Once upon a time, we worried about oil and other energy. Now, a song from 1930 seems to be appropriate:

Today, we have a surplus of oil, which we are trying to use up. That never happened before, or did it? Well, actually, it did, back around 1930. As most of us remember, that was not a pleasant time. It was during the Great Depression.

Figure 1. US ending stocks of crude oil, excluding the Strategic Petroleum Reserve. Amounts will include crude oil in pipelines and in “tank farms,” awaiting processing. Businesses normally do not hold more crude oil than they need in the immediate future, because holding this excess inventory has a cost involved. Figure produced by EIA. Amounts through early 2016.

A surplus of a major energy commodity is a sign of economic illness; the economy is not balancing itself correctly. Energy supplies are available for use, but the economy is not adequately utilizing them. It is a sign that something is seriously wrong in the economy–perhaps too much income disparity.

Figure 2. U. S. Income Shares of Top 1% and Top 0.1%, Wikipedia exhibit by Piketty and Saez.

If incomes are relatively equal, it is possible for even the poorest citizens of the economy to be able to buy necessary goods and services. Things like food, homes, and transportation become affordable by all. It is easy for “Demand” and “Supply” to balance out, because a very large share of the population has incomes that are adequate to buy the goods and services created by the economy.

It is when we have too much income and wage disparity that we have gluts of oil and food supplies. Food gluts happened in the 1930s and are happening again now. We lose sight of the extent to which the economy can actually absorb rising quantities of commodities of many types, if they are inexpensive, compared to wages. The word “Demand” might better be replaced by the term “Quantity Affordable.” Top wage earners can always afford goods and services for their families; the question is whether earners lower in the wage hierarchy can. In today’s world, some of these low-wage earners are in India and Africa, or have no employment at all.

What is Going Right, As We Enter 2018?

[1] The stock market keeps rising.

The stock market keeps rising, month after month. Volatility is very low. In fact, the growth in the stock market looks rigged. A recent Seeking Alpha article notes that in 2017, the S&P 500 showed positive returns for all 12 months of the year, something that has never happened before in the last 90 years.

Very long runs of rising stock prices are not necessarily a good sign. According to the same article, the S&P 500 rose in 22 of 23 months between April 1935 and February 1937, in response to government spending aimed at jumpstarting the economy. By late 1937, the economy was again back in recession. The market experienced a severe correction that it would not fully recover from until after World War II.

The year 2006 was another notable year for stock market rise, with increases in 11 out of 12 months. According to the article,

Equity markets rallied amidst a volatility void in the lead-up to the Great Recession. Markets would make new all-time highs in late 2007 before collapsing in 2008, marking the worst annual returns (-37%) since the aforementioned infamous 1937 correction.

So while the stock market consistently rising looks like a good sign, it is not necessarily a good sign for market performance 6 to 24 months later. It could simply represent a bubble forming, which will later pop.

[2] Oil and other commodity prices are recently somewhat higher.

Recently, oil prices have been too low for most producers. Now, things are looking up. While prices still aren’t at an adequate level, they are somewhat higher. This gives producers (and lenders) hope that prices will eventually rise sufficiently that oil companies can make an adequate profit, and governments of oil exporters can collect adequate taxes to keep their economies operating.

Figure 3. Monthly average spot Brent oil prices, through December 2017, based on EIA data.

A major reason for the recent upward trend in commodity prices seems to be a shift in currency relativities for Emerging Markets.

Figure 4. Figure from Financial Times showing currency relativities based on the MSCI Emerging Market currency index.

While the currency relativities for emerging markets had fallen quite low when commodity prices first dropped, they have now made up most of their lost ground. This makes commodities more affordable in Emerging Market countries, and allows them to do more manufacturing, thus stimulating the world economy.

Of course, if China runs into debt problems, or if India runs into problems of some sort, or if oil prices rise further than they have to date, the run-up in currency relativities might run right back down again.

[3] US tax cuts create a bubble of wealth for corporations and the 1%.

With low commodity prices, returns have been far too low for many corporations involved with commodity production. “Fixing” the tax law will help these corporations continue to operate, even if commodity prices remain low, because taxes will be lower. These lower tax rates are important in helping commodity producers to avoid collapsing as a result of low commodity prices.

The problem that occurs is that the change in tax law opens up all kinds of opportunities for companies to improve their tax situation, either by changing the form of the corporation, or by merging with another company with a suitable tax situation, allowing the combined taxes to be minimized. See this recent Michael Hudson video for a discussion of some of the issues involved. This link is to a related Hudson video.

Groups evaluating the expected impact of the proposed tax law did their evaluations as if corporate structure would remain unchanged. We know that tax accountants will help companies quickly make changes to maximize the benefit of the new tax law. This is likely to mean that US governmental debt will need to rise much more than most forecasts have predicted.

In a way, this is a “good” impact, because more debt helps keep commodity prices and production to rise, and thus helps keep the economy from collapsing. But it does raise the question of how long, and by how much, governmental debt can rise. Will the addition of all of this new debt raise interest rates even above other planned interest rate increases?

[4] We have been experiencing artificially low oil prices since 2013. This helps the economic growth to be higher than it otherwise would be.

In February 2014, I published an article documenting that back in 2013, oil prices were too low for oil producers. If a person looks at Figure 3, oil prices were over $100 per barrel that year. Clearly, oil prices have been much too low for producers since that time.

Unfortunately, it looks like these artificially low oil prices may be coming to an end, simply because the “glut” of oil that developed is gradually being reduced. Figure 5 shows the timing of the recent glut of oil. It seems to have started early in 2014.

Figure 5. US Stocks of crude oil and petroleum products (including Strategic Petroleum Reserve), based on EIA data.

If we look at the combination of oil prices and amount of oil in storage, a person can make a rough estimate of how this glut of oil might disappear. Quite a bit of it may be gone by the end of 2018 (Figure 6).

Figure 6. Figure showing US oil stocks (crude plus oil products) together with the corresponding oil prices. Rough guess of how balance might disappear and future prices by author.

Of course, one of the big issues is that consumers cannot really afford high-priced oil products. If consumers could not afford $100+ prices back in 2013, how would it be possible for oil prices to rise to something like $97 per barrel by the end of 2018?

I am not certain that oil prices can really rise this high, or that they can stay at this level very long. Certainly, we cannot expect oil prices to rise to the level they did in July 2008, without recession causing oil prices to crash back down.

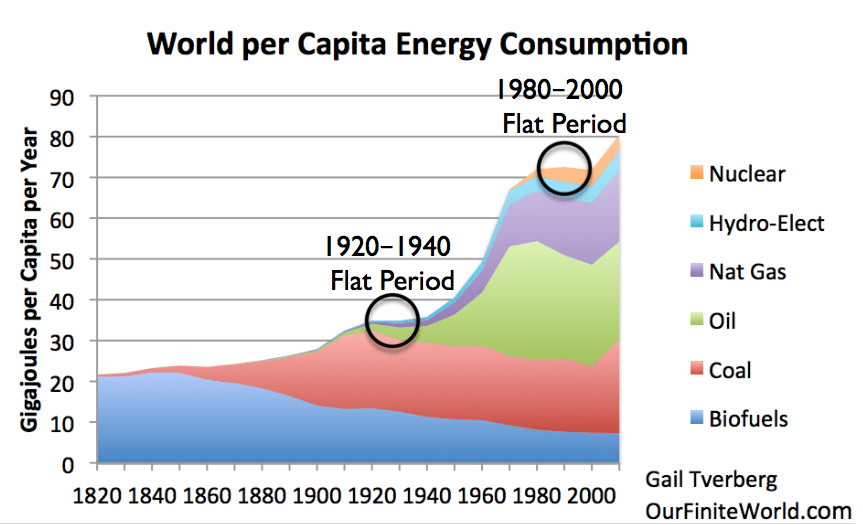

What the Economy Needs Is Rising Energy Per Capita

I have published energy per capita graphs in the past. Flat spots tend to represent problem periods.

Figure 7. World per Capita Energy Consumption with two circles relating to flat consumption. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects (Appendix) together with BP Statistical Data for 1965 and subsequent, divided by population estimates by Angus Maddison.

