to which I answer: so what? Nobody wants to be stuck in traffic in Beijing.

How about everyone rides a bicycle…..like in the old days

Somehow, we need sort of paved roads for the bicycles to ride upon. These are the problem. Also, bicycles are not suitable for carrying multi-ton replacement parts for wind turbines and other large objects needed by our industrial economy. They also don’t work for carrying water for fracking.

Dirt roads and trails in the forest is no problems for modern cross country bicycles. Actually, unpaved surfaces it is a feature and not a bug.

https://mtnweekly.com/wp-content/uploads/2018/04/Mountain-Biking-Trail-Etiquete-Mud-Season.jpg

that’s how the Japanese invaded Burma

Don’t count on modern cross country bicycles. Think of home made bicycles, made with local materials.

Bicycles and trains will be a part of IC, a long, long time after we drop petroleum enabled transportation.

https://mentalplanners.files.wordpress.com/2012/01/bikes-vs-cars.jpg

I wonder if we again will listen to the pounding of steam locos powering along the last stretches of rail in IC with boilers glowing red like coal in he11?

https://youtu.be/qVCZRQLfkWo

Industrial civilization will fail if energy consumption doesn’t stay high enough. In fact, a cutback in debt levels may be sufficient to bring the system down.

have you ever taken a long hard look at a bike

then tried to figure out how to make one in a non-industrial environment?

Good point!

Just use one that you build from salvaging parts from the billion already made.

IC will survive, you however will most likely not. So why not enjoy that hitl3rmobile of yours pretending that your wastrel consumerism is what makes BAU tick.

http://www.energyfuse.org/wp-content/uploads/2015/05/burning-oil-wells-kuwait-wired_18apr13_getty_b.jpg

Just light up the desert and call it growth. Because burning energy is good for ya’ “economy”.

💪

This could be the future, but it also means something different from industrial civilization as we know it.

https://www.facebook.com/photo.php?fbid=624857264779452&set=g.146587539416217&type=1&theater&ifg=1

https://i.pinimg.com/originals/4f/7e/c5/4f7ec591995b76705b32793dd2957842.jpg

Harry:

“China injected liquidity into the financial system by offering medium-term loans to banks, in the government’s latest effort to support economic growth…

“The People’s Bank of China (PBOC) added 300 billion yuan ($43 billion) through the medium-term lending facility, with 286 billion yuan being used to roll over loans coming due on Monday.”

wow, now China is imitating the Fed and doing massive quasi-repurchase operations…

what?

what liquidity problem?

let’s all do the Repo…

“So much for the great divergence between economic systems led by the U.S. and China. In the monetary arena, they look more alike than at any point in recent years.”

https://finance.yahoo.com/news/china-central-bank-fed-look-220050865.html

With all the activity, perhaps world markets will make it through year end!

The optimism will quickly wear off and of course the underlying issues you write about can only worsen, but sentiment does count for something.

The UK election result, which all but removes the feared no-deal scenario from the table, and the “phase one” trade deal between China and the US are temporarily relieving geopolitical anxiety and I can see us coasting through into the not-so-roaring 20’s without too much drama. Unless of course the repo issue snowballs or some black swan swoops down upon us.

Harry, I’m not so sure about “no deal”. I think it is firmly back on the table. First, because it is now a matter o law that the UK will leave on 31 January, and without an officially signed and sealed deal. Secondly, there is supposed to be an acceptable “trade deal” by the end on 2020, which will absolutely not happen because, as usual, the EU will not keep its promises. And finally, as the election showed, most of the adult population are sick, tired and disgusted with EU interference is what they would still like to be a sovereign country.

Low commodity prices are part of the problem:

“Many countries are facing structural uncertainties that could have far-reaching, systemic implications for markets and the global economy… questions [will be raised] about the functioning and resilience of the global economy and markets…

“The main worry – one that too few market participants have spotted – is that over the next five years, global economic and market conditions may need to deteriorate nearer to crisis levels before national, regional, and multilateral political systems muster an adequate response.”

https://www.theguardian.com/business/2019/dec/16/global-economy-trade-growth

History says that at some point, our luck runs out.

Yes, it was a good run while it lasted. I still recall great care-free days in the mid 70’s and my parents were basic middle class in Northern Virginia. My father did the 1 hour commute to his military job in Arlington/DC area. I had a motorcycle, a guitar, 3 square meals a day, ROTC scholarships for college. It was a great time to be alive even for regular people. My mother didn’t start to work even part-time until I was in high-school. And that wasn’t even because it was needed.

As it stands now, my mother still has premium level health insurance, can travel wherever and whenever she wishes, sends money to her kids and grandkids (they need it) and she still thinks the world is a great place and always will be. I have to bit my tongue when I visit. Timing is everything isn’t is? Sure, she had a tough childhood, but she did everything right and has a nice quality of life in her retirement.

I had it easy, even going into middle age, but won’t have the retirement she has. Her grandkids had it easy , but are struggling in their early adult years. I don’t even want to think about what kind of life the grandkids will have to face.

2019 is looking more and more like 1929 every day.

It depends on the mental disposition of the people. A slight shift toward autism seems to be evolutionary preferable as the technological advancement progresses at an ever increasing rate.

https://youtu.be/7Pq-S557XQU

Yes, person of the year is doing fine!

Yup, she’s raking in the money.

https://steemitimages.com/640×0/https://cdn.steemitimages.com/DQmXD7PxKos1rb23rV1AwBq3ahS8HDs4Uz3XBafwRLM2N2Z/71181921_2214673932163684_2183614085420023808_n.jpg

My son with mild autism (Asperger’s Syndrome) is doing surprisingly well in the job market. He can do a great job reading computer programs and finding bugs in them. This is not a skill everyone has.

