My view has long been that if the world economy does not have enough energy resources, it will have to contract. The situation is analogous to a baker without enough ingredients to bake the size of cake he wants to make, or a chemist not being able to set up a full-scale model of a reaction. Perhaps, if a plan is made to make a smaller, differently arranged economy, it could still work.

The types of energy with inadequate supplies are both oil (particularly diesel and jet fuel) and coal. Diesel and jet fuel are especially used in long-distance transportation and in food production. Coal is particularly used in industrial activities. Without enough of these fuels, the world economy is forced to make fewer goods and services, and to make them closer to the end user. Somehow the economy needs to change.

My analysis indicates that our expectation of what goes wrong with inadequate energy supplies is wrong. Strangely enough, it is the finances of governments that start to fail, early on. They add too much debt to support investments that do not pay back well. They add too many programs that they cannot be supported for the long term. They become more willing to quarrel with other countries. Of course, no one will tell us what is really happening, partly because politicians themselves don’t understand.

In this post, I will try to explain some of the changes taking place as the economy begins to reorganize and deal with this inadequate energy supply situation.

[1] One energy limit we are hitting is with respect to “middle distillates.” This is the fraction of the oil supply that provides diesel and jet fuel.

Each type of energy supply seems to be most suitable for particular uses. Middle distillates are the ones the economy uses for long distance transport of both humans and goods. Diesel is also heavily used in farming. If the world is short of middle distillates, we will have to figure out a way to make goods in a way that is closer to the end user. We may also need to use less modern farm equipment.

The top line on Figure 1 indicates that the world economy has gradually been learning how to use less total oil supply, relative to population. Before oil prices began to soar in 1973, oil with little refining was burned to produce electricity. This oil use could be eliminated by building nuclear power plants, or by building coal or natural gas electricity generation. Home heating was often accomplished by deliveries of diesel to individual households. Factories sometimes used diesel as fuel for processes done by machines. Many of these tasks could easily be transitioned to electricity.

After the spike in oil prices in oil prices in 1973, manufacturers started making cars smaller and more fuel efficient. In more recent years, young people have begun deferring buying an automobile because their cost is unaffordable. Another factor holding down oil usage is the trend toward working from home. Electric vehicles may also be having an impact.

On Figure 1, data for crude oil (second line) is available through October 2024. This data suggests that crude oil production has been encountering production problems recently. Note the oval labeled “Crude oil problem,” relating to recent production for this second line. The other two lines on Figure 1 are only through 2023.

The problem causing the cutback in oil production (relative to population) is the opposite of what most people have expected: Prices are not high enough for producers to ramp up production. OPEC, and its affiliates, have decided to hold production down because prices are not high enough. The underlying problem is that oil prices are disproportionately affected by what users can afford.

Food prices around the world are critically dependent upon oil prices. The vast majority of buyers of food, worldwide, are poor people. If budgets are stretched, poor people will tend to eat less meat. Producing meat is inefficient; it requires that animals eat a disproportionate number of calories, relative to the food energy they produce. This is especially the case for beef. A trend toward less meat eating, or even eating less beef, will tend to hold down the demand for oil.

Another approach to holding down food costs is to buy less imported food. If consumers choose to eat less high-priced imported food, this will tend to use less oil, especially diesel and jet fuel. Another thing customers can do to hold down food costs is to visit restaurants less. This also tends to reduce oil consumption.

On Figure 1, the third line is the one I am especially concerned about. This is the one that shows middle distillate (diesel and jet fuel) consumption. This is the one that was greatly squeezed down in 2020 by the restrictions related to Covid. Diesel is the fuel of heavy industry (construction and road building), as well as long distance transport and agriculture. Electricity is rarely a good substitute for diesel; it cannot give the bursts of power that diesel provides.

Close examination of the third line on Figure 1 shows that between about 1993 or 1994 and 2007, the consumption of middle distillates was rising relative to world population. This makes sense because international trade being ramped up, starting about this time. There was a dip in this line in 2009 because of the Great Recession, after which middle distillates per capita consumption noticeably leveled off. This flattening could be an early pointer to inadequacy in the middle distillate oil supply.

In 2019, middle distillate consumption per capita first started to stumble, falling 1.4% from its previous level. The restrictions in 2020 brought middle distillate consumption per capita down by 18% from the 2019 level. This was a far greater decrease than for total oil (top line on Figure 1) or crude oil (middle line). By 2023 (the latest point), per capita consumption had only partially recovered; the level was still below the low point in 2009 after the Great Recession.