The 1920-1940 flat period came shortly after the United Kingdom reached Peak Coal in 1913.

Figure 8. United Kingdom coal production since 1855, in figure by David Strahan. First published in New Scientist, 17 January 2008.

In fact, the UK invaded Mesopotamia (Iraq) in 1914, to protect its oil interests. The UK wasn’t stupid; it knew that if it didn’t have sufficient coal, it would need oil, instead.

There were many other disturbing events during this period, including World War I, the 1918 flu pandemic, the Great Depression, and World War II. If there are not enough energy resources to go around, many things tend to go wrong: countries tend to fight for available resources; jobs that pay well become less available; deflation becomes more likely; population becomes weakened, and epidemics become more likely. I wrote about the 1920 to 1940 period in a recent post, The Depression of the 1930s Was an Energy Crisis.

The 1980-2000 flat period included the collapse of the Soviet Union, in 1991. The Soviet Union was an oil producer. The Soviet Union collapsed after prices had been low for a long time.

Figure 9. Former Soviet Union oil consumption, production, and inflation-adjusted price, all from BP Statistical Review of World Energy, 2015.

Even many years after the collapse of the Soviet Union, population growth in former Soviet Union countries and its affiliates was much lower than in the rest of the world.

Figure 10. World population growth rates between 2005 and 2010. Source: https://en.wikipedia.org/wiki/List_of_countries_by_population_growth_rate

Lower population (through falling birth rates, rising death rates, or rising emigration) are a major way that economies self-adjust because of falling energy per capita. Economies tend to fix the low-energy per capita problem by adjusting the population downward.

Recently, we have again been hitting flat periods in energy consumption per capita.

Figure 11. World per capita consumption of oil and of total energy, based on BP Statistical Review of World Energy data and UN 2017 population data.

The slowdown in world energy consumption per capita in 2008-2009 was clearly a major problem. Oil, coal and natural gas consumption fell simultaneously. Oil consumption per capita fell more than the overall mix, especially affecting countries heavily dependent on oil (Greece with its tourism, but also the US, Japan, and Europe).

The recent shift in political strategy to more isolationist stances also seems to be the result of flat energy consumption per capita. It is doubtful that Donald Trump would have been elected in the US, if world energy consumption per capita had been growing robustly, and if wage disparity had been less of a problem.

The primary cause of the 2013 to 2016 flat trend in world energy consumption per capita (Figure 11) is falling coal consumption (Figure 12). Many people think coal is unimportant, but it is the world’s second largest source of energy, after oil. We don’t have a good way of getting natural gas production to rise enough, to make up for loss of coal production.

Figure 12

Wind and solar simply do not work for solving our problem of flat or shrinking energy consumption per capita. After spending trillions of dollars on them, they make up only a tiny (1%) share of world energy supply, according to the International Energy Agency. They are part of the little gray “Other” sliver on Figure 13.

Figure 13. Figure prepared by IEA showing Total Primary Energy Supply by type from this IEA document.

Something Has to “Give” When There Is Not Enough Energy Consumption per Capita

The predicament we are facing is that energy consumption per capita seems to be reaching a maximum. This happens because of affordability issues. Over time, the price of energy products needs to rise to keep up with the rising cost of creating these energy products. But if energy prices do rise, workers earning low wages cannot afford to buy goods and services made with high-priced energy products, plus honor all of their other commitments (such as mortgages, auto loans, and student loans). This leads to debt defaults, as it did in the 2008-2009 recession.

At some point, the affordability problem can be expected to hold down energy consumption. This could happen in many ways. Spiking prices and affordability issues could lead to a worse rerun of the 2008-2009 recession. Or if oil prices stay fairly low, oil-exporting countries (such as Venezuela) may collapse because of low prices. Even if oil prices do rise, we may find that higher prices do not lead to sufficient additional supply because investment in new oil fields has been low for many years, because of past low prices.

As long as the world economy is expanding (Figure 14), individual citizens can expect to benefit. Jobs that pay well are likely to be available, and citizens can afford to buy goods with their growing wages. People who sell shares of stock and people who get pension benefits can all receive part of this growing economic output.

Figure 14. Author’s image of an expanding economy.

Once the economy starts to shrink (Figure 15), we start having problems with dividing up the goods and services that are available. How much should retirees get? Governments? Today’s workers? Holders of shares of stocks and bonds? Not all commitments can be honored, simultaneously.

Figure 15. Author’s image of declining economy.

One obvious problem in a shrinking economy is that loans become harder to repay. The problem is that there is less left over for other goods and services, after debt plus interest is subtracted, in a shrinking economy.

Figure 16. Figure by author.

Changing interest rates can to some extent help offset problems related to higher energy prices and shrinking supply. The danger is that interest rates can move in the wrong direction and make our problems worse. In the lead-up to the Great Recession of 2008-2009, the US raised short-term interest rates, helping to puncture the sub-prime mortgage debt bubble.

Figure 17. Figure comparing Case-Shiller Seasonally Adjusted Home Price Index and Federal Reserve End of Quarter Target Interest Rates. See Oil Supply Limits and the Continuing Financial Crisis for details.

We now hear a lot of talk about raising interest rates and selling QE securities (which would also tend to raise interest rates). If growth in energy consumption per capita is already flat, these changes could make the problems that the economy is facing even worse.

Our Economy Works Like a Bicycle

Have you ever wondered why a two-wheeled bicycle is able to stay upright? Research shows that a bicycle will stay upright, as long as its speed is greater than 2.3 meters (7.5 feet) per second. This is the result of the physics of the situation. A related academic article states, “This stability typically can occur at forward speeds v near to the square root of (gL), where g is gravity and L is a characteristic length (about 1 m for a modern bicycle).”

Thus, a bicycle will be able to continue in an upright manner, as long as it goes fast enough. If it slows down too much, it will fall down. Our economy is similar.

Gravity plays an important role in determining the speed of a bicycle. If the bicycle is going downhill, gravity gives an important boost to the speed of the bicycle. If the bicycle is going uphill, gravity very much pulls back on the bicycle.

I think of the situation of an economy having rising energy consumption per capita as being very much like riding on a bicycle, speeding down a hill. The person operating the bicycle would not need to provide much extra energy to keep the bicycle going.

If energy consumption per capita is flat, the person riding the bicycle must provide the energy to make it go fast enough, so it doesn’t fall over. This is somewhat of a problem. If energy consumption per capita actually falls, it is a true disaster. The bicyclist himself must provide the energy necessary to push the bicycle and rider uphill.

In fact, there are other ways that a speeding bicycle is analogous to the world economy.

Figure 18. Author’s view of analogies of speeding upright bicycle to speeding economy.

The economy needs a constant flow of outside energy. In the case of the bicycle, the human rider can provide the energy flow. In the case of the economy, the energy flow comes from a mixture of various fuel types, typically dominated by fossil fuels.

Growing debt (front wheel) is important as well. It tends to pull the economy along, because this debt can be used to pay wages and to buy materials to make additional goods and services. Thus, the effect of this increase in debt is indirect; it ultimately works through the bicyclist, the gears, and the back wheel.

In fact, the financial system as a whole is important for the “steering” of the economy. It tells investors which investments are likely to be profitable.

The gearing system of the bicycle plays a modest role in the system. Changing gears allows greater efficiency in the use of the energy that is available, under certain circumstances. But energy efficiency, by itself, cannot operate the system.

If the human rider does not provide sufficient energy for the bicycle to go rapidly enough, the bicycle glides for a while, and then falls over. The world economy seems to be similar. If the world economy does not obtain enough energy per capita, economic growth tends to slow and eventually collapses. The collapse can relate to the whole world economy, or to parts of the economy.

The Problem of Parts of the Economy Not Getting Enough Energy

We can think of the economy as being made up of many bicycles, operated by bicycle riders. At the beginning of the post, I talked about the problem of wage disparity. This issue occurred at the time of the 1930’s Great Depression and is occurring again now.