I would say that most people with an obscure obsession of something, like, let’s say, people who find finite world issues fascinating.

Yes people, it is time to admit that you all belong to the club of mild autism.

Put the books aside and show us the code.

https://i.pinimg.com/originals/c9/c7/c2/c9c7c24576bc40705f9ad4c7d5a3bce8.jpg

Yep all the future generations have to pay for all that ……just keep adding it up…it was never really “earned” income…

Having had a reprieve of over a decade, we can only ask if we, personally, used it well.

I feel that I did, but, ‘Please, sir, may I have (another ten years) more?!’

Hmm, most unlikely I fear…….

Don’t despair just yet. Almighty God may yet grant us another decade of decadence.

“The lights are back on, yet it feels like no-one is home. The end of load shedding this week may have provided light relief, but its overall impact has been draining. Eskom are likely to sink even further into their black-hole of debt – currently estimated to be worth R450 billion – and it’s threatening to take South Africa with it.”

https://www.thesouthafrican.com/news/will-eskom-load-shedding-cause-recession/

“Zimbabwe’s fuel shortages have reached critical levels just less than two weeks before the Christmas holiday. Long winding queues are visible at most fuel stations while most are completely empty. Frustrated and desperate motorists are spending long hours parked at fuel stations.”

https://www.enca.com/news/zimbabwe-fuel-shortages-reach-critical-levels

“Zambia risks having to switch off power production completely at the Kariba hydropower dam for the first time as water levels already at the lowest in more than two decades continue to drop, according to the state-owned electricity utility…

“Zambia and Zimbabwe depend on hydropower plants at Kariba, the world’s biggest man-made freshwater reservoir, for nearly half of their generating capacity.”

https://www.moneyweb.co.za/news-fast-news/worlds-biggest-reservoir-may-stop-power-output-amid-drought/

create a population by unsupportable means

supply it with energy from an unsustainable source

govern it with people with unproven intelligence

and there you have our world crisis writ small

It will soon be writ large

I am afraid you are correct.

Hydroelectric is very intermittent, especially when it is not fed by melting ice water. I wish that countries had been told that they could not really build industries around hydroelectric, without at least doubling the cost with fossil fuels for when hydroelectric is not available. People cannot expect to use this electricity except for the most optional activities, such as watching television and videos. It is mostly a big waste of money.

Hydroelectric is not intermittent. Let’s drop that narrative, please.

It is dispatchable. It is not intended to be used as a replacement for thermal power generation. Once the reservoir is empty. There is no further means to dispatch power to control surges and spikes in the grid.

Dispatchable, Gail, Dispatchable. 🙂

Hydroelectric is available at certain times of the year. This makes it intermittent. It doesn’t necessarily have to be intermittent during a 24 hour period.

These are a few charts from my file:

https://gailtheactuary.files.wordpress.com/2018/08/california-annual-hydroelectric-production.png

https://gailtheactuary.files.wordpress.com/2018/07/washington-state-hydroelectric-generation-by-month.png

https://gailtheactuary.files.wordpress.com/2018/07/hydroelectric-generation-by-year-france-italy-spain.png

Hydroelectric is only dispatchable when it is available. Unfortunately, in parts of the world with rainy and dry seasons, this is a major problem. An economy with lot and lots of fossil fuels can use a little hydroelectric to help buffer intermittent wind and solar, at times.

Norway uses 100% dispatchable power for their electricity needs. 24/7/365

It is a matter of systems engineering and resource management. If there is an imminent drought, then perhaps spin up the thermals before the reservoirs are empty. Or run it to the last drop of water and act surprised.

That is if there are any spare capacity that can be brought online. If there is not, well, enjoy IC while it lasts.

New Zealand has done very well with hydroelectric dams. We have a lot of them, and they supply the bulk of our electricity all year round. Most of the rest of our electricity is supplied by geothermal and wind with a small percentage of solar. We also have fossil fuel fired generation, with coal being phased out in favour of gas and a move towards “renewables”.

The hydrodams are fed by either snowmelt from lakes in the Southern Alps or the Waikato River which flows from Lake Taupo (our largest lake, in a volcanic caldera).

As good as our hydrodams, geothermal, and wind are, however (and despite what everybody else likes to believe), they are not renewable.

New Zealand is sort of like Norway in that it is cold enough to get a lot of snowmelt to feed its hydroelectric. This seems to help. Countries in hot, dry climates do not do well with hydroelectric.

Generally intermittent sources of power is a good compliment to sufficient dispatchable power near by. Long transmission lines to population centers is a sign of bad systems engineering.

The energy needs in IC should never exceed the fully renewable capacity. The fossil fuels should be ear marked for its role as an absolutely fantastic raw material in the industrial processes which it plays a fundamental role in growing prosperity and technological advancement.

We do well with our hydro electric here in B.C. as well. Our small population (4.9 million) vs our huge mountains over a large area make it possible for us to have 93% of our electric power from hydro. We also have Site C which will provide us with lots of export power. Are you listening California?

“In a bid to boost its economy, Zambia legalized the production and exportation of cannabis on Monday which will serve only economic and medicinal purposes… the approval for the export of cannabis was granted at a special cabinet meeting earlier this month.”

https://www.reuters.com/article/us-zambia-cannabis/zambia-approves-cannabis-exports-to-boost-economy-idUSKBN1YK1XU

A country that cannot depend on its electricity supply has huge problems!

South Africa’s problem is peak coal. It coal production has been flat since 2007. Its electricity production stopped rising in 2007 as well. Between 2007 and 2018, South Africa’s population has risen by 18% during that time, so electricity consumption per capita has been falling, year after year. The price for exported coal has been low, so the country could not work around its problems by selling its exported coal at a higher price.