Middle distillates can be found in almost any kind of oil, but the best supply is in very heavy oil. Examples of providers of such heavy oil are Russia (Urals), Canada (oil sands), and Venezuela (oil sands in Orinoco belt). The price for such heavy oil tends to lag behind the price for lighter crude oil because of the high cost of transporting and processing such oil.

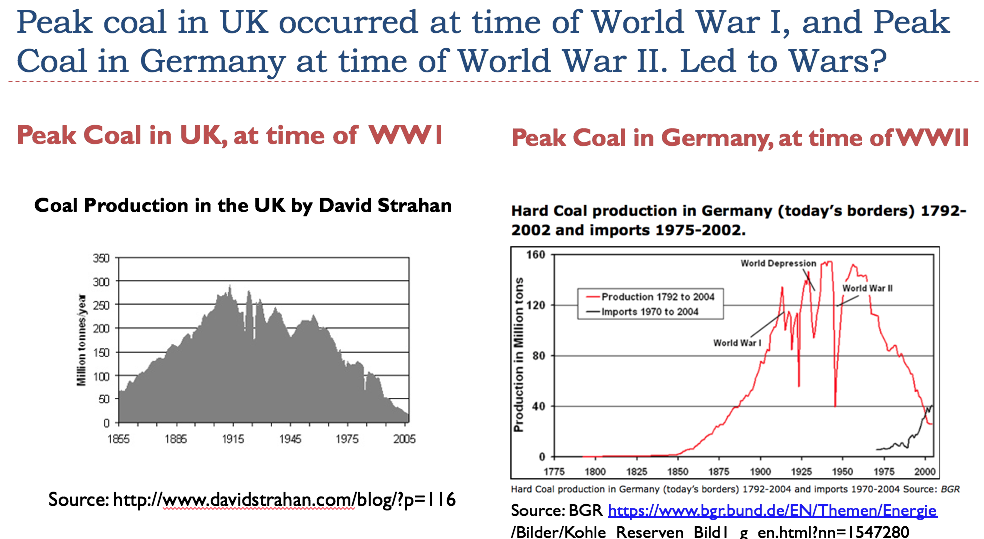

Strangely enough, countries that are not getting enough funds for their exported fossil fuels tend to start wars. My analysis suggests that at the time World War I started, the UK was not getting a high enough price for the coal they were trying to extract. The coal was getting more expensive to extract because of depletion. Germany had a similar problem at the time World War II started. The financial stresses of exporters who feel they are getting an inadequate price for their exported fossil fuels seems to push them toward wars.

We can speculate that the financial pressures of low oil prices have been somewhat behind Russia’s decision to be at war with Ukraine. The recent problems of Venezuela and Canada may also be related to the low prices of the heavy oil they are trying to extract and export.

Extracting a greater quantity of heavy oil would likely require higher prices for food around the world because of the use of diesel in growing and transporting food. Publications showing oil reserves indicate that there is a huge amount of heavy oil in the ground around the world; the problem is that it is impossible to get the price up high enough to extract this oil.

The existence of these heavy oil “reserves” is one of the things that makes many modelers think that our biggest problem in the future might be climate change. The catch is that we need to get the oil out at a price that consumers of food and other goods can afford.

[2] Another energy limit we are hitting is coal.

Coal energy is the foundation of the world’s industry. It is especially used in producing steel and concrete. Coal started the world industrial revolution. The primary advantage it has historically had, is that it has been inexpensive to extract. It is also fairly easy to store and transport. Coal can be utilized without a huge amount of specialized or complex infrastructure.

China produces and consumes more than half of the world’s coal. In recent years, it has been far above other countries in industrialization.

World coal consumption per capita has been falling since about 2011. Arguably, world coal consumption was on a bumpy plateau until 2013, with world coal consumption per capita truly falling only during 2014 and thereafter.

This pattern of coal usage means that world industrialization has been constricted, especially since 2014. In fact, the restriction started as early as 2012. It became impossible for China to build as many new condominium apartment buildings as inexpensively as promised; this eventually led to defaults by builders. World steel output started to become restricted. The model of world economic growth, led by China and other emerging markets, began to disappear.

The problem coal seems to have is the same as the problem diesel has. There is a huge quantity of coal resources available, but the price never seems to rise high enough for long enough for producers to truly ramp up production, especially relative to the ever-growing world population. Coal is especially needed now, with intermittent wind and solar leaving large gaps in electricity generation that need to be filled by burning some fossil fuel. Coal is much easier to ship and store than natural gas. Oil is convenient for electricity balancing, but it tends to be high-priced.

