Financial markets have been behaving in a very turbulent manner in the last couple of months. The issue, as I see it, is that the world economy is gradually changing from a growth mode to a mode of shrinkage. This is something like a ship changing course, from going in one direction to going in reverse. The system acts as if the brakes are being very forcefully applied, and reaction of the economy is to almost shake.

What seems to be happening is that the world economy is reaching Limits to Growth, as predicted in the computer simulations modeled in the 1972 book, The Limits to Growth. In fact, the base model of that set of simulations indicated that peak industrial output per capita might be reached right about now. Peak food per capita might be reached about the same time. I have added a dotted line to the forecast from this model, indicating where the economy seems to be in 2019, relative to the base model.1

Figure 1. Base scenario from The Limits to Growth, printed using today’s graphics by Charles Hall and John Day in Revisiting Limits to Growth After Peak Oil with dotted line at 2019 added by author. The 2019 line is drawn based on where the world economy seems to be now, rather than on precisely where the base model would put the year 2019.

The economy is a self-organizing structure that operates under the laws of physics. Many people have thought that when the world economy reaches limits, the limits would be of the form of high prices and “running out” of oil. This represents an overly simple understanding of how the system works. What we should really expect, and in fact, what we are now beginning to see, is production cuts in finished goods made by the industrial system, such as cell phones and automobiles, because of affordability issues. Indirectly, these affordability issues lead to low commodity prices and low profitability for commodity producers. For example:

- The sale of Chinese private passenger vehicles for the year of 2018 through November is down by 2.8%, with November sales off by 16.1%. Most analysts are forecasting this trend of contracting sales to continue into 2019. Lower sales seem to reflect affordability issues.

- Saudi Arabia plans to cut oil production by 800,000 barrels per day from the November 2018 level, to try to raise oil prices. Profits are too low at current prices.

- Coal is reported not to have an economic future in Australia, partly because of competition from subsidized renewables and partly because China and India want to prop up the prices of coal from their own coal mines.

The Significance of Trump’s Tariffs

If a person looks at history, it becomes clear that tariffs are a standard response to a problem of shrinking food or industrial output per capita. Tariffs were put in place in the 1920s in the time leading up to the Great Depression, and were investigated after the Panic of 1857, which seems to have indirectly led to the US Civil War.

Whenever an economy produces less industrial or food output per capita there is an allocation problem: who gets cut off from buying output similar to the amount that they previously purchased? Tariffs are a standard way that a relatively strong economy tries to gain an advantage over weaker economies. Tariffs are intended to help the citizens of the strong economy maintain their previous quantity of goods and services, even as other economies are forced to get along with less.

I see Trump’s trade policies primarily as evidence of an underlying problem, namely, the falling affordability of goods and services for a major segment of the population. Thus, Trump’s tariffs are one of the pieces of evidence that lead me to believe that the world economy is reaching Limits to Growth.

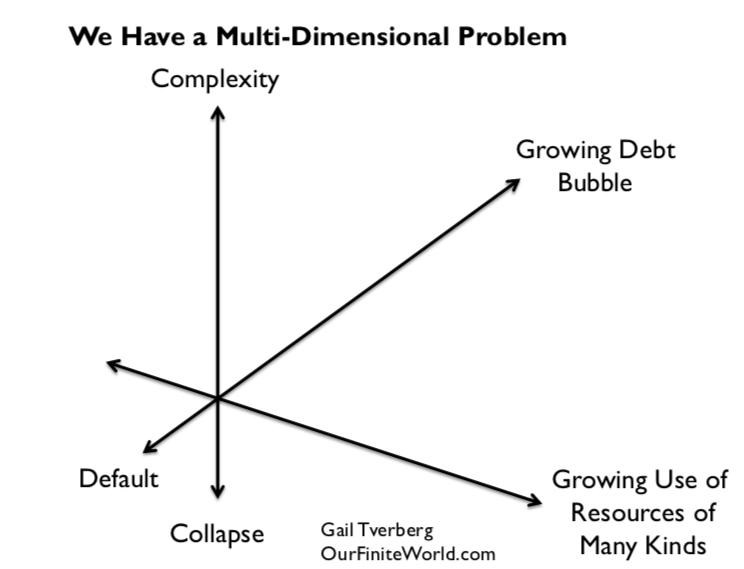

The Nature of World Economic Growth

Economic growth seems to require growth in three dimensions (a) Complexity, (b) Debt Bubble, and (c) Use of Resources. Today, the world economy seems to be reaching limits in all three of these dimensions (Figure 2).

Figure 2.

Complexity involves adding more technology, more international trade and more specialization. Its downside is that it indirectly tends to reduce affordability of finished end products because of growing wage disparity; many non-elite workers have wages that are too low to afford very much of the output of the economy. As more complexity is added, wage disparity tends to increase. International wage competition makes the situation worse.

A growing debt bubble can help keep commodity prices up because a rising amount of debt can indirectly provide more demand for goods and services. For example, if there is growing debt, it can be used to buy homes, cars, and vacation travel, all of which require oil and other energy consumption.

If debt levels become too high, or if regulators decide to raise short-term interest rates as a method of slowing the economy, the debt bubble is in danger of collapsing. A collapsing debt bubble tends to lead to recession and falling commodity prices. Commodity prices fell dramatically in the second half of 2008. Prices now seem to be headed downward again, starting in October 2018.

Figure 3. Brent oil prices with what appear to be debt bubble collapses marked.

Figure 4. Three-month treasury secondary market rates compared to 10-year treasuries from FRED, with points where short term interest rates exceed long term rates marked by author with arrows.

Even the relatively slow recent rise in short-term interest rates (Figure 4) seems to be producing a decrease in oil prices (Figure 3) in a way that a person might expect from a debt bubble collapse. The sale of US Quantitative Easing assets at the same time that interest rates have been rising no doubt adds to the problem of falling oil prices and volatile stock markets. The gray bars in Figure 4 indicate recessions.

Growing use of resources becomes increasingly problematic for two reasons. One is population growth. As population rises, the economy needs more food to feed the growing population. This leads to the need for more complexity (irrigation, better seed, fertilizer, world trade) to feed the growing world population.

The other problem with growing use of resources is diminishing returns, leading to the rising cost of extracting commodities over time. Diminishing returns occur because producers tend to extract the cheapest to extract commodities first, leaving in place the commodities requiring deeper wells or more processing. Even water has this difficulty. At times, desalination, at very high cost, is needed to obtain sufficient fresh water for a growing population.

Why Inadequate Energy Supplies Lead to Low Oil Prices Rather than High

In the last section, I discussed the cost of producing commodities of many kinds rising because of diminishing returns. Higher costs should lead to higher prices, shouldn’t they?

Strangely enough, higher costs translate to higher prices only sometimes. When energy consumption per capita is rising rapidly (peaks of red areas on Figure 5), rising costs do seem to translate to rising prices. Spiking oil prices were experienced several times: 1917 to 1920; 1974 to 1982; 2004 to mid 2008; and 2011 to 2014. All of these high oil prices occurred toward the end of the red peaks on Figure 5. In fact, these high oil prices (as well as other high commodity prices that tend to rise at the same time as oil prices) are likely what brought growth in energy consumption down. The prices of goods and services made with these commodities became unaffordable for lower-wage workers, indirectly decreasing the growth rate in energy products consumed.

Figure 5.

The red peaks represented periods of very rapid growth, fed by growing supplies of very cheap energy: coal and hydroelectricity in the Electrification and Early Mechanization period, oil in the Postwar Boom, and coal in the China period. With low energy prices, many countries were able to expand their economies simultaneously, keeping demand high. The Postwar Boom also reflected the addition of many women to the labor force, increasing the ability of families to afford second cars and nicer homes.

Rapidly growing energy consumption allowed per capita output of both food (with meat protein given a higher count than carbohydrates) and industrial products to grow rapidly during these peaks. The reason that output of these products could grow is because the laws of physics require energy consumption for heat, transportation, refrigeration and other processes required by industrialization and farming. In these boom periods, higher energy costs were easy to pass on. Eventually the higher energy costs “caught up with” the economy, and pushed growth in energy consumption per capita down, putting an end to the peaks.