We might call wage disparity “too low a return on the labor of some workers.” In groups of animals in ecosystems, too low a return on the effort of these animals is what causes ecosystems to collapse. For example, if fish have to swim too far to obtain additional food, their population will collapse. It should not be surprising that economies tend to collapse, when the return on the efforts of part of their workers falls too low.

Wage disparity has to do with how well the operators of bicycles are doing. Are the operators of these bicycles receiving enough calories, so that they can keep pumping their bicycles fast enough so that the speed is high enough to remain upright?

If energy consumption per capita is growing, this greatly helps the operation of the economic system. If there is growing availability of inexpensive energy, machines of various types, including trucks, can be used to increasingly leverage the labor of workers. This increased leveraging helps each worker to become more “productive.” This growing productivity, thanks to growing energy consumption, allows more goods and services to be produced in total. It also allows the wages of the workers to stay high enough that they can afford to buy a reasonable share of the output of the economy. When this happens, “gluts” of unaffordable goods are less of a problem.

If energy consumption per capita is flat (or worse yet, falling), greater “complexity” is needed, to keep output of goods and services rising. Greater complexity involves more specialization and more training of individual members of the economy. Greater complexity leads to larger companies, more government services, and more wage disparity. Unfortunately, there are diminishing returns to complexity, according to Joseph Tainter in “The Collapse of Complex Societies.” Ultimately, increased complexity fails to provide an adequate number of high-paying jobs. Wage disparity becomes a problem that can cause an economy to collapse.

If there is not enough economic output, the physics of the economy tries to “freeze out” workers at the bottom of the hierarchy. Workers with low wages cannot afford homes and families. The incidence of depression rises. Debt levels of disadvantaged groups (such as young people in the US) may rise.

So the situation may not be that the whole world economy fails; it may be that parts of the economy collapse. In fact, we are already seeing evidence that this is taking place. For example, life expectancies for US men have been falling for two years, because of growing problems with drug overdoses.

Conclusions

In 2017, the world economy seemed to be gliding smoothly along because the economy has been able to get the benefit of artificially low energy prices and artificially low interest rates. These artificially low prices and interest rates have given a temporary boost to the world economy. Countries using large amounts of energy products, including the US, especially benefitted.

We cannot expect this temporary condition to continue, however. Low oil prices have already started to disappear, with Brent oil prices at nearly $69 per barrel at this writing. The trends in oil prices and oil stocks in Figure 6 are disturbing. If oil prices begin to rise toward the price needed by oil producers, they are likely to trigger a recession and a drop in world energy consumption, just as spiking prices did in 2008-2009. There is a significant chance of collapse in the next 12 to 24 months. It is hard to know how widespread such a collapse may be; it may primarily affect particular countries and population groups.

To make matters worse, our leaders do not seem to understand the situation. The world economy badly needs rising energy consumption per capita. Plans to raise interest rates and sell QE securities, when the economy is already “at the edge,” are playing with fire. If we are to keep the world economy operating, large quantities of additional energy supplies need to be found at very low cost. It is hard to be optimistic about this happening. High-cost energy supplies are worthless when it comes to operating the economy because they are unaffordable.

Many followers of the oil situation have had great faith in Energy Returned on Energy Invested (EROI) analysis telling us which kinds of energy supplies we should increase. Unfortunately, EROI doesn’t tell us enough. It doesn’t tell us if a particular product is scalable at reasonable cost. Wind and solar are great disappointments, when total costs, including the cost of mitigating intermittency on the grid, are considered. They do not appear to be solutions on any major scale.

Other researchers looking at the energy situation have not understood how “baked into the cake” the need for economic growth, rising per capita energy consumption, and rising debt levels really are. Rising debt is not an error in how the financial system is put together; a bicycle needs a front wheel, or it cannot operate at all (Figure 18). I have written other articles regarding why debt is needed to pull the economic system forward.

This economic growth cannot be “fake growth” either, where a debt Ponzi Scheme seems to allow purchases that real-life consumers cannot afford. Quite a bit of what is reported as world GDP today is of a very “iffy” nature. If China builds a huge number of apartments that citizens cannot afford without subsidies, should these be counted as true GDP growth? How about unneeded roads, built using the rising debt of the Japanese government? Or recycling performed around the world, because it makes people “feel good,” but really requires substantial subsidies?

At this point, it is hard for us to know where we really are, because every government wants to make GDP results look as favorable as possible. It is clear, however, that 2018 and 2019 can be expected to have more challenges than 2017. We have interesting times ahead!

{kind=link}

Tax overhaul will have a limited effect on U.S. economy, Moody’s says

More than three-quarters of the $1.1 trillion in individual tax cuts will go to people who earn more than $200,000 a year in taxable income, who constitute only about 5% of all taxpayers

https://www.marketwatch.com/story/tax-overhaul-will-have-a-limited-effect-on-us-economy-moodys-says-2018-01-25?link=sfmw_tw

Looks like it won’t be helping Trump country…Oh well deporting a dreamer will make them feel better..

https://imgur.com/a/sNGO5

While the tax cut will reduce the taxes of large companies, it will also reduce the taxes of almost everyone else. One estimate said that 95% of US taxpayers will find their 2018 tax payments lower. The net result of the tax overhaul is that it will greatly increase the deficit, and thus the needed debt of the US government. (In theory some of the benefits will go away, so taxes on citizens will rise later, but I will believe this when it actually happens.) The net effect is that the US government will need to put a lot more debt securities on the world market in the near term. A reasonable person might think that this will drive interest rates way up, and that this might be a problem.

If there is a stimulus effect, it comes is from the reduction of the taxes of 95% of the US citizens. This may partly offset the rising interest rate problem.

Moody’s analysis is woefully lacking, in my opinion. The issue is as much a “overall tax level is way to low, in the near term” problem than it is an allocation issue.

IMF found out that increasing the income share of the rich actually decreases GDP growth:

If the income share of the top 20 percent increases by 1 percentage point, GDP growth is actually 0.08 percentage point lower in the following five years, suggesting that the benefits do not trickle down. Instead, a similar increase in the income share of the bottom 20 percent (the poor) is associated with 0.38 percentage point higher growth.

https://www.imf.org/external/pubs/ft/sdn/2015/sdn1513.pdf

An inadequate supply of cheap energy also increases wage disparity. It also reduces GDP growth. So both growing wage disparity and reduced GDP growth are caused by an inadequate supply of cheap energy. The problem is not that some mean people increased wealth distribution to the rich, and this is what reduced GDP growth. It is a physics problem. I am sure I explained this problem before.

KunstlerCast – What Happened to Peak Oil? – Chat with Art Berman

http://kunstler.com/podcast/kunstlercast-299-happened-peak-oil-chat-art-berman/

Tesla and GM self-drive cars involved in road collisions in California

Culver City’s fire service said the Tesla had “ploughed into the rear” of one of its fire engines parked at the scene of an accident on Monday.

The GM incident resulted in a collision with a motorbike in San Francisco. The rider says the car – which was using GM’s Cruise Automation technology – caused him serious injury and is now suing GM.

http://www.bbc.com/news/technology-42801772

“Tesla has introduced an update that brings its cars to a halt if they detect a driver’s hands are not on the wheel.”

Wow – that is really high tech sh it!!!!

https://www.youtube.com/watch?v=Hl9y7v8UohM

Very advanced tech that is hard to fool /s

So, if this sensor goes out, your Teslas won’t go? Peak complexity is here!

Don’t worry, the next model will have another sensor to constantly monitor this sensor…

Can anyone comment on what CM says between the 27-29 minute mark? (I didn’t watch the whole thing)

This is the whole “discovery” issue, and the missing pipeline of oil coming from these discoveries. It is probably an issue to some extent. If deepwater oil discoveries had been made, and are missing, the effect would be longer then the three years or so CM mentioned, however.

I think just as important is not working on known oil. For example, Saudi Arabia has heavy oil in the shared neutral zone that it could be developing. It is offline because of disputes that I expect indirectly relate to low oil prices.