[3] Political leaders created new narratives that hid the problems of inadequate middle-distillate and coal supplies.

The last thing we can expect a politician to tell his constituents is, “We have a shortage problem here. There are more resources available, but they are too expensive to extract and ship to provide affordable food, electricity, and housing.”

Instead, political leaders everywhere created new narratives and started to encourage investments following those new narratives. To encourage investment, they lowered interest rates (Figure 4), made debt very available, and offered subsidies. Governments even added to their own debt to support their would-be solutions to energy problems.

Political leaders developed very believable narratives. These narratives were similar to Aesop’s Fable’s “Sour Grapes” story, claiming that the grapes were really sour, so the wolf didn’t really want the grapes he initially sought.

The popular narrative has been, “We don’t really want coal or heavy types of oil anyhow. They are terribly polluting. Besides, burning fossil fuels will lead to climate change. There are new cleaner forms of energy. We can also stimulate the economy by adding more programs, including more subsidies to help poor people.”

This narrative was supported by politicians in most energy-deficient countries. The increase in debt following this narrative seemed to keep the world economy away from another major recession after 2008. People began to believe that it was debt-based programs, especially those enabled by more US government spending, that pulled the economy forward.

They did not understand adding debt adds more “demand” for goods and services in general, and the energy products needed to make them. However, it doesn’t achieve the desired result if inexpensively available energy resources are not available to meet this demand. Instead, the pull of this demand will partly lead to inflation. This is the issue the economy has been up against.

[4] What could possibly go wrong?

There are a lot of things that have started to go wrong.

(a) US governmental debt is skyrocketing to an unheard-of level. Relative to GDP, the US Congressional Budget Office (CBO) projects that US debt will soon be higher than it was at the time of World War II.

Notice that the latest surge in US government debt started in 2008, when the Federal Reserve decided to bail out the economy with ultra-low interest rates (Figure 4). A second surge took place in 2020, when the US government began more give-away programs to support the economy as Covid restrictions took place. The CBO forecasts that this surge in debt will continue in the future.

(b) Interest on US government debt has become a huge burden. We seem to need to increase government debt, simply to pay the ever-higher interest payments. This is part of what is driving the increased debt projected in the 2025 to 2035 period.

Figure 6 shows a breakdown of actual Fiscal Year 2024 US Federal Government spending by major categories.

Note that US government spending on interest payments ($881 billion) is now larger than defense payments ($855 billion). Part of the problem is that the ultra-low interest rates of the 2008 to 2022 period have turned out to be unsustainable. (See Figure 4.) As older debt at lower interest rates is gradually replaced by more recent debt at higher rates, it seems likely that these interest payments will continue to grow in the future.

(c) Continued deficit spending appears likely to be needed in the future.

The CBO estimates in Figure 5 seem likely to be optimistic. In January 2025, the CBO expected that inflation would immediately decrease to 2% and stay at that level. The CBO also expects the primary deficit to fall.

(d) The shortfall in tax dollars cannot easily be fixed.

Today, tax dollars mostly come from American taxpayers, either as income taxes or as payroll taxes.

A person can deduce that to stop adding to the deficit, additional taxes of at least 5% or 6% of GDP (which is equivalent to 12% to 14% of wages) would be needed. Doubling payroll taxes might provide enough, but that cannot happen.

Corporate income taxes collected in recent years have been very low. US companies are either not very profitable, or they are using international tax laws to provide low tax payments.

(e) The incredibly low interest rates have encouraged all kinds of investment in projects that may make people happy, but that do not actually result in more goods and services, or more taxable income.

Figure 8 shows that US corporate income taxes have been falling over time. The reason is not entirely clear, but it may be that companies set their sights lower when the return that is required to pay back debt with interest is low. All the subsidies for wind, solar, electric vehicles, and semiconductor chips have focused the interest of businesses on devices that may or may not be generating a huge amount of taxable income in the future.

I have written articles and given talks such as, Green Energy Must Generate Adequate Taxable Income to Be Sustainable. Green energy can look like it would work if a person uses a model with an interest rate near zero, and policies that give renewable electricity artificially high prices when it is available. The problem is that, one way or another, the system as a whole still needs to generate adequate taxable income to keep the government operating.

Of course, many of the investments with the additional debt have been in non-energy projects. There have been do-good projects around the world. Young people have been encouraged to go to college using debt repayable to the government. Government funding has supported healthcare and pensions for the elderly. But do these many programs truly lead to higher tax dollars to support the US government? If the economy truly were very rich (lots of inexpensive surplus energy), it could afford all these programs. Unfortunately, it is becoming clear that the US has more programs than it can afford.