Figure 6 shows Figure 5 with the valleys labeled, instead of the peaks.

Figure 6.

When I say that the world economy is reaching “peak industrial output per capita” and “peak food per capita,” this represents the opposite of a rapidly growing economy. In fact, if the world is reaching Limits to Growth, the situation is even worse than all of the labeled valleys on Figure 6. In such a case, energy consumption growth is likely to shrink so low that even the blue area (population growth) turns negative.

In such a situation, the big problem is “not enough to go around.” While cost increases due to diminishing returns could easily be passed along when growth in industrial and food output per capita were rapidly rising (the Figure 5 situation), this ability seems to disappear when the economy is near limits. Part of the problem is that the lower growth in per capita energy affects the kinds of jobs that are available. With low energy consumption growth, many of the jobs that are available are service jobs that do not pay well. Wage disparity becomes an increasing problem.

When wage disparity grows, the share of low wage workers rises. If businesses try to pass along their higher costs of production, they encounter market resistance because lower wage workers cannot afford the finished goods made with high cost energy products. For example, auto and iPhone sales in China decline. The lack of Chinese demand tends to lead to a drop in demand for the many commodities used in manufacturing these goods, including both energy products and metals. Because there is very little storage capacity for commodities, a small decline in demand tends to lead to quite a large decline in prices. Even a small decline in China’s demand for energy products can lead to a big decline in oil prices.

Strange as it may seem, the economy ends up with low oil prices, rather than high oil prices, being the problem. Other commodity prices tend to be low as well.

What Is Ahead, If We Are Reaching Economic Growth Limits?

1. Figure 1 at the top of this post seems to give an indication of what is ahead after 2019, but this forecast cannot be relied on. A major issue is that the limited model used at that time did not include the financial system or debt. Even if the model seems to provide a reasonably accurate estimate of when limits will hit, it won’t necessarily give a correct view of what the impact of limits will be on the rest of the economy, after limits hit. The authors, in fact, have said that the model should not be expected to provide reliable indications regarding how the economy will behave after limits have started to have an impact on economic output.

2. As indicated in the title of this post, considerable financial volatility can be expected in 2019 if the economy is trying to slow itself. Stock prices will be erratic; interest rates will be erratic; currency relativities will tend to bounce around. The likelihood that derivatives will cause major problems for banks will rise because derivatives tend to assume more stability in values than now seems to be the case. Increasing problems with derivatives raises the risk of bank failure.

3. The world economy doesn’t necessarily fail all at once. Instead, pieces that are, in some sense, “less efficient” users of energy may shrink back. During the Great Recession of 2008-2009, the countries that seemed to be most affected were countries such as Greece, Spain, and Italy that depend on oil for a disproportionately large share of their total energy consumption. China and India, with energy mixes dominated by coal, were much less affected.

Figure 7. Oil consumption as a percentage of total energy consumption, based on 2018 BP Statistical Review of World Energy data.

Figure 8. Energy consumption per capita for selected areas, based on energy consumption data from 2018 BP Statistical Review of World Energy and United Nations 2017 Population Estimates by Country.

In the 2002-2008 period, oil prices were rising faster than prices of other fossil fuels. This tended to make countries using a high share of oil in their energy mix less competitive in the world market. The low labor costs of China and India gave these countries another advantage. By the end of 2007, China’s energy consumption per capita had risen to a point where it almost matched the (now lower) energy consumption of the European countries shown. China, with its low energy costs, seems to have “eaten the lunch” of some of its European competitors.

In 2019 and the years that follow, some countries may fare at least somewhat better than others. The United States, for now, seems to be faring better than many other parts of the world.

4. While we have been depending upon China to be a leader in economic growth, China’s growth is already faltering and may turn to contraction in the near future. One reason is an energy problem: China’s coal production has fallen because many of its coal mines have been closed due to lack of profitability. As a result, China’s need for imported energy (difference between black line and top of energy production stack) has been growing rapidly. China is now the largest importer of oil, coal, and natural gas in the world. It is very vulnerable to tariffs and to lack of available supplies for import.

Figure 9. China energy production by fuel plus its total energy consumption, based on BP Statistical Review of World Energy 2018 data.

A second issue is that demographics are working against China; its working-age population already seems to be shrinking. A third reason why China is vulnerable to economic difficulties is because of its growing debt level. Debt becomes difficult to repay with interest if the economy slows.

5. Oil exporters such as Venezuela, Saudi Arabia, and Nigeria have become vulnerable to government overthrow or collapse because of low world oil prices since 2014. If the central government of one or more of these exporters disappears, it is possible that the pieces of the country will struggle along, producing a lower amount of oil, as Libya has done in recent years. It is also possible that another larger country will attempt to take over the failing production of the country and secure the output for itself.

6. Epidemics become increasingly likely, especially in countries with serious financial problems, such as Yemen, Syria, and Venezuela. Historically, much of the decrease in population in countries with collapsing economies has come from epidemics. Of course, epidemics can spread across national boundaries, exporting the problems elsewhere.

7. Resource wars become increasingly likely. These can be local wars, perhaps over the availability of water. They can also be large, international wars. The timing of World War I and World War II make it seem likely that these wars were both resource wars.

Figure 10.

8. Collapsing intergovernmental agencies, such as the European Union, the World Trade Organization, and the International Monetary Fund, seem likely. The United Kingdom’s planned exit from the European Union in 2019 is a step toward dissolving the European Union.

9. Privately funded pension funds will increasingly be subject to default because of continued low interest rates. Some governments may choose to cut back the amounts they provide to pensioners because governments cannot collect adequate tax revenue for this purpose. Some countries may purposely shut down parts of their governments, in an attempt to hold down government spending.

10. A far worse and more permanent recession than that of the Great Recession seems likely because of the difficulty in repaying debt with interest in a shrinking economy. It is not clear when such a recession will start. It could start later in 2019, or perhaps it may wait until 2020. As with the Great Recession, some countries will be affected more than others. Eventually, because of the interconnected nature of financial systems, all countries are likely to be drawn in.

Summary

It is not entirely clear exactly what is ahead if we are reaching Limits to Growth. Perhaps that is for the best. If we cannot do anything about it, worrying about the many details of what is ahead is not the best for anyone’s mental health. While it is possible that this is an end point for the human race, this is not certain, by any means. There have been many amazing coincidences over the past 4 billion years that have allowed life to continue to evolve on this planet. More of these coincidences may be ahead. We also know that humans lived through past ice ages. They likely can live through other kinds of adversity, including worldwide economic collapse.

Note:

[1] Note that where the dotted line for 2019 is placed is based on where I see the 2019 economy relative to the downturn in industrial output per capita, based on a number of kinds of evidence, not all of which is cited in this article. The 1972 base model would give a slightly different timing of the downturn, a few years earlier. Also note that while the original “The Limits to Growth” book is no longer in print, Limits to Growth: The 30-Year Update by the same authors is available for sale.

@Davidin100Million… ans all:

If the economy is dependend on growth, and growth is dependend on increasing fossil energy input, and we are soon faced to peak oil because of the falling output of shale oil, how can we make it until 2030? It looks like we are just now at the beginning of a deflationary depression what will destroy the house of cards much earlier.

Saludos

el mar

It looks to me that way as well. There are an awfully lot of interconnected systems that threaten to fail in a slowdown. In fact, a slowdown in China’s coal production is just as important, or more important, than peak oil in this regard. International trade needs to contract. The promises made to pensioners seem unlikely to be payable. Many debt defaults seem likely to be ahead.

Thank you Gail. That sounds logical to me. And that is wy we feel the nervous vibrations caused by the bow wave of the starting deflation all over the world. From Trump over Brexit to yellow vests and Bolsonaro ….

There are different phases in response to terminality. Bargaining is one of them.

https://www.nytimes.com/2019/01/27/upshot/world-economy-low-growth-low-interest-deflation.html

“The World Economy Just Can’t Escape Its Low-Growth, Low Inflation Rut.” I agree. This is what collapse looks like.

Russia-Saudi alliance abandons assault on US shale as oil supply crunch looms

The oil alliance of Opec and Russia has abandoned efforts to drive US shale out of the global energy market, accepting the hard reality of America’s irrepressible frackers for years to come.