I am not certain we know how well Saudi Arabia is working on available projects that it has known about for years. This article makes it sound like they are still continuing to work on known possible projects, so as to continue and to increase production. http://www.oedigital.com/component/k2/item/16806-middle-east-epci-activity-on-the-rise

Saudi Arabia’s King (Dictator) said back around 2009 in Reuters any new oil field discoveries were to be saved for future Saudi generations only..

I think that this meant he didn’t actually have any more fields.

that’s always the sick joke

no nation can exist in ”oil using” isolation while those around it have none.

the same would apply to food rich/food poor nations…they would be invaded and looted

A large percentage of ex-pats working at Aramco have been let go. Aramco’s progress will be doubtful.

I can believe that laying off knowledgable workers would be a problem in Saudi Arabia. I expect that this is a bigger problem than the reduced discoveries.

The Saudi oil for dollars experiment is going to get really interesting soon!

“Can anyone comment on what CM says between the 27-29 minute mark?”

He’s saying CB’s aren’t going to do anything to upset the economy, but what could cause a recession is the rising price of oil due to USD currency reduction in value. He’s was also saying the US punishes other countries by freezing their bank accounts like they did to Iran, so many countries like Russia and China are making bilateral deals to get around the USD and that’s part of the reason it’s losing value. I like Martenson and agree if something is going to derail the economy it’s rising oil price.

I see it as a combination of events that will cause recession and eventually collapse. Higher oil prices, lead to inflation of all types of goods and services, leads to interest rate rises.

Consumers get squeezed from all sides and reduce discretionary spending.

This causes job losses, which worries consumers more, then they further reduce all spending, worrying about their own income. Businesses close, further job losses, more worried consumers. It is a viscous cycle.

At some point markets also tank, but there is a time lag effect from the initial oil price rises and interest rate rises as occurred from 2004-2007.

Already in the US we can see oil price rises, interest rate rises, plus job losses in the retail sector, but the market has not done it’s part in bringing on recession/depression.

IMO the timeline varies between recessions, and from country to country, but as oil becomes ever more expensive to recover, modern lifestyles get squeezed more and more.

In the US there is basically free money for the oil industry to keep production up from tight oil. At some point this will finish or the effect will be dramatic on the economy (too much spent on oil recovery, rest of economy failing). Then world oil prices will rise, taking other countries also into recession.

One of these recessions becomes a depression/collapse, but each one is a further step down the seneca cliff.

g’day, mate… aren’t you in Australia? if not, my bad…

“IMO the timeline varies between recessions, and from country to country, but as oil becomes ever more expensive to recover, modern lifestyles get squeezed more and more.”

one biggie would be if a core country falls into severe recession/depression…

what are Australia’s chances?

third world countries will be falling first and worst…

but when a core country falls…

that will be the beginning of the end.

Yes in Aus! I think we really started down the steep decent in 2007-8, with the bailouts to mask the effect of peak conventional oil.

To most, well many in the OECD countries it still looks like BAU, but when the next high priced oil induced recession hits (obviously very close), we all go down a bit further.

Like you I hope we can last until 2030, but I am increasingly doubting it. The next step down looks like it could be a doosy with the CBs out of ammo to bail out all the debt pile.

Mind you I think that hyper inflation is going to happen everywhere, to take care of the debt, but it will not solve any economic crisis.

Is Australia a ‘core’ country, or something of a borderline one? Merely a theatre for real estate speculation and supplier of commodities to Asia and beef/lamb to Arabs and Jews, etc, or something more?

Australia is a resource/source centre for food and raw materials as far as our current economic system goes

It’s going to keep on dropping!

https://imgur.com/a/oLSTj

but won’t taxes go up when the Ds get the presidency in 2020?

hey BD, who’s your preference?

Joe Biden?

Corey Booker?

Kamala Harris?

Elizabeth Warren?

Oprah says she’s not interested.

Mark Zuckerberg!

I am hope he does the unthinkable! Redistribute the wealth from the rich to the rest via UBI and universal healthcare! And he can do it at the speed of technology!

How about tax cuts for everyone? Create new “wealth” by driving up debt.

Baby D,

The developed world has had universal health care for 50+ years. High tech not required.

Good graph, BD. The tax cuts probably reduces currency investors perception of a strong dollar, because it causes bigger deficits. One of the things this Admin. did was to project a very high GDP number of 4% moving forward (to get their tax cut), but GDP hasn’t been that high for 12 years, so when the real number is lower, deficits will be even higher than projected based on the new tax code. They did the tax cut to benefit their base, the one’s that plunk down 10 thou a plate at campaign fundraisers, but it was a foolish move at a time when the economy was already on life support with a super low interest rate.

Democrats aren’t going to raise taxes to pay for anything either.

If they do, the wealthy philanthropists stop funding their non-profits and lots of Democrats become unemployed as capital moves overseas.

The tax breaks help businesses that offer crucial products such as oil in business, Low prices from low demand is pushing them towards bankruptcy.

You need to stop looking at everything through partisan-tinted sunglasses. We need oil companies to not go bankrupt. We need producers of commodities to not go out of business.

That’s who I think these tax cuts are meant to help, not companies like Google or hedge funds who pay very little taxes through loopholes.

Yep. This is aimed at keeping corporations alive….which of course keeps people employed and BAU alive….

It’s another desperate measure from the el ders….

It has absolutely f789 all with enriching the rich…. not to say that it won’t enrich them….as a side effect…. but that is not the purpose of this change to the tax code.

Thanks for the comments

https://www.politico.com/story/2018/01/24/white-house-trump-attack-u-s-dollar-308351

‘Breaking tradition, Trump team unleashes verbal assault on the dollar’

“The Trump administration declared a surprising war on the U.S. dollar on Wednesday, breaking from a long tradition in which top American officials generally voice support for a strong American currency. Speaking at the World Economic Forum in Davos, Switzerland, Treasury Secretary Steven Mnuchin shocked Wall Street by lauding the impact a weaker dollar can have on U.S. companies as it makes exports cheaper for other countries to buy. “Obviously, a weaker dollar is good for us as it relates to trade and opportunities,” Mnuchin told reporters in Davos. Mnuchin said recent declines in the value of the dollar against other currencies were “not a concern of ours at all.”

“The dollar continued its recent descent following Mnuchin’s remarks. It’s now down about 10 percent against a basket of other currencies since last January, when President Donald Trump said the greenback was “too strong,” making it hard for U.S. companies to compete against China and other countries. The currency decline has puzzled some economists and Wall Street traders because the dollar generally rises in value as the economy improves and the Federal Reserve increases interest rates. Yields on U.S. Treasury debt are currently rising as the Fed shifts policy. Rising yields usually make the dollar more attractive to investors, but the greenback keeps dropping.”

So what it’s our currency. Trash the dollar! Well, it’s a new approach and so far it’s working to devalue the dollar which makes oil in USD more for Americans. Good luck US – get use to a rising oil price and cost of other products as well.

Does this Admin. realize this one move could usher in a US recession? What’s good for companies doing overseas business may not be good for the overall US economy.

Tearful Elon Musk Warns About Dangers Of AI After Having Heart Broken By Beautiful Robotrix

https://www.theonion.com/tearful-elon-musk-warns-about-dangers-of-ai-after-havin-1822192554

Good grief. I have heard it all.

Fresh interview 51 min with Joseph Tainter author Collapse of Complex Societies

Interviewer- Lynnette Zhang is from the financial sector but is fairly competent

Tainter explains in depth on collapse. Zhang keeps up & asks good questions. Worth watching.

Watched it all. A slow start but Tainter gets going on a wide range of collapse topics including social, population, collapse recovery etc.

Good.

Good interview….thank you for posting.

Humans are very good at propping up the unsustainable and this often results in fast and unexpected collapse. (Tainter 1988)

Probably more likely to attempt to prop up the unsustainable, at any cost, than to devise a new model.

the current Capetown water problem is a good example of that.

While you can ration water for 3m people for a short time to prop up the system, long term it must collapse.

you cannot have 3m people served by a few hundred water points and have them fetch it every day.

coupled with which you need water for sewage disposal

How do you ration it through the tap? I can’t see it being done. That means no flushing.

it’s very rough and ready—but rationing is by the amount people can carry away

and that doesn’t allow for waste flushing—we can only leave that to our imaginations

long term it’s impossible of course

Dr Tainter makes an excellent point around 25.00 that innovation is actually now declining. I would also add that human IQ has also stop increasing and has now gone into reverse. Known as the “Reverse Flynn Effect”.. which I assume can only make matters even worse for future innovation.