(f) The ultra-low interest rates have encouraged asset price bubbles and wealth disparities.

With ultra-low interest rates and readily available debt, property prices tend to rise. Investors decide to buy homes and “flip” them. Or they buy them, and plan to rent them out, hopefully making money on price appreciation.

Stock market prices are also buoyed by the readily available debt and low interest rate. The US S&P 500 stock market has provided an annualized return of 10.7% per year since 2008, while International Markets (as measured by the MSCI EAFE index) have shown a 3.3% annual return for the same period, according to Morningstar. The huge increase in US government debt no doubt contributed to the favorable S&P 500 return during this period.

Wealth disparities tend to rise in an ultra-low interest period because the rich disproportionately tend to be asset owners. They are the ones who use “leverage” to get even more wealth from rising asset prices.

(g) Tensions have risen around the world, both between countries and among individual citizens.

The underlying problem is that the system as a whole is under great strain. Some parts of the system must get “shorted” if there is not enough coal and certain types of oil to go around. Politicians sense that China and the US cannot both succeed at industrialization. There is too little coal, for one thing. China is struggling; quite often it seems to be trying to try to “dump” goods on the world market using subsidized prices. This makes it even more difficult for the US to compete.

Individual US citizens are often unhappy. With the bubble in home prices and today’s interest rates, citizens who are not now homeowners feel like they are locked out of home ownership. Inflation in the cost of rent, automobiles, and insurance has become a huge problem. People who work at unskilled hourly jobs find that their standard of living is often not much (or any) higher than people who choose to live on government benefits rather than work. Fairly radical leaders are voted into power.

[5] The major underlying problem is that it really takes a growing supply of low-priced energy products to propel the economy forward.

When plenty of cheap-to-extract oil and coal are available, growing government debt can help to encourage their development by adding to “demand” and raising the prices consumers can afford to pay. High prices of oil and coal become less of a problem for consumers.

But when energy supply of the required types is constrained, the additional buying power made available by added debt tends to lead to inflation rather than more finished goods and services. This inflationary tendency is the problem the US has been contending with recently.

Strangely enough, I think that growing inexpensive coal supply supported the world economy, as oil prices rose to a peak in 2011. As China industrialized its economy using coal, its demand for oil rose higher. The higher world demand coming from this industrialization helped to raise oil prices. But as coal supply (relative to world population) began to fall, oil prices also began to fall. By 2014, the decline in industrial production caused by the lower coal supply (Figure 3) likely contributed to the fall in oil prices shown on Figure 9.

It is the fact that oil prices have not been able to rise higher and higher, even with added government debt, which is inhibiting oil production. World coal production is inhibited by a similar difficulty.

[6] The world economy seems to be headed for a major reorganization.

The world economy seems to be headed in the direction that many, many economies have encountered in the past: Collapse. Collapse seems to take place over a period of years. The existing economy is likely to lose complexity over time. For example, with inadequate middle distillates, long-distance shipping and travel will need to be scaled way back. Trading patterns will need to change.

Governments are among the most vulnerable parts of economies because they operate on available energy surpluses. The collapse of the Central Government of the Soviet Union took place in 1991, leaving in place more local governments. Something like this could happen again, elsewhere.

I expect that complex energy products will gradually fail. Gathering biomass to burn is, in some sense, the least complex form of supplemental energy. Oil and coal, at least historically, have not been too far behind, in terms of low complexity. Other forms of today’s human-produced energy supply, including electricity transmitted over transmission lines, are more complex. I would not be surprised if the more complex forms of energy start to fail, at least in some parts of the world, fairly soon.

Donald Trump and the Department of Government Efficiency seem to be part of the (unfortunately) necessary downshift in the size of the economy. As awful as may be, something of this sort seems to be necessary, if the US government (and governments elsewhere) have greatly overpromised on what goods and services they can provide in the future.

The self-organizing economy seems to make changes on its own based on resource availability and other factors. The situation is very similar to the evolution of plants and animals and the survival of the best adapted. I believe that there is a God behind whatever changes take place, but I know that many others will disagree with me. In any event, these changes cannot take place simply because of the ideas of a particular leader, or group of leaders. There is a physics problem underlying the changes we are experiencing.

There is a great deal more that can be written on this subject, but I will leave these thoughts for another post.

{kind=link}

{kind=link}

{kind=link}