“To really fight shale we’d need oil below $40 a barrel,” said Kirill Dmitriev, head of Russia’s wealth fund.

“That is not good for the Russian economy and it is not good for the Saudi economy. It is not practical, and we are not going to try to fight it,” he told the World Economic Forum in Davos.

A string of Opec members would risk incipient insolvency if there were another oil price war along the lines of 2014-2016. Saudi Arabia’s ruling dynasty would struggle to maintain its cradle-to-grave welfare model needed to head off political dissent.

Mr Dmitriev, a key architect of Russia’s oil strategy, said his country was working tightly with the Opec cartel and was now pursuing prices of $60 to $70, deemed the optimal range needed to ensure long-term stability.

Brent crude has crept up into the bottom of this range after a dramatic sell-off in October and November on global recession fears and a soft US line on Iranian sanctions. The Opec-Russia deal last month to trim output by 800,000 barrels a day (b/d) has restored balance to the market.

Surging shale output in the Permian Basin lifted US output by 2m b/d last year, an increase alone equal to the entire production of Mexico.

The US has pulled ahead of Russia and Saudi Arabia to become the world’s biggest producer of crude at 11.7m b/d, a feat made possible by America’s deep capital markets and $50bn of equity financing for wildcat projects.

Vicki Hollub, chief executive of Occidental, said the Permian was an astonishingly prolific basin with multiple layers of rich resources. Seismic imaging, multi-pad drills, and longer lateral bores have radically changed the economics of the industry.

“We’ve driven down the breakeven price of much of the Permian to less than $40, and in some cases even to $30, so there is still going to be a lot of opportunity to grow,” she said.

This time investors will be more disciplined. “They have been burned and are much more cautious now. Investors are going to hold companies to account,” she said.

Fatih Birol, head of the International Energy Agency, said new pipelines in Texas would unblock a major bottleneck by the end of this year, opening the way for a fresh flood of US shale into world markets. “We’ve not seen the full impact of shale yet. The second wave is on its way,” he said.

Dr Birol said it was perfectly plausible that the US would raise output by a further 10m b/d over the next decade. This would entirely change the geopolitical prospects of Russia and the Middle East.

John Hess, founder of Hess Petroleum, said the US would keep growing to 15m b/d but then start to hit all kinds of constraints. “Shale is about 6pc of world oil supply now, and it probably will go up to 10pc by mid-decade. Then it flattens out,” he said.

“Resources start to degrade. Eventually you get to locations that aren’t as attractive as the ones we’re drilling right now. So shale is not the next Saudi Arabia but at the end of the day it is an important component of short-cycle supply,” he said.

Supply shortfall

Mr Hess said the problem was that global spending in conventional long-term projects had collapsed. This is setting the stage for a serious crunch in the future.

The world needs new capex investment in oil and gas of $580bn each year to stand still. It spent just $350bn in 2016, $370bn in 2017, and $410bn in 2018. The effects of this shortfall are not yet visible in world supply. They soon will be.

Majid Jafar, head of Crescent Petroleum in Dubai, said natural attrition was relentlessly eroding future supply. “There is chronic under-investment and a natural decline of 3m to 4m barrels a day. We need to add a new Iraq each year,” he said.

Mr Jafar warned of a coming supply crisis within five years. The paradox of oil today is that even though the spot market is well supplied and Opec is holding back output, spare capacity is actually at wafer thin levels.

This is an accident waiting to happen and there are geopolitical stress points all over the world. Venezuela’s Maduro regime is now in its final agonies, raising a lot of questions about $50bn of debts to China and $17bn owed to Russia.

Venezuela has slashed output by two thirds to 1.1m b/d. “It is the biggest drop in the history of the oil market for a medium producer,” said Dr Birol.

Mr Jafar said that ultimately the global oil industry should be grateful to Texas frackers. “We don’t see US shale as a threat at all.

That of course has reduced the economic urgency of renewable energy, which is what the Mid-East producers fear even more. It is why environmentalists view shale with such deep suspicion.

https://www.telegraph.co.uk/business/2019/01/25/russia-saudi-alliance-reaches-truce-us-shale-oil-supply-crunch/

https://i.imgur.com/BwSPCg5.jpg

I think we have a new name—–

This is an oldie by now, but it’s still valid:

May 3, 2018

The Democrats’ favorite sport: Ruining people

By Patricia McCarthy

Vince Foster, Hillary’s lawyer friend from Arkansas who died by his own hand in 1993, once said of Washington, D.C., “Here, ruining people is considered sport.” He had learned the hard way how brutal is the game of politics, especially if one works for the Clintons. What Ted Kennedy did to Judge Robert Bork to keep him off the Supreme Court in 1986 was a disgusting and vicious perversion of the Constitution. What they did to Clarence Thomas in 1991, with Joe Biden in the Kennedy role, was beyond the pale and certainly racist; as we still see today, the left cannot allow black Americans to be conservative, especially one as brilliant as Thomas. As the Clintons came to dominate and control the Democratic Party from 1992 on, the game became more sinister and more dangerous.

Over the past twenty-six years, the virus that is the Clintons on the American body politic has metastasized into a virulent auto-immune disease. They are a virus that seeks to utterly destroy what it sees as an enemy but may well end up demolishing itself, with devastating results. With Trump’s win, this virus amped up its attack on all things Trump: his supporters, his agenda, his family, his friends, and his Cabinet and staff. So intent on getting and keeping power and massive amounts of ill gotten riches were they that the American people chose, once and for all, to reject Hillary and to inoculate themselves from further damage at the hands of the Clintons and their sycophants.

But a disease for which only half of the antibiotics are given becomes angrier and even stronger. The Democratic Party today has moved so far to the left, become so radicalized, that it is a blight on the American landscape. Its favored strategy is to destroy everything, anyone, and anything that stands in its way – thus the Mueller witch hunt that has cost so many so much. Gen. Flynn has lost his house. Michael Cohen’s homes and office were raided. Michael Caputo, a “witness,” let the Senate committee know what he thinks when he said to them, “God [d—] you to Hell.” It remains to be seen if the DOJ I.G. report we await will tell the true story of their diabolical contempt for all that is good about this nation.

The collusion-with-Russia hoax has been effectively exposed for what it was and is: a plan devised to overturn the results of the 2016 election. Only the blinkered media and their counterparts in Congress fail to see that their plan has not only backfired, but boomeranged. We know the plan was to get Flynn, then do the same to Trump (McCabe).

The Democrats have tried to block all of Trump’s nominees to his Cabinet, to the courts, to ambassadorships but have failed for the most part. This past week, they slimed Rear Admiral Ronny Jackson, the White House physician to the Obamas and Bushes, after Trump nominated him to head up the V.A. Sen. Tester accused the man of a long list of bad acts, none of which is true. They want Scott Pruitt gone from the EPA. Only two Democrats voted to confirm Mike Pompeo as secretary of state despite a résumé second to none. Only three Democrats voted to confirm Neil Gorsuch, a justice in the Scalia mode, a true constitutional scholar. This cannot be said for Sotomayor and Kagan.

Throughout his two terms, Obama appointed people who, like him, view the Constitution as an old, irrelevant document written by old white men. The left today, like Obama throughout his administration, seeks to increasingly transform the U.S. into a socialist nation with all the abrogated freedoms that would entail.

How to achieve the Marxist society they favor? Destroy everyone, every conservative, pro-Constitution person and every person of faith who reaches or aspires to a position of power, and do it by any means, no matter how low, no matter how illegal, no matter how immoral. This is what they do.

Those who do not stand up and yell “foul” but stay silent and go along to get along are as guilty of these crimes against the country as was the Ted Kennedy left and the Chuck Schumer-Nancy Pelosi left are today. Of these people and their fellow leftists, not one has spoken out about the crimes of the Clintons and the pay-to-play scheme of their “foundation.” Not one.

The Democratic Party of today, as Dennis Prager has so often pointed out, is no longer liberal, no longer the party of JFK. It is now the party of Saul Alinsky, the man who instructed, “Pick the target, freeze it, personalize it, and polarize it” and “If the ends don’t justify the means, what does?”