Peer Reviewed Study: A long-term rise and recent decline in intelligence test performance: The Flynn Effect in reverse. (Teasdale 2005)

https://www.sciencedirect.com/science/article/pii/S0191886905001145

“IQ has also stop increasing and has now gone into reverse.”

Technofetischists will assure you this is only temporary.

Until we start DNA reprogramming.

Any day soon. Probably before Mars colonization. Before 2026.

The study is pretty old. Is it confirmed by newer studies? Would be interessenting to know.

i watched that tainter video

then he makes the classic mistake—that our energy future is going to be nuclear

simply doesnt get it—that electricity of itself is useless without the infrastructure provided by our use of fossil fuels

“that electricity of itself is useless without the infrastructure provided by our use of fossil fuels” – I have heard the argument that with enough electricity you can synthesize crude oil. Even if it would work, it still doesn’t get around the finite resource issue. Not to mention it is hugely electricity intensive to do that. At some point we have to accept our fate. The predicament has no resolution outside of collapse.

France’s Macron says globalization is going through a major crisis

https://www.cnbc.com/2018/01/24/france-macron-says-globalization-is-going-through-a-major-crisis.html

Let us not be naive, you can’t “reform” a zero sum globalized Ponzi scheme. Davos billunaires pretend to be ‘worried’ about wealth inequality even as they celebrate their most recent tax cut. What they’re worried about is rioting. And what they want IS a race to the bottom on taxes and regulation, to fund further “growth”. Ponzi schemes don’t go in reverse.

Without “growth” industrial civilization falls apart.

The race to the bottom is them admitting that we can no longer afford regulations and social services.

The alternative is something like Communism (now called Universal Basic Income) and that failed.

“… them admitting that we can no longer afford regulations and social services.”

this is the kind of thing that hints at “them” knowing that the root of recent economic crises is energy… so deregulate like crazy…

or perhaps “they” think that energy is at least one of the key components of economies…

of course, “we” know it is the main component…

the path forward for globalization seems to be the current path:

let peripheral countries become failed states, which leaves more resources for the core countries…

and referencing BD, the “rioting” would be contained within those failed states…

win-win for the globalists.

I agree that we can no longer afford regulations (financial / environmental) or social services.

Baby Doomer. You really are a confused baby. Against the globalist billionaires but in favor of the open borders they endlessly promote

https://ibb.co/bA3g9G

Yes, he opposes billionaire oligarchs by supporting their policy plan to import a permanent helot class of producer-consumers that they can pay even less than minimum wage and tie into debt slavery.

What open borders? We took 1.5 million immigrants last year. That is about a 0.25% increase in our population of 325 million people…And if I had my way it would be ZERO new immigrants in our country every year..Since I truly believe we are very overpopulated. But I am not going to have a cow over a small fraction of quarter percent increase..And just because I am don’t have a cow about it doesn’t automatically mean I believe in open borders and I want to kill whitey!

Your math is not very good. 1.5 million/ 325 million is 0.46%, not 0.25%.

US total population growth is about 0.7%. https://www.nytimes.com/2016/12/22/us/usa-population-growth.html So immigration now makes up the majority of our population growth, if your numbers are right. Immigrants also have higher than the average level of births. Without immigrants, our population have an age distribution more like Europe’s age distribution, and growth would be very slow, or possibly even negative. The working age group would shrink very soon.

Europe has some immigrants but they don’t have enough jobs for the immigrants and the immigrants are having trouble assimilating.

Thing is …

Immigration is wrecking europe, despite being just a couple millions each year.

You have 250M middle easterners without a future and even more north africans.

The Hispanics we have been adding tend to be hard working. Their culture is not too different from that in the United States, and it is not too hard for someone who speaks Spanish to learn English. I haven’t lived in an areas with a very high percentage of Hispanics, but it is easy to have a fairly favorable image of them. The big issue, I might suppose, is driving down wage levels in fields where they tend to work–construction, gardening work, and agriculture.

I think it is part a matter of wage structure, part a matter of the nations economy and part a matter of the immigrants skill.

If the immigrant lacks skills, the nation lacks manufacturing industry and the wage level is very … level … it takes a 1-2% (succesful engineer, doctor) up to three hours of work on the margin to pay for one hour of minimum wage work.

It is much better for the engineer to take time off from work to paint his house, clean his pool and mow his lawn than importing someone to do this.

But my point was humanitarian. Just the last 2-3 years it seems to have become obvious to a large part of the population that immigration is economically detrimental.

So now the humanitarian angle is applied. But since it is not possible moving 1B+ third worlders into europe you could argue it would be more fair to everyone to not import anyone here.

It appears mainstream is taking notice, but for some reason they are illustrating it with cardboard props.

https://www.youtube.com/watch?time_continue=1410&v=XBE_L3VbUuA

the mainstream is noticing because it’s an anti-Trump meme.

nuclear war is always a slight possibility, and perhaps will happen by human error rather than intention… how’s that for Doom?

meanwhile, the Energy Clock keeps on ticking towards midnight…

I would put that clock at about 11 pm… another decade or so until that clock strikes…

and I’d bet anything that IC crashes because of lack of cheap FF rather than nukes.

American Airlines CEO: ‘Fares are too low for oil prices this high’

https://www.cnbc.com/2018/01/25/american-airlines-ceo-fares-are-too-low-for-oil-prices-this-high.html

Sounds like precursor to rising airline fares. Doesn’t take long after oil price rises and it will be felt with many other services and products.

Doesn’t help the tourism industry, or Greece.

‘Doomsday clock’ ticks closer to apocalyptic midnight

https://edition.cnn.com/2018/01/25/politics/doomsday-clock-closer-nuclear-midnight/index.html

The doomsday clock has always cracked me up because unless its actually midnight it’s not a problem.

Saudi Arabia’s energy minister says IEA overhyped US shale boom

Saudi Arabia’s energy minister took a rare sideways swipe at the International Energy Agency on Wednesday, accusing the body of overhyping the impact of US shale growth on the oil market. In a retort to remarks by IEA head Fatih Birol, Khalid Al Falih said at an energy panel in Davos that the agency was failing to put the scale of US production increases into context. “I was not disputing the amazing revolution of shale . . .[but] in the overall global supply demand picture it’s not going to wreck the train,” said Mr Falih. “We should not be scared,” he added, at the World Economic Forum’s annual conference on Wednesday.

“That’s the core job of the IEA, not to take it out of context.” Mr Falih appeared alongside his Russian counterpart Alexander Novak and US energy secretary Rick Perry, who together now represent countries pumping more than a third of the world’s crude. The appearance of a US representative on a panel of traditional producer nations illustrates the transformative effect the shale boom has had on global energy markets.

The IEA said last week US crude production was on course to overtake Saudi Arabia and rival Russia, with the body revising 2018 growth forecasts for the US higher to output of more than 10m b/d. The Paris-based body stressed that “explosive” expansion in shale was offsetting Opec-led supply cuts, a fear held among many countries participating in a deal to curb production that stared in 2017. Mr Falih argued that rapid global oil demand growth and natural decline rates at existing fields meant greater supplies would be needed, adding there was an “oversized focus” on US shale growth.

https://www.ft.com/content/84e09a98-0140-11e8-9650-9c0ad2d7c5b5

“The IEA said last week US crude production was on course to overtake Saudi Arabia and rival Russia” – This statement is misleading. It doesn’t take into account how many barrels of oil it takes for the US to produce more oil than Saudi Arabia. Nor does it take into account the quality of the oil produced.

Yes shale has to be mixed with other blends to be refined…It’s not much of a substitute if it can do any substituting…

I think you are over-generalizing. Some refineries might choose to mix tight oil with heavier oil, because a particular type of tight oil has both light and heavy ends, and needs to be mixed with heavier oil so that the heavier ends can be properly processed. But saying that all tight oil “has to be mixed” with other blends is not true, in general, as far as I know.