This is who the left is today. Leftists’ mission in life is to destroy anyone who gets in their way. Vince Foster knew of what he spoke.

“The Democratic Party today has moved so far to the left, become so radicalized, that it is a blight on the American landscape.”

The Dem elite are conservatives on everything except a few trivial social issues, and they are called radical communists by the people who control 2 branches of govt. There is the indicator of which direction US politics leans towards.

The 20s will roar again.

Center/Right if you are on the Right.

Conservative hacks.

Dims

I though Hillary killed Vince Foster?

Daily News?

“flexibly centrist” with a “high-minded, if populist, legacy”.[19] The News endorsed Republican George W. Bush in the 2004 presidential election.

Sounds like a left wing publication.

Since May 2017 the former FBI chief Mueller investigates an alleged collusion between Trump, his campaign and something Russian with regards to the 2016 election. No evidence has been produced so far that substantiate any such collusion. The people who fanatically claim that there must have been such a connection are now disappointed. The long awaited Stone indictment was one of their last straws. But there is absolutely nothing in it that hints at any collusion.

All these alleged crimes were committed in relation to an appearance of Stone before a House Permanent Select Committee on Intelligence (HPSCI) investigation.

During the 2016 election Stone publicly claimed that he was in direct communication with Wikileaks and its editor Julian Assange. Steve Bannon, then part of the Trump campaign, asked Stone to ask Wikileaks at what time it would release new batches of emails that had been obtained from the Democratic National Committee. The Trump campaign was naturally interested in using these releases to attack the competing candidate Hillary Clinton.

Wikileaks and Assange denied that they had any relations or communications with Roger Stone. It later turned out that Stone had two contact persons, the New Yorker comedian Randy Credico and the conservative writer Jerome Corsi, who he MIGHT have had some contact or insight into Wikileaks. The indictment says nothing about their relations to Wikileaks.

During his appearance in front of the HPSCI Stone misremembered, contradicted or lied about several details related to his earlier false claim. He also asked Randy Credico to lie to the committee. Those are the only issues the indictment is about. It is about the lies of a notorious liar which became process crimes when he repeated them during an investigation. Stone himself denies emphatically that he committed any crime and promises to defend himself in court.

Nowhere does the indictment say that this has anything to do with the Trump campaign, Russia, Wikileaks or the not existing relations between them.

But some media will not tell you that……

https://www.moonofalabama.org/2019/01/pelosi-aghast-stone-indictment-proves-that-trump-campaign-deliberately-campaigned-for-trump.html

Thanks. It does help to get a bit of clarity.

“O brave new world that has such people in it”

Roger Stone’s worst crime, of course, is that he has aged horrifically. I thought he was supposed to be RICH? The solution is to trick him into the Big Brother House, where he will be literally stoned by an invited audience. This will be poetic justice, a beautiful post-modern event and will aid community cohesion. 🙂

Thanks, Duncan, obviously you hit a nerve….what did Trump expect? His term in office up to now was undoing the previous Democrat President’s policies and boasting about it.

Did Mr. Trump expect cooperation with the opposition? If so, he is naive and not a statesman.

never mind

this will give you 4 minutes of hilarity at the don’s expense

https://youtu.be/ZL5CDt_1xcE

Trump is not the brightest porch light on the block—

Clinton not ruling out running in 2020: report

https://thehill.com/homenews/campaign/427156-clinton-not-ruling-out-running-in-2020-report?amp&__twitter_impression=true

https://i.imgur.com/vI6H49x.gif

The Dims need to get wise—

I know its a long shot.

They did, their following the MONEY just like the repugs are.

That’s why I won’t waste my worthless “vote” on either of them!

Cheer up! Perhaps Nader will run again.

Mr. unsafe at any speed.

Maybe Nadar will get a Corporate sponsor this time around…

Nader is so clean, even the repugs couldn’t frame him.

Corporate? Not a chance he would be that slimy.

one theory (perhaps of many) is that she is “thinking” of running again (against Trump of course) so that if his DOJ brings criminal charges against her, she can claim that it is purely politically motivated…

my understanding is that Comey actually admitted there were crimes but that she didn’t intend to commit those crimes, so therefore he gave her the FBI Special Pass…

Here’s a fascinating video examining Clinton’s body language.

https://www.youtube.com/channel/UC65EDzqpOAQZLBmAdHAnZng

Wrong video, as far as I can see.

If she wasn’t a viperous b**** at the State Department, I would’ve voted for her. She’s ruthless, but I think the Clintons would generally be adults in the room, so-to-speak.

Meta-politics inspired by game of thrones characters is precisely why the Ds lost. The loonies can play that game harder, longer, better because not very much can be done to improve the avg voters’ lives at this point. May as well promise things people do want.

Jeff Bezos gives a pitiful amount of his $160B fortune to charity

https://nypost.com/2019/01/26/jeff-bezos-gives-a-pitiful-amount-of-his-160b-fortune-to-charity/

And just to give you an idea of how rich billionaires are..If you inherited one billion dollars, you could spend $1000 dollars a day for over 2700 years before you ran out of money..And that is just one billion dollars..Bezos has around 160 billion..

maybe he’s concerned that too much charity would be inflationary. or maybe he’s just so tight he squeaks?

but but but…

he claims that Blue Origin is his most important work:

https://www.blueorigin.com/

he’s going to save the human race!

he can’t be wasting his money on charity…

He’s a strange guy.

check your history

anyone lucky enough to be the first to discover what people want, and deliver it to them, gets very rich indeed

Also, his ex-wife McKenzie is going to get a hefty cut of that ¥160B, forcing Jeff to take somewhere between a haircut and a scalping! After the lawyers get their cut, there might not be a lot left for poor old charity to sink its teeth into.

He should have her “clipped” 😉

Back 10 years ago, the elites at the Davos conference were seen as the people who ruled the world..

Now they are seen as the people who ruined the world..

but don’t we know better?

that the decline in net (surplus) energy derived from FF is what eventually will “ruin the world”…

at least by about 2030 or so…

True, but being chattering apes, a physical fact will always be given, by preference, a social-political explanation.

Has U.S. shale oil entered a death spiral?

http://mediad.publicbroadcasting.net/p/kstx/files/201311/permian_basin_oil_rig__mose_buchele_.jpg

“With the big Wall Street players now questioning the value of their existing investments in shale oil, the industry is finding it hard to raise money. Not a single bond sale has come off since November in an industry which must continuously raise capital to survive.

To add to the problems, the future of U.S. shale oil production seems to be in the Permian Basin in Texas which has been providing the lion’s share of oil production growth for the entire country. But ongoing drought in an already arid West Texas has raised doubts about whether the Permian will have enough water to meet all the demand for fracking new wells.”

Lack of funding could prove to be a huge problem. Lack of water for fracking combined with lack of water for funding could easily put them out of business. Waiting for desalinated water form the ocean, and taking it by truck to where it would work would theoretically be feasible, but the cost would be outrageous.

Profit does not seem to be a business model.

Just keep the game going—-

You are right. We seem to have a lot of businesses, worldwide, that seem to be operated just to keep the game going. China understands that businesses need to be operated to provide jobs for people. In a sense, this can be their primary purpose. All kinds of debt can be added, so that the system seems to keep operating, even if the output produced has virtually no value to anyone (homes for investors to buy that will fall apart after building, homes that not enough workers can afford to live in, unneeded roads and airports, unneeded rapid transit trains that few can afford). In the US, the story can’t be quite this transparent.

“…homes for investors to buy that will fall apart after building”

Hey now Gail. Give credit where credit is due!

Those million dollar Chinese investment properties don’t start falling apart for at LEAST 2-3 years after they are built! 😉

This is a good article on the water problem in the Permian basis that Kurt Cobb links to.

https://oilprice.com/Energy/Energy-General/Low-Oil-Prices-Are-Not-The-Only-Problem-For-The-Permian.html

The article points out that this is likely to be a cost issue, pushing down the margins of producers further, as they move to less desirable acreage as the best areas are drilled further. Recycling of “produced water” can be done to provide additional water, but this costs several dollars a barrel. Trucking water from a longer distance probably costs even more.

“With the big Wall Street players now questioning the value of their existing investments in shale oil, the industry is finding it hard to raise money.”

USA might have to nationalize this industry…

Might. They also will need to nationalize investments in natural gas and coal. Something tells me that this really can’t happen, because the US is already in a position where it cannot reasonably balance its budget. Too much has been promised to the elderly and disabled. Also, private pensions look ready to default, in the next few years. They would need to be nationalized as well. Too many problems to fix the way people would like them fixed.

Simple solution, comrade.

Nationalize everything! Then no need to worry about pesky “budgets”, and socialist umbrella takes care of everyone 🙂

https://alphahistory.com/coldwar/wp-content/uploads/2012/06/dossier-start-bg1.jpg

Former NASA scientist and climate advocate James Hansen said “suggesting that renewables will let us phase rapidly off fossil fuels in the United States, China, India, or the world as a whole is almost the equivalent of believing in the Easter Bunny and Tooth Fairy.”

https://freebeacon.com/issues/critics-polis-100-renewable-energy-pledge-based-on-magical-thinking-will-cost-millions-of-jobs/?fbclid=IwAR3aATRCi9aZLMihbNdLhpcEgEYR9g5EHt_izjY2_t7BKJUEQ7vucnKZmU0

Heinberg says the same thing

Your right, their both NUTS! You cannot “transition” from a RESOURCE to a TECHNOLOGY that’s dependent upon that SAME RESOURCE!

What is so complex about comprehending that SIMPLE FACT?

I suspect their getting paid to say that as they must surly know that “renewables” cannot replace essential resources.

They will find out, the hard way.

The “yellow vests” will be out en masse when the lights go out & their left freezing in the dark as their batteries die.

I would keep a VERY close eye on the rig count – https://ycharts.com/indicators/us_rotary_rigs when it tanks, that’s it!

I feel sorry for all those young people who are demanding that we “keep it in the ground” & “get off oil & transition to renewables”, they know not of what their asking for.

Please read it again, Sheila. Hansen and Heinberg would agree with you that one cannot “transition” from a RESOURCE to a TECHNOLOGY that’s dependent upon that SAME RESOURCE! They point out that we won’t be able to transition to renewables.

On the other hand, they are suggestion that we might be able to transition to some form of nuclear, and if pressed they might well argue that nuclear, once it gets up to speed, needn’t be dependent on fossil fuels. The same might be argued for space-based solar.

Whether any of the above technologies can really be independent of fossil fuels in the real world rather than just in theory is a question I am not qualified to answer.

energy is use-less until it is put to use

without all the whizzy whirry things we depend on, energy doesn’t have any use

but all those whirry whizzy things require fossil fuel energy to produce

That’s the wall I keep banging my head against over on Resilience

why I don’t know

masochism I guess

still—when I stop it feels good

I feel sorry for the young too: they mostly don’t know how things really work from the energy point of view, and they are being fed such propaganda in the media, and at school. too – they will believe that the ‘New Green Deal’ is something real.

It is not a good plan to bring people up on Utopian fairy tales of that kind.

Real fairy tales are much better and more true to life.

“I feel sorry for the young too: they mostly don’t know how things really work from the energy point of view”

Do we “old” people (though I’m only in my late 30’s, so I like to imagine I’m not “old” just yet) really know how things work from an energy point of view? Even those of us who frequent OFW and have a greater understanding of the energy predicament we face don’t really do much to change our current energy paradigm. Instead, we continue to live in our own energy “Utopian fairy tale”, struggling with the cognitive dissonance that comes with the realization that our way of life will end (and likely soon).

I’ve come to the conclusion that there’s really no point in criticizing all the different groups of people (e.g. “New Green Deal’ers”, “Peak Oil Deniers”, “Status Quo’ers”, “#MeToo’ers”, “Canadians”) out there, as they basically all have their own “Utopian fairy tale” in their own minds – all of them just as bad as the rest, really. Their constant screaming, bickering, arguing and fighting with their various detractors is simply the ongoing struggle to see who will be in charge of the great unwashed masses, and thus enforce their version/vision of the “Utopian fairy tale” on everyone else 😐

Don’t you know that motors can be run on water but big energy is suppressing this fact because they would lose their income? On a serious note I guess rig count is where the rubber meets the road.

“A person often meets his destiny on the road he took to avoid it.”

“More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly.”

― Woody Allen

“When you come to a fork in the road, pick it up and eat something with it.”

— Me

https://imgur.com/a/dQ6jk9M

I homeschooled my daughter for one year, the year she was supposed to be in eighth grade, when she was about 13. I continued to work part time as well; the requirements for home schooling were not very demanding. She taught herself HTML and put up a blog that she updated nearly every day, receiving over 1000 hits per day. She also started some sort of a newsletter, which she sent out by snail mail to subscribers who sent her $1 per issue, also by snail mail. She would not have learned those things in school.

We also ended up sending both of our boys to a private school for several years.

I have very few relatives with children in school now. The few who have school age children are homeschooling them now.

I can very easily see how homeschooling would be preferable. Wish I’d had that option growing up instead of going to the zoo school I went to before high school that was anything but a place of learning. It was violent and mostly a series of distractions from learning. Teachers didn’t even try to intervene in fist fights and nothing happened – no one went home, no trip to the principals office, nothing. Integration meant payback to the descendents of the slave owners. Nothing could be said otherwise or it was considered prejudice. On our last day at that school people were elated, happiness pervaded all day long and for some reason no one got their pockets picked, their lunch stolen, bullied or humiliated. I wonder why? It was their last chance to do something to us. Why not? Maybe that was suppose to mean we were suppose to forget everything that happened there.

Then we went to high school where it was different, not violent, just trying to catch up on what wasn’t learned in junior high and get good enough grade to go to college. And college I must say was a beautiful experience of higher learning and the rest of the joys of life.

To qualify for a collage education, you first need a good educational foundation, but if your a girl, have divorced parents, were raised by grandparents who thought their days of raising children were over, were moved around a lot, different schools, different types of “learning”, were picked on, mocked & bullied, & couldn’t even see the chock board where the lessons were taught, you couldn’t get the educational foundation that was needed for collage.

In high school, girls were regulated to the “mommy track” we learned how to be house wives, a “skill” no employer would need, girls were not allowed to take any of the trade classes, those were for BOYS ONLY, we couldn’t even learn to drive, BOYS ONLY!

Too much home “schooling” in the US is RELIGION based! So along with math & ABC’s, they “learn” that Jesus is lord & “savior” & the “rapture” is coming “soon”.

Home schooling can be superior to public school with the right, EDUCATED parents, public schools just teach us to believe what we are told & not to think for ourselves & we were tought a lot of BS.

Now PBS which used to have good programing is sounding more like Fox “news” reich wing propaganda every day, their even repeating the LIE that Venenzualia collapsed because of “socialism” with no mention of the real reason for it’s collapse, the steep drop in the price of it’s OIL from over $100. a barrel down to $30. a barrel & the sale of oil was 87% of it’s income. I guess spending money to provide it’s people with health care, child care, maternal care & food assistence is “socialist” & thus a crime. Let ’em die!

Any country that lost 70% of it’s income whether capitalist, socialist or communist would collapse.

Now the US is working to overthrow it’s DEMOCRATICALLY ELECTED president with it’s own, corporate puppet so it can seize it’s OIL just as it overthrowed it’s ruler in Iraq to steal it’s OIL, same thing happend in Libya – OIL again, in Afghanistan it’s rare earths.

We are currently engaged in 15 military actions.

thanks god we have sent some proof of

homo sapiens in deep space regardless

what happens to our species

https://youtu.be/w_T0Xt_PooM

Not the appropriate site to get philosophical, but I have always wondered if, assuming that life evolves (whether spontaneously or via diaspora) throughout the universe, all civilizations are ultimately doomed to a cruel death loop whereby they either destroy themselves or some cataclysmic event like a meteor prevents them from advancement to the point that they can ever make contact with another advanced life form.

Remember, it is not just the distance, measured in light years, that keeps us apart, but also time! Earth is 4+ billion years old, the last 500 million with life forms, but so far only a century with “advanced intelligence” capable of making and receiving contact. An incredible temporal coincidence would be required to cross paths.