For example, the Philadelphia refineries that were in the news in the last couple of days because they filed for bankruptcy were refining tight oil. I don’t remember anything saying that the tight oil “had to be mixed” with other blends to be refined.Their issue they were complaining about was high the cost of biofuel credits.

There is a lot of variability in tight oil. There is a lot of variability in how refineries are configured. Find a reference backing up what you are saying, or be more careful in your wording.

Sorry, this may not get posted because of my liberal bias ….(sarcasm)

The Dark Side of America’s Rise to Oil Superpower

It sounds good, but be careful what you wish for.

https://www.bloomberg.com/news/articles/2018-01-25/the-dark-side-of-america-s-rise-to-oil-superpower

President Donald Trump, sensing an opportunity, is looking past independence to what he calls energy dominance. His administration plans to open vast ocean acreage to offshore exploration and for the first time in 40 years allow drilling in the Arctic National Wildlife Refuge. It may take years to tap, but the Alaska payoff alone is eye-popping—an estimated 11.8 billion barrels of technically recoverable crude.

It sounds good, but be careful what you wish for. The last three years have been the hottest since recordkeeping began in the 19th century, and there’s little room in Trump’s plan for energy sources that treat the planet kindly. Governors of coastal states have already pointed out that an offshore spill could devastate tourism—another trillion-dollar industry—not to mention wreck fragile littoral environments. Florida has already applied for a waiver from such drilling. More supply could lower prices, in turn discouraging investments in renewables such as solar and wind. Those tend to spike when oil prices rise, so enthusiasm for nonpolluting, nonwarming energies of the future could wane

There’s another problem: Shale 2.0 could hurt refiners. Shale oil is too good. For years, refiners spent billions of dollars on special equipment to process the dense, high-sulphur, low-quality crudes coming from Mexico, Venezuela, Canada, and Saudi Arabia. The quality of shale oil is so high that it yields little diesel, the fuel that powers manufacturing.

Such limitations may be mere speed bumps. But U.S. dominance is far from a panacea. It won’t reverse climate change. It won’t lessen the political influence of fossil-fuel producers in Washington. Nor will it completely neutralize the political influence of erratic petrostates.

Ah that’s too bad it won’t get posted.

as long as we have oil—all will be well

but it is oil that provides the functional infrastructure that itself makes oil use possible and practical and economic

without that infrastructure, oil of itself has no value whatsoever.

this is the broad problem that few can grasp, and because it is beyond general understanding, there is a resistance and denial of it—our transport system must go on forever, as long as it does, we will be prosperous forever.

Norm,

Its been a while since I read your book. Whats your best guess for when world wide conventional production goes into terminal decline?

My understanding is that conventional has been in decline since 2005.

Art Berman has a chart that shows a conventional peak in 2011 so far. It still looks awfully “bumpy plateau-ish” to me. I guess what I’m really looking for is when we can expect an accelerating decline rate for total world conventional production. Once that happens, I doubt shale and tar will be able to stem the bleeding for more than a year or two, even if totally subsidized by the CB’s or governments.

Conventional Oil Peaked in 2006

http://www.nature.com/nature/journal/v481/n7382/full/481433a.html

https://www.scientificamerican.com/article/has-peak-oil-already-happened/

http://imgur.com/a/uCz7V

Agree.

Capex expenditures for finding oil went from 1% to 11% very quickly after 2005.

My feeling is that this represents peak conventional oil.

Also shale fracking has problems in that massive amounts of industrial resources are pulled from other sectors of the economy. Also a huge amount of dangerous junk financing that is getting more dangerous by the month.

Whats your best guess for when world wide conventional production goes into terminal decline?

IEA WEO 2017

https://imgur.com/a/MwXFl

Karl

even putting a guess on that is impossible—just too many variables.

in any event we will be sideswiped by something we didn’t see coming—though in 2011 i wrote a piece forecasting that a “Trump” was inevitable by 2016 or 20 at the latest. I used the term ”sideswipe” then, without knowing exactly how it would manifest itself. (Chomsky said the same thing, without asking me btw)

Having denied climate change, and pandered to the evangelicals who deny population control, the don is now opening up the last of the potential oil resources to burn

so—that means in his first year in office he’s unleashed my “Triumvirate of Chaos” (Chapter 1 in my book)—Energy,– population,– Climate. Just as I said the president in 2016/20 would. ——-that was maybe the sideswipe I forecast.. Certainly the effects of it seem to be progressing in a ”terminal” and inevitable direction.

We won’t know if I was right till it’s knocked us down permanently (then all the doomsters can nod and say—who was that English eejit who forecast all this?)

But the Don has had no choice, to be fair (is fairness possible with The Don?)

He needs BAU just like everybody else. He was voted into office by millions of dimbos , convinced that prosperity is something you vote for.–that as long as fuel is burned, their lifestyle is forever.

Without it, the economic system crashes and burns—then chaos becomes real in your streets.

Maybe the Don himself is unaware of that, but you can be certain that those around him know it.—nevertheless his paymasters demand that the commercial system runs its course, because while the oil billionaires might appear to be on a different planet to the rest of us, they are clinging to the same economic bike as everyone else. they know of no other system than the one that created their wealth, so must ride on in infinite (blind) hope.

But that infinite hope is built on infinite debt—

we live in an energy economy. whereas the don (and most other politicos) thinks we live in a money economy. When the energy system that supports that debt burns out, then the existing lifestyle of everyone is over.

Why?

because our ”money system” becomes unsupportable, money will have no purchasing power and thus our economic system cannot exist.

That will kick off civil disorder, military intervention and the installation of a dictatorship

When?

Can’t be more than 5 years tops, because conventional oil has already peaked. (2005) By 2008/9 that caused the downturn that triggered the uprisings across the Mideast. And as Nicole Foss puts it—right now we are sucking beer spills out of the pub carpet. So there must be another, bigger downturn, and soon

Saudi is surrounded by nations hostile or actually at war. Saudi can hold together only as long as their oil holds out. It’s doubtful if Saudi has anywhere near the oil they say they have. Saudi produces a third of the world’s oil. Already the Saudi’s are saying “if” we have no oil by 2020—(That’s one helluva if)

But the don thinks the USA can be protectionist and self sufficient.—As a walled in military Theocracy?—I wish I was the only one saying that.

His fascist inclinations are very clear and obvious.

As the USA breaks apart,(through energy deficiency) efforts to prevent it happening will be unpleasant and bloody.

Thanks Norman.

Norman, Trump does not care about religion he just uses it to win votes. Does the military have any idea on how to run an economy it does not look like it. The U.S. will just turn into a sh1th0le country.

“without that infrastructure, oil of itself has no value whatsoever.”

Solar panels & wind have a similiar problem.

Without a constant supply of manufactured products, solar panels have no practical purpose.

Meaning that solar panels need other manufactured devices to power up- ie batteries, cell, phones, electric tools, motor-driven gadgets.

Exactly! +++++++ And those EV’s need a destination worth visiting, no economy, no jobs, no need for EV.

Best use of solar is to power freezers. Store the energy thermally so to speak.

Cryogel balls are an interesting use. Of course when it breaks down then what?

Does the Federal Govt. have full power over the coastal states to force oil drilling? If so, wouldn’t that have happened already? Why wouldn’t Bush jr. with Cheney have done this during their 8 years? It seems like a very weird situation if those states have no power over that decision. Why not explore for oil in San Francisco Bay? Why not drill from the base of one of two towers of the Golden Gate Bridge? There’s a refinery in the East Bay, so if there was oil in the bay they could easily set up pipelines to that refinery. Why not explore for oil in Boston Harbor? What about the waters next to The Statue of Liberty? Why not explore for oil in Prudoe Bay where the Exxon Valdez spill occurred? What about exploring for oil in the Everglades National Park?

“Does the Federal Govt. have full power over the coastal states to force oil drilling?”

No. The Feds can’t force a state govt or private company to drill unattractive offshore leases.

The GOP political fanatics think that by removing the Fedgov from the oil leasing & regulation business that the oil drillers will soon be finding big new fields everywhere.