In fact, that was the most striking feature to me of the introduction to the Star Wars movies. The story was based on events a long time ago. Civilizations far more advanced than ours could hope to become may have already arisen and vanished hundreds of millions of years ago. We are programmed to think only of advances being in the future, not in the past, and that we as a species could never devolve back to a more primitive and less energy intensive existence.

it seems to me, that any level of civilisation is entirely dependent on its ability to convert one energy form into another

Egyptians converted food=muscle==stone& metals

Greeks Incas and Romans did the same

the laws of physics preclude any “other way”

There could possibly have been ancient civilisations (1m yr +) using the above progressions, but none on our level because to do so would have involved consumption of finite resources–which is the problem we have. If they had consumed them, they wouldn’t have been there for us in our own era. We know the elements in the periodic table. There are no others available.

High energy inputs are necessary to convert and use those elements.

It doesn’t seem possible to have a cohesive civilisation unless you have hard edged tools driven by forces stronger than the people of that civilisation. (you can’t do things without tools)

Thus we get back to the universal law:-

Civilisation is dependent on explosive force converted into rotary motion

You are right. Most of what we have is in some sense converted energy.

this is an absolutely ”must watch’

Jeremy Rifkin, the third industrial revolution

https://www.youtube.com/watch?v=QX3M8Ka9vUA

1.5 hours–so take it in small doses, but brilliant clear frightening stuff

This is what Jeremey Rifkin’s book blurb on the same subject says:

What Rifkin has to say is a must watch/listen because of the clarity of his delivery and information, particularly on entropy and economics

however, where I think he falls down—is on that ”millions of businesses” thing.

Our fundamental problem is extraction of food-energy from the earth

no matter how many whirry whizzy things you have in your hand or pocket, if those food calories don’t appear on your plate, it’s game over

Food calories are terribly important, I agree. And electricity does nothing for providing food.

I think the other part of the system that is terribly important is the built infrastructure–the roads, bridges, pipelines, electricity transmission lines, water and sewer treatment plants, the refineries, the furnaces, the railroad tracks and airports, and even the airplanes, trains, trucks, fire engines, and many other vehicles that make our system operate. We cannot make or even repair these items with electricity. They require fossil fuels. These things tend to be “out of sight, out of mind”. But if these things break down, our system is in deep trouble. Admittedly, the furnaces could perhaps be replaced with heat pumps, but even doing this requires metals and a transportation system. These require fossil fuels, not electricity.

NO, everything we have is converted energy!

try not eating for a week

But where does Rifkin deal with that cultism or monasticism that you (and I) have considered sine qua non? Or Reinhold Niebuhr’s Divine Madness of the Soul? Apparently, Rifkin can do without mystery. Then what about the human proclivity to tribalism? Does he consider that? Does he also consider that the path we’re on might have to do with somebody’s (not everybody’s) epistemological construction? .

Thanks Norman for the Rifkin link….His well received best seller way back in the 80s, “Entropy: A New World View” was a major tpping point in my life…was set on the Doomer path ever since and look where it led me….thanks Mr. Rifkin!

From Wikipedia

In the book the authors analyze the world’s economic and social structures by using the second law of thermodynamics, also known as the law of entropy. The authors argue that humanity is wasting resources at an increasing rate, which if unchecked will lead to the destruction of civilization, which has happened before on a smaller scale to past societies. The book promotes the use of sustainable energy sources and slow resource consumption as the solution to delay or forestall death by entropy. Critics: Rifkin’s 1980 views assume that entropy is disorder. However, a more modern based on information theory treats entropy as uncertainty. The later approach explains how in some cases entropy increases order. In fact, order spontaneously increases in the world all the time in evolution and also in an economy that is constantly improved. Therefore, Rifkin’s book is controversial. See “Entropy God’s Dice Game” by Kafri and Kafri.

I’m stilling waiting for the outcome ….hopefully till I push up daisies.

thanks Bill

I would have thought disorder and uncertainty were so close in meaning that to try to find difference would be nitpicking in the extreme

evolution seems to introduce ‘disorder’ in order to further the necessary game of chance that is our existence

Right, this is one solution to the Fermi paradox. If we collapse … soon …. maybe … in 20 years, we will have sent signals to outer space (artificially generated electromagnetic waves) for about 100 years : this is just a ‘ping’. And we will have been able to listen to alien signals for approximatively the same time. This is a blink of an eye. If all advanced civilizations in the galaxy, or universe, last as little as us, despite their possible large number, the probability that one can ‘hear’ the signal of another is quite low.

Tremendous distances, few time, few energy seem to separate us. This is God’s will : no interstellar tower of Babel.

Hmm, Well now, at least we can’t blame them for the mess we’re in, can we?

This post for Gail.

Back YahooFINANCE

IMF’s Lagarde on the absence of women at banks: ‘Be careful what you look like

The lack of women in finance is unfair to women and bad for banks, International Monetary Fund Managing Director Christine Lagarde told Yahoo Finance this week at the World Economic Forum.

“There’s something wrong,” said Lagarde, who has helmed the IMF since 2011. “If you look at the composition of boards in that sector, only 20% of them are women. If you look at the CEOs of the financial sector, only 2% are women … our societies don’t look like that. And if you look at graduates from universities and business schools, it doesn’t look like 20% or 2%. It’s a lot more than that.

Asked about her advice for Trump if he selected her to be an economic advisor for the administration, Lagarde quickly responded, “Trump would never ask me to be his advisor.”

She continued: “I would try to identify how well-governed, multilateral trade can be efficient and can be beneficial for each and every participant. That would be my mission No. 1.

https://finance.yahoo.com/news/influencers-imf-christine-lagarde-jpm-erdoes-kpmg-doughtie-will-i-am-130107953.html

I like her MISSION….BAU ….FULL THROTTLE …BABY…(and more little ones to keep the economy expanding, of course)

When we discuss such precise statistics, let’s not forget that this very Mrs. Lagarde spends xy% part of every day cooking her already over burned skin on the artificial sun or such similar cosmetics crap procedures..

God Bless their little hearts…They do it to make us menfolk happy….sarcasm….

(More likely worried what others may evaluate them….this is an excellent video on the subject…naturally by a man….ugh! Gail, I hope you like😃).

John Berger has some great discussions…

https://m.youtube.com/watch?v=bZR06JJWaJM&t=424s

Ways of Seeing….

Competitive beauty-who would have thought?

Christine Lagarde is a feminist: all that orange stuff, every morning – she does it all for herself, not to excite us.

This might be behind a paywall for others, but:

https://www.wsj.com/articles/the-facts-about-facebook-11548374613

“The Facts About Facebook

We need your information for operation and security, but you control whether we use it for advertising.

477 Comments

By Mark Zuckerberg

We’re very focused on helping people share and connect more, because the purpose of our service is to help people stay in touch with family, friends and communities. But from a business perspective, it’s important that their time is well spent, or they won’t use our services as much over the long term. Clickbait and other junk may drive engagement in the near term, but it would be foolish for us to show this intentionally, because it’s not what people want.

Another question is whether we leave harmful or divisive content up because it drives engagement. We don’t. People consistently tell us they don’t want to see this content. Advertisers don’t want their brands anywhere near it. The only reason bad content remains is because the people and artificial-intelligence systems we use to review it are not perfect—not because we have an incentive to ignore it. Our systems are still evolving and improving.

Finally, there’s the important question of whether the advertising model encourages companies like ours to use and store more information than we otherwise would.

There’s no question that we collect some information for ads—but that information is generally important for security and operating our services as well. For example, companies often put code in their apps and websites so when a person checks out an item, they later send a reminder to complete the purchase. But this type of signal can also be important for detecting fraud or fake accounts.

We give people complete control over whether we use this information for ads, but we don’t let them control how we use it for security or operating our services. And when we asked people for permission to use this information to improve their ads as part of our compliance with the European Union’s General Data Protection Regulation, the vast majority agreed because they prefer more relevant ads.

Ultimately, I believe the most important principles around data are transparency, choice and control. We need to be clear about the ways we’re using information, and people need to have clear choices about how their information is used. We believe regulation that codifies these principles across the internet would be good for everyone.”

And that is that. If you see irrelevant ads from now on, blame all the people who don’t want to share their deepest darkest lore with Zucki.

Sorry, couldn’t help myself….if I put Zuckerbergs words into pictures..

https://m.youtube.com/watch?v=FCcdr4O-3gE

Yes, Mark, that sums up nicely.

Renewable energy ‘simply won’t work’: Top Google engineers

https://www.theregister.co.uk/2014/11/21/renewable_energy_simply_wont_work_google_renewables_engineers/

Solar and Wind produced less than two percent of total world energy in 2016 — IEA WEO 2017

https://www.iea.org/publications/freepublications/publication/KeyWorld2017.pdf

It Will Take 131 Years To Replace Oil, And We’ve Only Got 10

https://www.businessinsider.com/131-years-to-replace-oil-2010-11

Warning of shortage of essential minerals for laptops, cell phones, electric cars, solar panels, wiring

https://www.sciencedaily.com/releases/2017/03/170320110042.htm

We Might Not Have Enough Materials for All the Solar Panels and Wind Turbines We Need

https://www.popularmechanics.com/science/energy/a25576543/renewable-limits-materials-dutch-ministry-infrastructure/

Study predicts world economy unlikely to stop relying on fossil fuels

https://phys.org/news/2016-02-world-economy-fossil-fuels.html

At this rate, it’s going to take nearly 400 years to transform the energy system

https://www.technologyreview.com/s/610457/at-this-rate-its-going-to-take-nearly-400-years-to-transform-the-energy-system/

Why sustainable power is unsustainable

https://www.newscientist.com/article/dn16550-why-sustainable-power-is-unsustainable/

Top scientists show why powering US using 100 percent renewable energy is a delusional fantasy

http://energyskeptic.com/2017/big-fight-21-top-scientists-show-why-jacobson-and-delucchis-renewable-scheme-is-a-delusional-fantasy/

https://i.redd.it/h48btr94ytc21.png

Russiagate is proof that the American Ideology can’t sustain itself without a boogeyman..

First it was the Soviets Then it was Iraqis Then Isis..And now the…Soviets again?

Maybe one day Americans will actually learn to face the real material conditions of their society..

Dwight D. Eisenhower warned about the MIC. Apparently no one paid attention because the MIC and the Deep State is the tail wagging the dog. When you receive $1 trillion a year you better find a way to make yourself relevant. That’s why we are always starting and looking for trouble around the world.

A long time ago, The American Dream replaced religion as the opium of the American people. Recall, for instance, how they sold Southern California as a paradise to the multitudes and then they pave paradise and put up a parking lot?

Or remember when America was sold as the envy of the world?

http://cdn.differencebetween.net/wp-content/uploads/2017/09/Difference-between-Cost-of-Living-and-Standard-of-living-1.jpg

them was the days

when everyone had their place and knew where it was

the hat business was better then also…

car wax was not so great then, though. all we had were organic waxes and later, silicon wax. you needed to wax your car at least once every 3 months to maintain the shine. no UV protection meant some colors would fade after a few years outside without a car cover.

yup

can’t imagine a time when we didn’t have Romanian car washers

Right! No need for church; we have salvation here on earth!

Sorry Gail,

Couldn’t resist this.

“Man is born free, and everywhere he is in chains.”

-Jean Jacques Rousseau

The world is swimming in $244 trillion of debt

https://markets.businessinsider.com/news/stocks/debt-around-the-world-hits-244-trillion-near-record-2019-1-1027872023#

wake me when it gets to $488 trillion…

Here’s a WSJ article from March 2016 saying we were at about $122 trillion:

https://blogs.wsj.com/moneybeat/2016/03/17/global-government-debt-is-actually-triple-what-we-thought-thanks-to-pensions/

Only about 2.66 years to double – fantastic!

Looks like we’ll be waking you up pretty soon, David… 🙂

Governments are mostly on a pay-as-you go basis. They guarantee bank accounts, pension plans, and nuclear power plants, but never carry any liability associated with these guarantees. The funding of Medicare is on a pay as you go basis. The funding of Social Security is very close to a pay-as-you go basis. There was extra funding collected a few years back, because it was clear a big number of baby boomers will be retiring. The government spent this extra money on other things (wars, probably), and left non-marketable US debt securities in place of what had been spent. So it still has to pay, one way or another.

So there is a lot of “debt” outstanding, that does not show up on any balance sheets. If energy supply were growing fast enough, and cheaply enough, perhaps it would be possible to pay these amounts.

https://www.businessinsider.com/trump-china-trade-war-winners-and-losers-chart-2019-1

There is a chart in that article definitely worth looking at, which shows the amount imported into China from different countries. It’s labeled: 7. winners, losers and Germany in the crossfire. In the latter half of 2018 the US, Japan and Germany’s exports to China plummeted big time, whereas Brazil skyrocketed. Russia was going up with Brazil, but then started dropping.

“Brazil has seen exports to China jump as a result of the stopping of US soybean exports to China thanks to the trade war. China turned instead to Brazil for its oilseed, causing a major spike in Brazilian exports of the agricultural commodity.”

These developments have all occurred as a result of the tariffs. I wonder now that China is getting their oilseed from Brazil if they China will ever decide to return to US soybeans. That’s the problem with major changes that happen as a result of a trade war – they don’t necessarily just pop back to how they were before.

This is the chart included in that Business Insider story:

https://gailtheactuary.files.wordpress.com/2019/01/china-percent-change-in-imports-by-partner-will-martin.jpg

It is a little difficult to read. I think it means percent change in a given quarter relative to the corresponding quarter a year ago, of all imports of goods and services from a given country.

fantasy time again

https://www.bloomberg.com/news/articles/2019-01-26/saudi-crown-prince-to-launch-425-billion-infrastructure-plan

“Saudi Arabia is seeking 1.6 trillion riyals ($425 billion) in investment by 2030 for infrastructure as well as energy, mining and other industrial projects, as part of an effort to cut its reliance on oil…”

ah, my favorite year appears once again…

the cost of “industrial projects” in a desert surely can’t be economically competitive with non-desert locations…

the article didn’t say if they have any resources that the rest of the world wants besides oil…

and if they think oil prices will be in a “high” range between now and 2030, they are sadly mistaken…

they obviously employ the same advisers as the emperor did when he bought his suit of clothes

isn’t it like 4:19 a.m. where you are?

fraid so—couldnt sleep

finally gave up and came on here to cheer myself up

LOL

Everyone promises ‘infrastructure investment’ these days – the ‘New Green Deal’, Corbyn in Britain, etc, – as if it were a kind of magical formula to revive a dying global economy.

In part, this will simply be an attempt to shore up what has already been built and is starting to crumble (rather quickly in the case of China!) and keep the electorate employed.

But it isn’t a magic bullet: historic infrastructure investment only made sense in so far as it enabled access to resources, processing, distribution and international commerce.

The building of towns, roads and bridges in 10th -12th century Europe truly re-established civilization and made further economic growth possible, and was quickly profitable. Same for Roman roads and ports, British canals and railways.

Otherwise, it merely functions to maintain debt expansion,and demand from temporarily-employed construction workers and associated professionals: politically and financially expedient, ‘keeping the plates spinning’,but only in the very short-term, and in no way is it an ‘investment.’

It’s almost Cargo Cult thinking…. Or like the old proverb ‘Have a baby and the food will come for it’.

Infrastructure investment is a way of raising demand for fossil fuels, and thus raising their prices. If infrastructure investment fails, we are in deep trouble. This is the reason for building all of the unneeded houses and roads, airports and high speed trains. It is the usual lever governments push on to try to get employment up as well as commodity prices up.

what it comes down to is:

don’t let this crash on my watch

Or, we are in deep trouble, so indulge in one last ,unsustainable – and unmaintainable – infrastructure expansion to maintain the illusion of demand and growth.

What was truly functional in creating prosperity, in the early stages of a civilisation, becomes a kind of totem for a failing system in its last stage.