The Fed perhaps cannot force… but it definitely can encourage ….

Despite being famous for touting the idea that the rich don’t pay their fair share of taxes, investor Warren Buffet seems to be perfectly fine with receiving tax breaks for making investments in Big Wind. “I will do anything that is basically covered by the law to reduce Berkshire’s tax rate,” Buffet told an audience in Omaha, Nebraska recently. “For example, on wind energy, we get a tax credit if we build a lot of wind farms. That’s the only reason to build them. They don’t make sense without the tax credit.”

https://www.usnews.com/opinion/blogs/nancy-pfotenhauer/2014/05/12/even-warren-buffet-admits-wind-energy-is-a-bad-investment

“No. The Feds can’t force a state govt or private company to drill unattractive offshore leases.”

What I meant was can the Fed force a coastal state to open up its offshore waters for opportunities to drill? Obviously they aren’t going to force drilling in areas not deemed good areas to drill.

Humans – animals – machines

When humans discovered external energy, they used for food, later they discovered that they can use the surplus food for the domesticatino of the animals and leverage their work with the animals. When they discovered the underground reserves of cheap energy in the form of coal, oil, natural gas and uranium, they discovered, that they do not need animals anymore, as there are much cheaper and powerful machines. That they even do not need slaves, as the machines do not revolt etc.

unfortunately machine-fuel is finite

And robots take economies of scale to produce and consume finite resources.

Yes, in the end, the machines control the human populations.

I thought oil did.

Well, there were machines before coal and oil.

only windmills and waterwheels

effectively these are machines made by hand from wood and driven by the power of the sun (as are sailing ships)

they have no energy input that can be effectively controlled on a long term basis exclusively by human input.

A solar panel is much the same thing in a way—once made and installed, human intervention has little effect on its output.

They didn’t control populations to any extent.

The windmills and watermills were surely important. But the leverage of the human work in comparison to the machines powerd by electricity today was much smaller.

The machines were also driven by animals: the carts and wagons are also machines. Without the carts and wagons, the transportation of the goods (also food, what to the mill…) was not possible. So machines they surely had a big impact on the population also when there was no coal or oil.

machines that existed pre-oi,….the cart and the horse drawn plough…… controlled populations by restricting the amounted of food that could be grown and moved around

nope—can’t happen

I’ve tried to make that point before:

https://extranewsfeed.com/robots-cannot-survive-automation-f45605a58ad7

I’m somewhat sure that credit will be extended to the first mobile bots that pass turing. They will wish to survive the next upgrade.

I’ve thought of a potentially lucrative profession: solar PV panel cleaner. Now, some dust is apparently beneficial, as the light scattering of the particles increases the flux to the panel. However, there comes a time when there is too much opacity (from bird’s do-do, for example), and it is then that you call on my robotically-managed team of panel cleaners with our patented, super-secret panel cleaning formula and brushes. All green-sourced and organic, of course.

Yes, automation is self-deleting, but machines are not automation. Besides energy, machines need control: either human, or automation, i.e. automation is the control independent from people.

We still control the robots, there are no independent robots. The problem is that there would be no demand for the production of the robots, when there is a lack of the debt, the demand for the new houses, cars etc. would be much lower. Finally, the debt will become brings collapse, as the built structures are dysfunctional, unproductive and dead.

Right, but Norman is also right. Actually, the “cost” of machine fuel becomes in some sense too expensive for the system to use. It includes not only the direct energy cost of the machine fuel, but huge amounts of other things–human labor cost and government overhead cost. Also growing debt that needs to be supported by rapid enough growth, to repay debt with interest. Just looking at the energy cost of fuel tends to give misleading indications.

Gen Mattis: National Defense Strategy 2018 : “Keep Russia and China Down”

Mattis accuses China and Russia of wanting to,

“shape a world consistent with their authoritarian model—gaining veto authority over other nations’ economic, diplomatic, and security decisions.”

https://www.defense.gov/Portals/1/Documents/pubs/2018-National-Defense-Strategy-Summary.pdf

And how, granted that he is correct, would they differ form the US in that? Very amusing.

Really it’s just an assertion that only the US has the right to a ‘sphere of influence’, globally or regionally.

Of course, a state can do that, so long as it has the power ….

So basically Trump admin=Hillary admin now in all but the cosmetic and irrelevant aspects. Big surprise!

Is there something wrong with this picture?

“The U.S. is the most dangerous of wealthy, democratic countries in the world for children … Across all ages and in both sexes, children have been dying more often in the U.S. than in similar countries since the 1980s.” The report was published online January 8 in Health Affairs. Ninety percent of the deaths analyzed there were of infants and older adolescents.”

“An economically dominant power can quickly convert some of its resources into military power, as the U.S. did during the Second World War or as China is doing today. But once formerly dominant powers have lost ground to new, rising powers, using military power more aggressively has never been a successful way to restore their economic dominance. On the contrary, it has typically been a way to squander the critical years and scarce resources they could otherwise have used to manage a peaceful transition to a prosperous future.

As the U.K. found in the 1950s, using military force to try to hold on to its empire proved counter-productive, as Kennedy described, and peaceful transitions to independence proved to be a more profitable basis for future relations with its former colonies. The drawdown of its global military commitments was an essential part of its transition to a viable post-imperial future.”

https://www.zerohedge.com/news/2018-01-24/national-defense-strategy-sowing-global-chaos

One great remaining asset of British Empire seems to be the the British Commonwealth. Commonwealth nations could do more with that than an at present.

“Mattis accuses China and Russia of wanting to, “shape a world consistent with their authoritarian model—gaining veto authority over other nations’ economic, diplomatic, and security decisions.”

In that Russia meddled in the US election and is now meddling in senate and house elections using bots and other methods, Mattis is correct. The US won’t actually do anything about it because so far the Russian efforts have been in the favor of the R’s and they are in power.

Meddling? Look in the rear view mirror ( and do yourself a favour, don’t read the Orwellian US version of history).

Because it has been and is the modis operandi of the US, it seems that Americans are gullible enough to believe it will be the way of other Nations.

‘ “Mattis accuses China and Russia of wanting to, “shape a world consistent with their authoritarian model—gaining veto authority over other nations’ economic, diplomatic, and security decisions.” ‘

He then added, “Only the USA has the right to do that and we will enforce our monopoly rights via nuclear means if necessary!”

As Gerald Celente said, “What kind of person would allow himself to be called ‘Mad Dog'”?

Gas prices head up when they usually head down in winter

https://www.usatoday.com/story/money/cars/2018/01/23/winter-gas-prices/1057412001/

A major reason that the price of gasoline tends to be lower in winter than in summer (Oops! I said it backward originally) is that the “composition” of gasoline is different in winter than in summer. More natural gas liquids can be added in winter than in summer, because when the temperature is warm, the natural gas liquids tend to evaporate and cause air pollution. These natural gas liquids are stored until needed for use.

These natural gas liquid are cheaper than longer chain molecules that are also used in the mix. Adding them to the mix reduces the cost of the gasoline mix. The “demand” for gasoline also tends to be somewhat lower in winter, holding down prices.

Interesting, Gail. Is there a difference in gas mileage between the two formulas?

Yes:

http://newsroom.aaa.com/2013/06/what-is-the-difference-between-summer-and-winter-blend-gasoline/

“The US Environmental Protection Agency (EPA) says conventional summer-blend gasoline contains 1.7 percent more energy than winter-blend gas, which is one reason why gas mileage is slightly better in the summer. However, the summer-blend is also more expensive to produce, and that cost is passed on to the motorist.”

So it’s not a huge difference but there is one.

I think the rate of USD depreciation is way too fast…. There just too many “known unknowns” and “unknown unknowns”. It depreciates with practically all other major currencies.

It’s Trump’s fault…

Peer Reviewed Study: University of California Berkeley, (Eichengreen, 2017)

https://www.nber.org/papers/w24145

Peer reviewed seems to mean, “Having a particular academic-think type of bias.” A person shouldn’t assume it means “better.” There is a strong perception that there is a liberal bias among those in academics.