Hellworld has no apex:

Starbucks CEO Howard Schultz is gearing up for a self-funded independent presidential run

https://www.theatlantic.com/politics/archive/2019/01/howard-schultzs-independent-run-could-help-trump/581374/

“self funded”… that might be good news…

if he puts a billion of his dollars back into the 2020 economy…

If truly happening and possibly in higher numbers more examples, that would support the theory-scenario of US finally turning into the age of openly-disclosed oligarchy..

This ‘doomsday prepper dream home’ in the Nevada desert is on sale for $900,000 — take a look inside

https://www.cnbc.com/2019/01/25/photos-inside-doomsday-prepper-castle-in-the-nevada-desert.html

goldmine will be good come doomsday

It is amusing how we have been conditioned to accept that renewable are self sustaining…”The castle is completely self sustaining and off the grid. Power comes from batteries charged by solar and wind energy. There is a 3,000-gallon propane tank to power heaters throughout the house, a 300-gallon diesel storage tank to fuel a diesel-powered generator and two back-up generators — one diesel and one propane. There is a 4,000-gallon water storage tank. There is both a rainwater harvesting system and an 800-gallon water-hauling trailer to bring water to the building.”

This property is of course, not self sustaining in the slightest.

A 500 lb pound bob would be the best end for this stupid extravagance.

another week of bau is ending that called for celebration

https://youtu.be/tzkG6Xu6lUE

this remind of man its time end this stupid war on drugs

especially after watch this video https://youtu.be/1BwVxmJPies

“another week of bau is ending that called for celebration”…

okay! BAU tonight, baby! just had a fine piece of dark chocolate…

4 weeks into 2019, and still going strong…

although I suspect that by the end of this year, TPTB will be saying that the recession started in Q1…

without any OFW type foresight, I went back to a “state” job earlier this decade, after having been laid off from a private company in the 2008/2009 Great Recession…

so although nothing in life is certain, I think I’m positioned to stay employed even if this recession hits hard… and I’m guessing that it will be worse than 08/09…

in the meantime, sure, celebrate…

Morris Berman said somewhere that all Americans think of themselves as temporarily embarrassed millionaires.

Good tactical thinking, when the ships starts to wobble, there will be enormous push of desperate folks kicked out of private sector then trying to bolt onto such “state/municipal” job.. of at least some temporary job security be it formal or real..

You never know, such few extra months of income/purchasing power might make a difference for future rounds-rodeos..

Certainly, in a decline the public sector unions, if they act as a consolidated voting block (as in Spain), can twist the arm of government for funding – much stronger leverage than most private sector workers who are too fragmented and often not unionised now.

In Spain the public sector workers are doing much better than private in wage negotiations: very powerful vote at the city and regional level, and politicians are keen to butter them up.

And in a revolutionary situation, all,resources will tend to flow to the state and political sector, even if it’s just a question of having a bed, meals, and boots on your feet, like the early Bolsheviks c 1920.

‘Resistance’ Media Side With Trump to Promote Coup in Venezuela

Trump ramped up the Obama administration’s sanctions, an action that caused Venezuelan oil production to plummet (FAIR.org, 12/17/18) and the economy to nosedive. Furthermore, US economic warfare against the country has cut Venezuela off from global capital markets—with the Trump administration threatening bankers with 30 years in prison if they negotiate with Caracas a standard restructuring of its debt (AlterNet, 11/13/17). The UN Human Rights Council formally condemned the US, noting that the sanctions target “the poor and most vulnerable classes,” called on all member states to break them, and even began discussing reparations the US should pay to Venezuela.

https://fair.org/home/resistance-media-side-with-trump-to-promote-coup-in-venezuela/?awt_l=O0FxW&awt_m=iAoY9fmr42R._TQ

Liberals will side with fascists against socialists, etc

US wants VZ to fail so it can justify going in on behest of Exxon to reclaim the oil fields they helped develop but feel it should be all theirs and not the people of VZ.

US diplomat convicted over Iran-Contra appointed special envoy for Venezuela

(Elliott Abrams, who was linked to failed coup against Chávez, to join Pompeo to urge security council to recognize Guaidó as head)

https://www.theguardian.com/us-news/2019/jan/26/elliott-abrams-venezuela-us-special-envoy

again and again

all conflicts is over resources

Murdering Latin American socialists and installing fascist governments across the region is a bipartisan issue. Liberals and conservatives both have a long history of supporting it.

oil is your lifeblood

nobody offers up their neck for their throat to be cut—irrespective of politics

we may not agree with it, but collective instinct kicks in

the USA sees Venezuela as its fuel tank—which is unfortunate for the folks living there

Europe badly needs diesel. They many the choice to operate their cars on diesel, as well as their trucks.

their turbo diesel engines get 50+ mpg, so the efficiency helps. that would be equivalent to a modern hybrid electric.

Well that’s history..

But now most of the companies are phasing these quality diesels out of the market/production! Instead the Brussels is pushing turbo gasoline engines of small displacement, even such crap like sub one liter engines on three valves..

Diesel is more energy dense—-

The world runs on diesel.

It doesn’t matter. You use what you have. Planning to become the chief buyer of an energy dense fuel, when there isn’t enough to go around, is a bad strategy.

The world runs on diesel–

Sorry, but it is true.

Is it possible (costwise) to convert gas cars to diesel?

Nope, only special custom vehicles..

Otherwise, normal car is easier to convert into natgas (CNG) or (LPG).. but you can’t park that in most public or even private garages.. And to purchase new car and leave it parked on street open to elements, fast temp/moisture cycling, no thanks that’s for i(diot)s.. Hence, large EV sales especially in countries with high purchasing power and or subsidies.

It’s a nice coordinated scheme how to corral plebs out of diesel usage for good.

(CNG) or (LPG)

Oh, I see. Fear of explosion!

Why in the world would a person want to convert a car from gasoline to diesel? Diesel is the fuel in short supply because everyone wants it. Oil sources that are primarily “heavy” and thus yield lots of diesel, are expensive to extract. They also often need “cracking,” which adds to the expense. It is hard to get the price of the heavy oils up high enough for the producer. They usually sell at discounted to WTI and Brent, because of the higher costs involved in refining.

Either gasoline or natural gas (CNG LPG) would be cheaper for operating a car, per mile traveled.

Germany continues to destabilize European energy sector in higher gear. They are basically pushing up pricing for renewables by crippling the existing reliable baseload infrastructure:

https://www.dw.com/en/germany-to-stop-using-coal-by-end-of-2038/a-47244572

They agreed to drop ~20GW of (brown coal and nuclear) power output in a decade, lolz.

Is that sheer ideology-lunacy of the German kind again or they are so cunning and intentionally front running collapse, i.e. closing the shop down, hah?

“The coal phase-out, for which green groups have campaigned for years, is backed by almost three-quarters of Germans, according to a new poll…”

mass hysteria!

so they want to end local coal production jobs, and the fallback is buying more Russian natural gas to satisfy their baseload electricity production needs…

they don’t know that this economic loonacy is what they are going to be getting…

oh well, they will be poorer but at least they won’t be burning that evil coal…

They may well end up burning that evil “someone” though. When times get really tough for civilized humans, historically the veneer of civilization tends to peel off, revealing the instinct to lash out at the other.

Then they “discover” that the only solution instead of coal is nuclear.

Car sales collapsed in Europe in the last quarter of 2018 and a gasoline glut has lead to negative returns on gasoline production for European refineries.

https://pbs.twimg.com/media/DxwYSSfX4AAaoCx?format=jpg&name=medium

.., RR, Jag LandRover, (and others) are extending their late winter/spring assembly line brake periods.. In other words dropping sales + brexit effect in action.

In some of their Spanish plants at least, VW are sacking workers over 61, replacing them with younger cheaper versions.

This has come after many stoppages in 2018 due to ‘lack of suitable engines’. 🙂

In Japan, younger isn’t necessarily cheaper. Especially among smaller manufacturers, they are encouraging older skilled workers to keep going because they are tried and tested, don’t require training, and are happy to work for a lower salary as they are already getting their pension.

I know factory workers, mechanics and nurses who are working into their seventies—to help out the firms or hospitals that require their labor. While many people who work for themselves are still working into their 90s.