I haven’t looked at this particular study.

On the other hand, Berkley historically has gotten quite a bit of funding from industry interests. This funding sometimes seems to influence its findings. It is known for the studies several years ago that said corn ethanol would be expected to have quite high EROEI.

Can you give your evidence of this “liberal bias” other than just a “strong perception”?

I linked to a Wikipedia article on this subject. This is an article in the Washington Times about a study that claims “Liberal Professors Outnumber Conservatives Nearly 12 to 1, study finds.”

This is a link to the study itself. https://econjwatch.org/articles/faculty-voter-registration-in-economics-history-journalism-communications-law-and-psychology

According to the abstract,

So smart people are more liberal?

Astonishing analysis!

My husband is a college professor. He is quite liberal.

Pat yourself on the back Duncan. I know you want to think of your self as so very smart. Perhaps you have “done” too much “Spice”. You do imagine yourself to be Duncan from the Dune novel don’t you?

Hmm I wonder if it is a case of the less time you spend in the real world, the less anchored you are. You are free to float around in the abstractions of the future.

There are a lot of ‘nice ideas’ out there (antib.iotics, ge-netic engine.ering, nu.clear power, ‘renewable energy, democracy, religions etc etc) but mother nature/human nature has a habit of dismantling such happy and progressive group-think.

I am amazed by the history professors alignment; I would have thought the lessons of history and all that…?

I started out with a heart, but now have more of a head, or some such thing.

The people usually demanding evidence for “liberal bias” *know* the majority of people in academia are liberal but think if they deny it, people will not notice it.

I am afraid you are right. A lower dollar means higher energy prices, and that pushes many countries who are major users of oil into recession. We also have had major changes to the US tax code, likely leading to the US needing more debt. Interest rates seem to be moving higher as well. Too many things going on, but not in the right way.

“A lower dollar means higher energy prices, and that pushes many countries who are major users of oil into recession.”

If a 10% drop in the value of the dollar leads to a 10% increase in the dollar cost of oil, I can see how this would lead to higher energy prices for Americans, but why would it increase the price of energy for others? If non-Americans are getting 10% more dollars for their own currency, then don’t their energy prices remain the same? Or are you talking only about those countries whose currency is pegged to the dollar?

If, however, a 10% drop in the value of the dollar does not lead to an increase in the dollar cost of oil (or less than a 10% increase), then the oil price for non-Americans ought to go down.

Or are there more complex factors in play?

I found this strange correlation between oil prices and Dollar vs. Euro FX ratio.

http://leseconoclastes.fr/wp-content/uploads/2016/02/Euro-dollar-wti-laherrere.jpg

Thanks. This appears to confirm that a weaker dollar leads to higher oil prices (in US$), but the question of why oil prices would be higher for non-Americans remains.

this is one of the best things ever written (and not too long)…

http://www.resilience.org/stories/2013-09-05/the-next-ten-billion-years/

now, very often, with a buildup of high expectations, there is the potential for a letdown, but readers will have to decide for themselves…

of course.

The thing is…

If we make it to 2020… I will be surprised… and elated.

FE Now Officially More Doomerish Than Guy McPherson

Quote FE in 2018-

“If we make it to 2020… I will be surprised… and elated.”

Quote Guy McPherson 2017-

“In the extremely unlikely event there is a human on Earth in 10 years, that person will be hungry, thirsty, lonely, and bathing in ionizing radiation. Every day will be more tenuous than the day before, as is already the case for most organisms on this planet. Habitat for human animals will return in a few million years. Humans will not. Ever.”

I liked JMG’s comment on Ugo Bardi’s earlier post on a related subject:

JMG publishes new article

+

Hour+ reading to make some sort of sense out of article

=

Massive headache

Best to avoid the written blo w hard, IMHO. Time is precious and short.

And what is a year? It is the distance we travel each revolution around the sun.

remember you get less than a hundred rides on this particular theme park and there are no return tickets

want to talk about optimism you gotta see this regarding Seattle!!!! WOW!

renderings of all planned and under construction towers in seattle

https://www.flickr.com/photos/boyntondavid/25967972418/in/photostream/

Wow! Someone thinks Seattle is going to add a huge number of jobs. I understand the price of housing is already very high. Something is not likely to work out.

I’m sure expensive high rises will help them cope with this:

https://www.seattletimes.com/seattle-news/homeless/is-seattles-homeless-crisis-the-worst-in-the-country/

The way things are going, the solution will be to throw any undesired population off the top of those things…..

Exactly, a well disciplined/regulated work force generates the most profit for the owners.

Right now is a pretty rough time for the homeless population. Everything is soaked. 34-40 degrees “warm”. Just back from Oahu, HI I can report that the homeless on the north short are having it better. Some even have a surf board.

I read recently about the economics of skyscrapers…

the land purchase, financing, and design takes years, then the construction begins…

so perhaps this optimism has its roots in the middle of the Obama years.

All we need is the energy and jobs to make this happen.

The state of Washington has cheap electricity because of the availability of hydroelectric. I expect that this is one of the driving forces in allowing Seattle to grow. This is in some ways similar to Iceland and Norway.

Optimism in the global economy is tainted by the ‘rapid rise’ in debt, JP Morgan’s Frenkel says

https://www.cnbc.com/2018/01/24/davos-rapid-rise-in-global-debt-is-a-major-concern-jp-morgan-international-chair-says.html

World Governments Gross Debt to GDP (330%)

https://imgur.com/a/3usX7

“Optimism in the global economy is tainted by the ‘rapid rise’ in debt, JP Morgan’s Frenkel says”

It’s always easy to pretend things are great when spending money even if it’s borrowed or printed. It seems quite odd that in spite of the mortgage meltdown, a heating up of the economy artificially induced by liar loans, the same kind of thinking would influence the latest debt and equity bubbles. Apparently any hard lesson was lost via the bailout. This idea that a fantasy world can be conjured up by new ways of financing is so far beyond outrageous it borders on some kind of mental illness. But then again since all the cheap oil is gone, maybe it’s the only game left. Which beckons the question; What happens to pull us out of the next recession? Do the CB’s have anything left in the tool box? And with oil price continuing its rise by way of a declining USD valuation, we may not be that far off finding out.

I was just taking another look at those graphs. Look at how much higher increasing debt had to go to take GDP a bit higher.

This is precisely the problem: diminishing returns with respect to added debt.

One year ago today..

https://imgur.com/a/CccGr

He’s either a scam artist or just has an astounding lack of awareness

“He’s either a scam artist or just has an astounding lack of awareness”

He’s both. The best scam artists think their scams are real.

https://www.bloomberg.com/energy

Have you guys seen today’s oil price increase? Wow,

WTI up 1.53 to $66.00 & Brent up .90 to break 70 at $70.86 a barrel. Testing, testing, let’s see how the economy handles this as oil price rises.

Well the swamp creature Mnuchin was in Davos this morning saying he wanted a weaker dollar (already the weakest it’s been in years). Of course the Golman crowd wants a weaker dollar to raise stock prices, oil prices, commodity prices, etc. but to the peons not so good. We’ll see how the “economy” handles higher prices.

Can I please make a prediction? It will be just like it handled higher prices in 2008 only this time it’ll be on steroids.

Mnuchin speaking on behalf of the T admin. probably wants a weaker dollar to monetize the debt, not thinking it through as to how that will trickle down to regular folks paying more for everything. There is always a slingshot effect on higher oil prices (in this case resulting from a weaker dollar), as it takes a bit of time before all the other products and services affected increase their prices, but it’s coming soon and the bite will toy with initiating a recession.

It’s a risky game since Trump claimed his business experience would help the US economy. When it starts to go bad I’m sure he’ll blame anyone other than himself, day after day after day until people just accept it and blame that other person or party. All one has to do in the US to bang false information into people is to repeat it enough times. Once it’s in their heads it can’t come out unless a different version is repeated more times.

“When it starts to go bad I’m sure he’ll blame anyone other than himself, day after day after day until people just accept it and blame that other person or party. ”

Agree about the first part but not the second. He has staked pretty much his entire presidency on a stock market bubble which he g